SHI 8.11.21 – Deconstructing Productivity

SHI 8.4.21 – Facing the Delta

August 4, 2021

SHI 8.18.21 – Looking Back to See the Future

August 18, 2021

We all understand the basic concept of productivity. If we “get stuff done” we’re said to have been productive. Productivity is also an economic metric, measured religiously by the Bureau of Economic Analysis (BEA), as a contributing factor in economic growth. But here’s an interesting question for us to consider:

“

Is productivity a ’cause’ or an ‘effect’?“

“Is productivity a ’cause’ or an ‘effect’?“

Asked another way, is ‘labor productivity’ a driving force behind GDP growth? In other words, does increased productivity cause increased GDP growth? Or is labor productivity merely a result — a measurement that explains why GDP grew at the rate it did? This may sound like splitting hairs, but I assure you it is not. This is actually a rather important distinction and I believe the answer to this question explains a quantum shift we’re seeing in the US economy right now. Intrigued? Read on.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

The short answer? Expanding. By a staggering measure. In fact, during Q1 and Q2, annualized 2021 ‘real’ growth averaged about 6.4%. In nominal terms, our US economy averaged almost 12% growth — adding $1.245 trillion of economic activity during the first half of the year. Forever more, COVID-19 will be mentioned concurrently with any discussion about 2020 GDP. Collectively, the world’s annual GDP was about $85 trillion by the end of 2020. But I am confident all 2021 GDP discussions will start with a nod to the blowout 1st quarter GDP growth number, because our ‘current dollar’ GDP grew at the annual rate of 10.7%! Annualized, America’s GDP blew past $22 trillion during the quarter, settling in at $22.72 trillion. The US, the euro zone, and China continue to generate about 70% of the global economic output.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

Every day, we hope to be productive or effective in whatever we do. But being productive has a different meaning at the Bureau of Labor Statistics, a government agency tasked with many jobs — including measuring just how productive the US labor force actually is — as viewed by both “cost” and by “results.” Here’s the BLS website if you want to take a deeper dive:

But here’s a link you should open … as it directly applies to today’s discussion (right click, ‘open link in new tab’):

This article, dated April of 2021 — less than 4 months ago — raises this issue:

“Labor productivity—defined as output per labor hour—has grown at a below-average rate since 2005, representing a dramatic reversal of the above-average growth of the late 1990s and early 2000s. The productivity slowdown during these years has left many economic observers wondering why this situation has occurred and what factors may have contributed.”

Summarizing, the BLS believes your and my productivity at work has been inadequate (below trend) for about 15 years. The BLS, I’m guessing, thinks we’re not working hard enough! 🙂

Perhaps. But for some odd reason, it appears we just started working much harder! That’s right, for some yet-unexplained reason, our collective output has increased dramatically, while at a time, our US labor force is smaller. Let me explain.

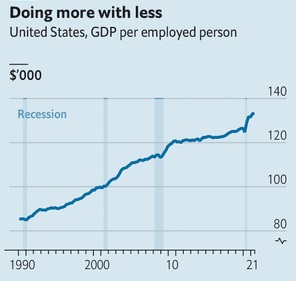

To the left is a graphic from an August 7th article in The Economist magazine. Essentially, what this graph tells us it that over time, say from about 1990 thru today, the amount of US GDP produced by each employed person has grown significantly. Back in 1990, an employed person — on the average, in the aggregate — produced about $85,000 of annual GDP. (And remember: This term, used here by the BLS, is always quoted in ‘real’ terms.) By 2021, this number had increased to about $135,000 per employed person.

It may be a little hard to tell on the graph, but it you look carefully, you can see that since the “recession” ended in early 2020 — yes we had a 2-month recession in 2020 — and shortly thereafter GDP output per employed person skyrocketed.

Said another way, at present, America is producing more output (a larger GDP) than about 18 months ago, and America is doing this with roughly 6 million fewer workers!

That’s the point.

In fact, peeling back the layers of this economic onion a bit more, looking specifically at “Manufacturing labor productivity,” we find that productivity in manufacturing, specifically, is absolutely soaring toward the heavens.

For years, as suggested from the BLS quote above, manufacturing labor productivity (MLP) has been falling. Shrinking. Measured every quarter, in the past 10 years, MLP has been reported 40 times. More than 25 of those quarterly measurements were negative. But not last quarter. No, last quarter we saw a 6.9% increase in productivity.

Why? How is the manufacturing sector, starved for workers, producing more with fewer employees? In a word, automation. And robots.

Amid the Labor Shortage, Robots Step in to Make the French Fries

This is an actual title of a WSJ article from just days ago. It’s an entertaining read … (right click, ‘open link in new tab’):

Restaurants are adapting to the labor shortages.

Said another way, forced to make french fries for you and me without enough people (labor), they have been turning to robotics. This trend is accelerating. The same is happening in warehouses across the world. Take a look at this image:

This machine, manufactured by the robotics division at Honeywell, is designed to unload trucks that have backed into the warehouse. Those yellow things at the top of the image? Suction cups. Honeywell is hoping that once this “robot” is perfected, a single “crew” will be able to supervise the simultaneous unloading of 3 or 4 trucks, each at the rate of 1,500 boxes per hour. Wow.

And we have to remember: These machines don’t take breaks, nor do they get an hour off for lunch. Nope, they work. Nonstop.

Today, US GDP is larger than it was about 18 months ago. At the same time, the US labor force is about 6 million people smaller. Our economy is producing more with less human labor. I contend a large part of that shift is automation and robotics.

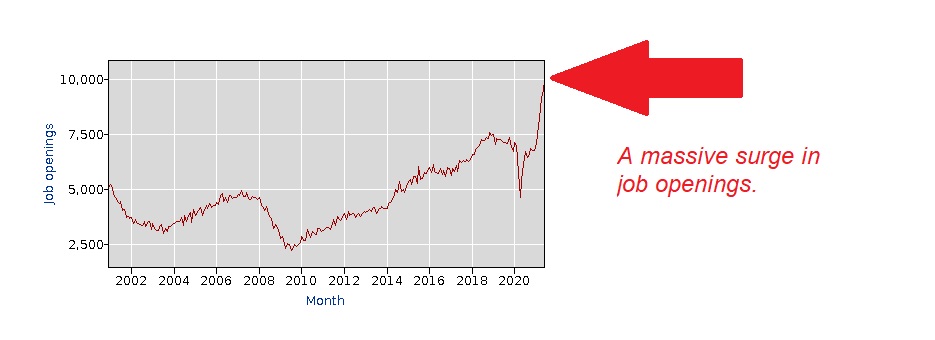

It’s worth noting that while the machines are definitely taking over many “routine” jobs, right now American businesses are also looking to hire more employees than ever before. The BLS also tracks the number of job openings. In June, for the first time EVER, this number eclipsed 10 million: Take a look at this BLS graph … reflecting monthly data since 2000:

The US ‘human’ labor force is currently about 160 million people. And the employers of these folks are looking to add more than 10 million people right now! So not only are robots fully employed … but humans are in high demand too!

Good news if you are an employee: Companies will fight over you today! Well, that assumes you’re more productive than a robot. But assuming you are, you are in high demand! Do you want to work remotely? Today, you may be able to talk your employer (existing or new) into this arrangement. Looking for more money? Ask. How about other perks? This is your time to ask .. employers want you to be happy!

Sorry employers. But I’m not sharing a secret … everyone knows employees are in high demand today. Treat yours well or they may seek other opportunities. If they do, perhaps I can offer a suggestion: Find a robot to do the job? 🙂

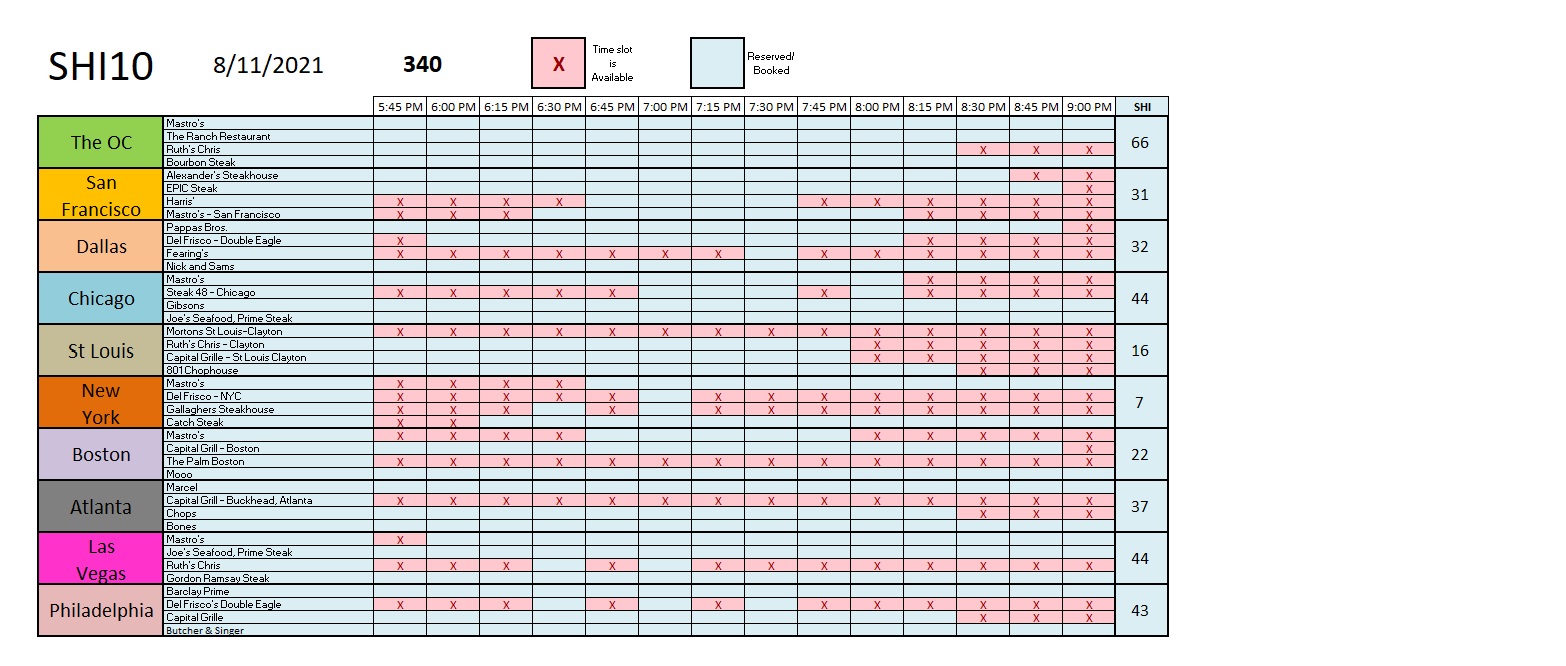

Speaking of demand, are expensive steak dinners in high demand this weekend? Let’s take a look:

Yep. As the trend report below shows, demand this week is the highest in about a month. Expensive eateries remain quite popular all across the country. Pricey beef is in high demand in the OC, ‘Vegas, Chicago and Philly. Restaurants in cities with high ‘delta variant’ infection rates — Dallas and Atlanta — are both showing high reservation demand for this Saturday. New York continues to languish … but, once again, I think their issue is more excess supply than demand.

Here’s the longer term trend report:

As we see above, the ‘Spread’ remains quite high, suggesting expensive steak reservation demand remains elevated relative to 2019 – pre-pandemic. Once again, the steakhouses suggest both beef and the economy are cooking.

Shortages are commonplace today. We observe some empty shelves in the grocery store, other shortages we hear about thru news feeds, and everyone who’s gone to a restaurant lately has seen the impact of supply chain disruptions in both staffing and prices. I doubt this will end soon. Not with employers seeking more than 10 million new employees. The only easy prediction here is the increasing acceleration of business automation. American business has always innovated and adapted. This continues unabated.

I believe GDP growth will continue even if employment levels don’t return quickly. If an employer cannot find a willing human employee, I believe more and more will “substitute” a machine in to do the job. Like you, I’m not a fan of this transformation, but like it or not, it is happening. And this trend will do nothing but accelerate.

<|> Terry Liebman