SHI 7.24.21 – Keeping it Real

SHI 7.21.21 – Working Without a Net

July 21, 2021

SHI 8.4.21 – Facing the Delta

August 4, 2021

When talking economics, it is critically important for the difference between ‘real’ and ‘nominal’ to be front of mind.

You will recall that ‘real’ means the number has been adjusted for the current rate of inflation, or ‘deflated’ using an inflation-type index. Some economic reports reflect the ‘real’ numbers as “Chained dollars” – suggesting a history of inflation adjustments have been made since the date specified. A ‘nominal’ number is the opposite. It is simply a current measurement. It does not take current or historical inflation into account. It’s just the number today. Sometimes, a ‘nominal’ number is reported as a “Current dollars” number – suggesting the number reflects today’s reading, without adjustment.

“

Your cash is worth less than you thought.“

“Your cash is worth less than you thought.“

Let me give you an example. Suppose you have $100 in your savings account. And let’s further assume you deposited that $100 exactly one year ago. As we all know, banks literally pay nothing on savings these days, so during that 1-year you probably didn’t earn any interest. You still have $100 in your account … and so the nominal or “Current dollars” value of your account is $100. If you wanted to, you could take that 100 bucks out of your account and buy $100 worth of stuff. However, on July 13 earlier this month, the BLS reported that the Consumer Price Index increased by 5.4% during the past 12 months (thru May, 2021). The ‘real’ value of your $100 today is actually lower by 5.4% after taking 1-full year of inflation into account. Thus the ‘real’ – or inflation adjusted – value of your savings account is only $94.88 today. In ‘real’ terms, your savings account is worth less than the number on your bank statement.

Sorry to be the bearer of bad news. 🙁

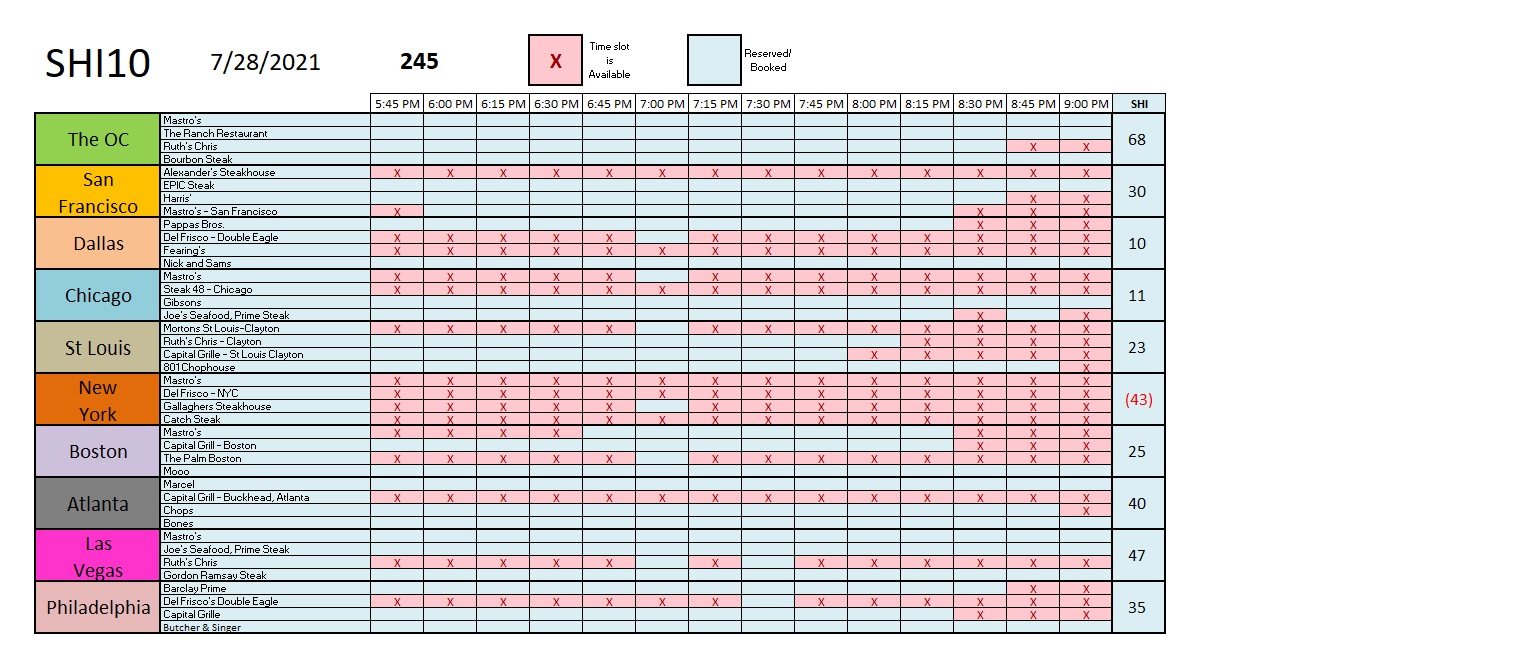

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

The short answer? Expanding. A lot. Forever more, COVID-19 will be mentioned concurrently with any discussion about 2020 GDP. Collectively, the world’s annual GDP was about $85 trillion by the end of 2020. But I am confident all 2021 GDP discussions will start with a nod to the blowout 1st quarter GDP growth number, because our ‘current dollar’ GDP grew at the annual rate of 10.7%! Annualized, America’s GDP blew past $22 trillion during the quarter, settling in at $22.05 trillion. The US, the euro zone, and China continue to generate about 70% of the global economic output.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

Why is this concept so important? Because “official” statical releases are typically the only reports that overtly state if the number shown is ‘real’ or ‘nominal.’ Often, an official report will reflect both numbers.

For example, the ‘Gross Domestic Product’ report from the Bureau of Labor Statistics always shows both numbers. In the most recent report for Q1, 2021, the BLS reported that GDP in the first quarter increased at the (annual) rate of 6.4%. Is that a ‘real’ number or ‘nominal?’ The distinction is important.

In fact, it is a ‘real’ number. The nominal number — or ‘Current dollar GDP’ — was actually up by 11% during Q1 – a significantly higher number. During Q1 of this year, the US GDP increased a nominal $566.8 billion over the prior quarter. That’s more than ½ a trillion dollar increase in just one quarter!

The interest rate on US Treasury notes and bonds – in fact, all notes and bonds around the world – is always a “current dollar” yield. Meaning it has not been adjusted for the effects of inflation. So you may be surprised to learn that the ‘real’ yield on the 10-year Treasury, calculated using the most recent inflation data, is now a negative 1.127%

That’s right: After taking into account the effects of inflation, holders of 10-year Treasury bonds actually lose money on their investment. Their ‘real’ yield is actually negative. Pretty amazing, right? Here’s a chart, courtesy of the London Financial Times, since the year 2000:

‘Real’ yields in the eurozone are also trading near all-time lows: The 10-year real interest rate swap — a key gauge of future interest rates across the currency bloc — is around a negative 1.65%.

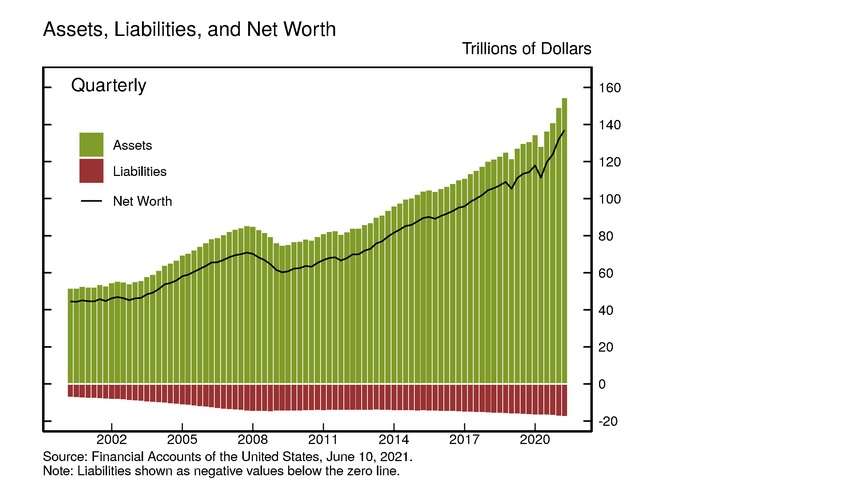

The theme here is consistent: ‘Real’ yields on sovereign debt, across the globe, are generally negative. Why? I’ve talked about this extensively in past blog posts. Essentially, it’s a supply/demand issue. Economists at the International Monetary Fund (IMF) believe ‘global savings’ increase by about $25 trillion every year. This is a staggeringly large number. For context, keep in mind that the ‘net worth’ of all US households, per the Federal Reserve, currently totals about $136.9 trillion. Let me repeat that: This is the combined net worth of all US households. So, clearly, an annual increase of $25 trillion globally is huge. Where can “savers” put all this money? Against that backdrop, it’s not surprising that investment yields have continue to fall year after year, as the chart above demonstrates.

I mentioned the US household net worth above. This is an interesting concept that you can personally track, if you’re interested, by simply googling the ‘Federal Reserve Z.1 report’. I’ll save you a bit of time today. Below is the data chart for the most recent US household balance sheet, courtesy of the FED, reflecting total assets of approximately $154 trillion, liabilities of just over $17 trillion, and an almost $137 trillion net worth:

Earlier today, the yield on the 10-year Treasury was reported around the 1.25% mark. But if you own one of these Treasury instruments, after adjusting for inflation, you should know that your yield is actually negative. Thus, the ‘real‘ yield is negative. Keep this important distinction ‘front of mind’ whenever you read, think about, or review investment opportunities or financial data. Inflation is a real thing – regardless of whether the rate is high or low – and it constantly erodes the value of your cash and investments. So, I suggest you keep it real. Know the difference … and you will know the extent of inflation’s value erosion. 🙂

All this real talk is making me really hungry. Let’s head to the steak houses.

Once again demand is slightly lower this week. Reservations for Saturday in the priciest of steakhouses are more available than in the recent past:

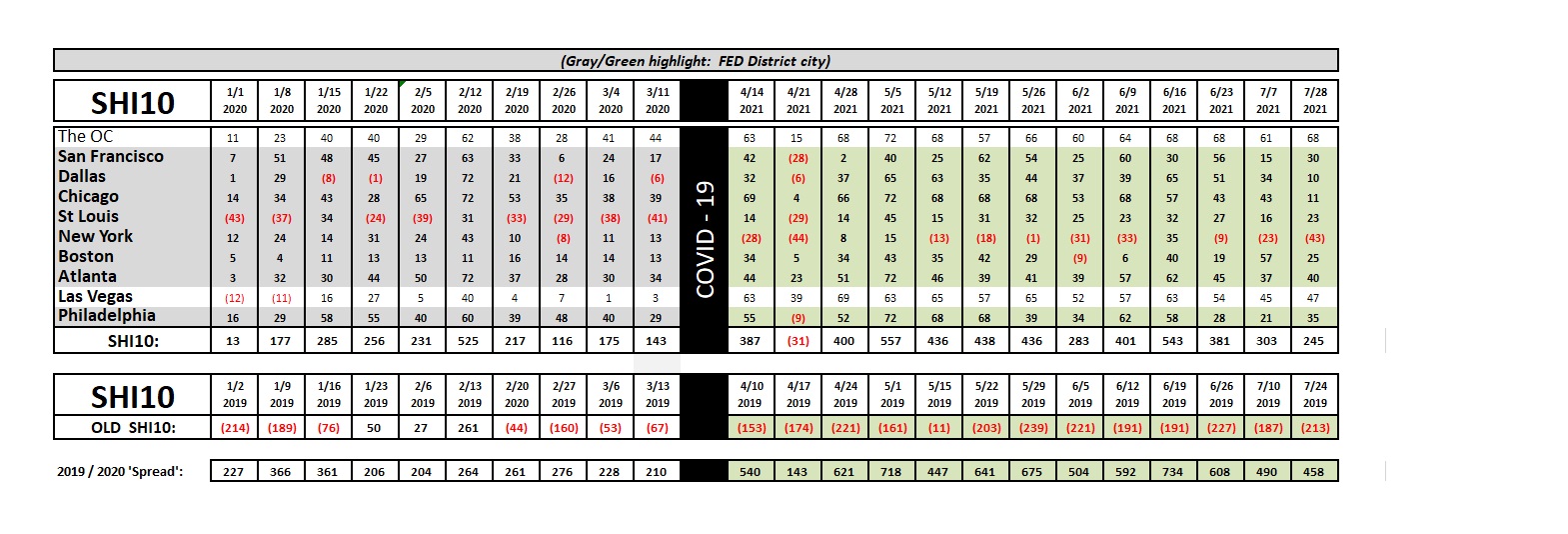

It’s interesting to note that NYC is, once again, back in the red. I hate to make a pun, but as the longer-term trend report below shows, the SHI in NYC is rarely in the black. Is this an economic phenomenon or are expensive steaks just not appealing to New Yorkers? Have the vegans taken over? Who knows, but once again this week, the NYC expensive eatery scene is not well-done. Enough of the bad puns. Here’s the trend report.

The spread remains robust, but week over week demand appears to be waning. It’s too early to determine the accuracy of this comment … let’s continue to watch the trend.

The next official US GDP report – highlighting the “advance” estimate for Q2 – is due out tomorrow morning at 5:30 am Pacific. Once again, economists are expecting a big number. I’m expecting a big number for Q2. I’m sure CNBC will carry the news … so turn on your TV at 5:30 am and see it live!

Or simply google “GDP 2nd quarter 2021” when you roll out of bed to open the latest report from the BEA dated July 29th. Remember that the headline number is ‘real,’ so read deeper into the report to find the ‘current dollar’ figure. I expect the nominal number to be north of 7%.

Finally, it’s worth noting that he FED finished their 2-day meeting and issued their latest FOMC statement. They continue to believe the that “path of the economy” depends on the course of the Coronavirus, that inflation is “transitory,” and that rate policy should remain unchanged. It sounds like the FED believes our economy has made progress toward making progress, but is not sure how much progress, if any, has actually been made.

Confused? Yeah, so am I. I say watch the GDP numbers tomorrow (real and nominal) for a good indicator. That number is solid. Just keepin’ it real. 🙂

<|> Terry Liebman