SHI 5/13/2026 – AI or Die

4.8.26 — Another Look at Private Credit

April 8, 2026

SHI 5.20.26 – Steaks Don’t Lie

May 20, 2026

I just returned from 3 weeks in Europe.

My wife and I traveled from France to Italy and then Spain. And then back to France.

The trip was fabulous. We enjoyed some great food, saw amazing sights, and spent time with many fabulous people in the different towns, villages and cities we visited, soaking in the local culture. We even found a fabulous ‘wine bar’ in Nice, France where the owner was a somm with deep insight into many smaller, lesser-known French wine regions and varietals.

But before we left the US, I was a bit – just a little – apprehensive. How, I wondered, is America perceived in Europe these days? Would my wife and I be warmly received … or … ??? Given all the craziness around the globe today, and the fact that the United States is a common factor in much of it, I was concerned.

So, before heading to Europe, I bought a new hat. That’s right – a hat. A photo of that hat is above. You didn’t know I was a HUGE hockey fan, right? 🙂

It’s true! I bought a hat celebrating my budding fandom in Canadian hockey – specifically the ‘Toronto Maple Leafs.’ And I wanted every European I met to know I was a fan.

OK, you’re right: I really couldn’t give two shakes of a hockey stick about Canadian hockey. But I thought – work with me here – if I’m wearing a Canadian hockey team hat, as opposed to a hat from Disneyland or UCLA, or the Lakers, or something similar, then maybe the Europeans I randomly encountered would think, “Oh, he’s a Canadian.” And if not that, at least the hat might throw them off the scent; at least, they wouldn’t naturally assume I was American. I was hoping to be just a little bit more incognito. After all, sliding thru, unnoticed, would probably be a good thing, right?

“

Everyone loves Canadians!“

“

Everyone loves Canadians!“

And the ploy was working great until I ran into a couple of young guys from Canada. We were walking the streets of Begur, Spain and it happened: With a smile on each of their faces, they maligned my much loved ‘Maple Leafs’! They quickly added their opinion that Montreal’s hockey team was far superior.

I’m guessing I had a very surprised, blank look on my face suggesting I had no idea what they were talking about – because I didn’t. I was lost. I had completely forgotten I was wearing the Toronto hat. Quickly thereafter, one of the guys said to the other, “Oh, he’s a fake.”

Caught. I was a fake. And they quickly figured it out. That was embarrassing.

My point? When buying my “fake hat,” I never considered what might happen if I ran into Canadians in Europe. Duh.

It was pretty easy for those Canadians to “out” me. I mean, really, what do I know about Canadian hockey? I guess I should have taken that into account when I bought my hat. After all, I know Canadians also travel to Europe on vacation.

And this my friends, essentially, is why I write this blog. To help me — and you too — identify as many of the “unknown unknowns” as possible. After all, as I’ve highlighted in past blogs, it’s not the “things we know” that get us. It’s the things we don’t know — the things we don’t even consider — that usually create our greatest challenges. Lesson learned.

Again. 🙂

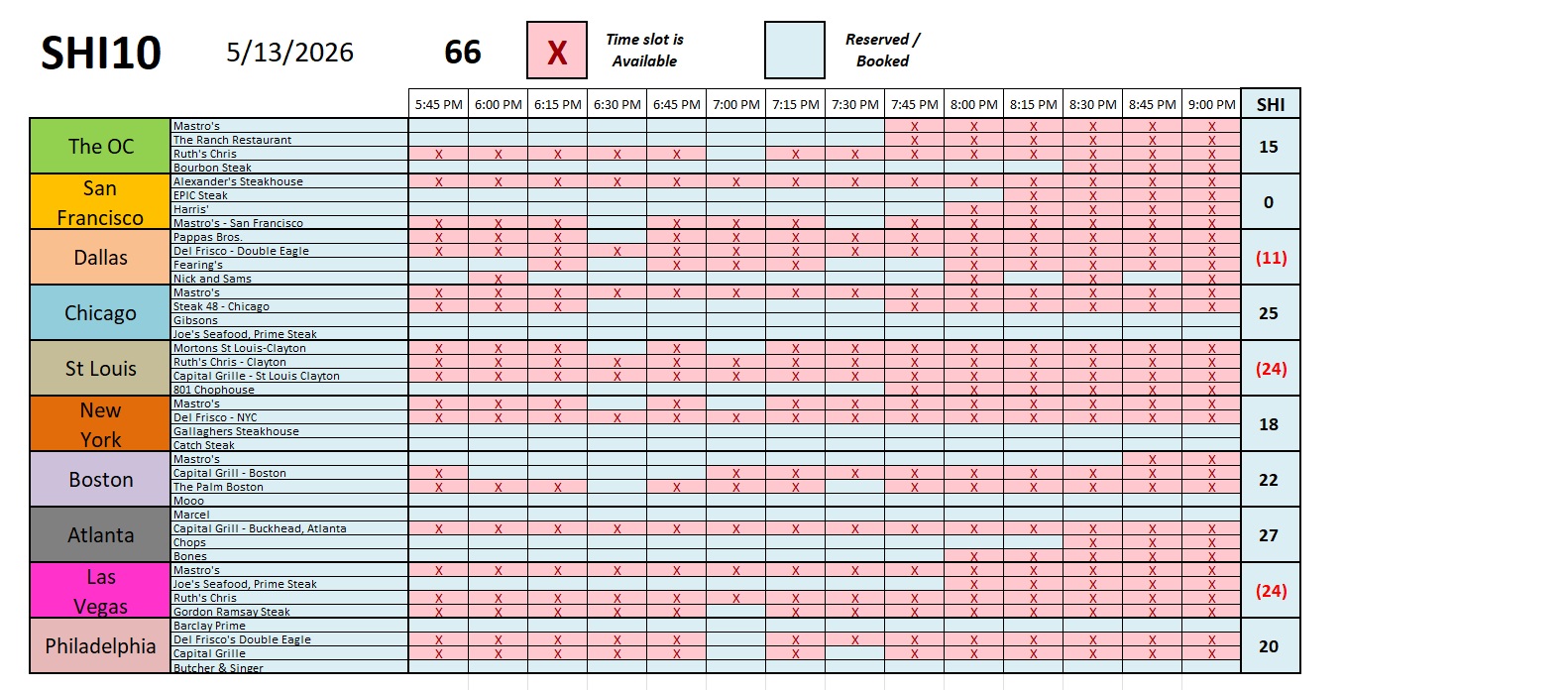

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. But is the US economy expanding or contracting?

Expanding … according the ‘advanced’ reading just released by the BEA, Q4, 2025 GDP grew — in ‘current-dollar‘ terms — at the annual rate of 5.1%.

The ‘real’ growth rate — the number most often touted in the mainstream media — was 1.40%. In current dollar terms, 2025 US annual economic output reached almost $31.50 trillion.

According to the IMF, the world’s annual GDP expanded to over $115 trillion in 2024. Further, IMF expects global GDP to reach almost $135 trillion by 2028 — an increase of more than 28% in just 5 years.

America’s GDP remains around 25% of all global GDP. Collectively, the US, the European Common Market, and China generate about 70% of the global economic output. These are the 3 big, global players. They bear close scrutiny.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

Kristalina Georgieva is the Managing Director of the International Monetary Fund — effectively the head of the organization. As the de facto head of the IMF, she regularly appears on CNBC to comment on global economic risks.

To be clear, she did not use the phrase “AI or die” during her interview. I simply felt her existential angst as I watched her speak. She stated that AI is unavoidable — countries must adopt it or fall behind. If they adopt AI, they will unlock productivity and economic growth; failure to incorporate AI swift enough, or systemically enough, and countries risk economic stagnation.

She did say AI is “hitting the labor markets” like a tsunami – and that most countries and businesses are not prepared for the speed of AI adoption.

What does she mean by these statements? Essentially this: a large portion of the jobs in advanced economies – she believes maybe as many as 2/3 – will be “affected” by AI in some manner. Countries that fail to adequately prepare will experience declining competitiveness.

Perhaps this is no great leap for you. After all, we’ve already seen essentially the same thing within the financial markets: We’ve seen wave after wave of business segments both adversely and positively impacted by the continuous parade of AI features as they roll out. Think of the pain in the SaaS segment and consultants. And the financial exuberance we’re seeing in the stock prices for memory and semiconductor companies.

Bill Ackerman didn’t say “AI or Die” either. However, he did say, “Every company is an AI company today” echoing the IMF Director’s comments, as they apply to companies and our economy over all. And he commented further, “…if you’re not, you’re going to fall behind.”

Interestingly, those realities appear to be playing out. US corporate earnings in the first quarter of 2026 have surprised just about everyone.

FACTSET is a company that tracks this type of thing. On May 8th, they reported, “Overall, 89% of the companies in the S&P 500 have reported actual results for Q1 2026 to date. Of these companies, 84% have reported actual EPS above estimates.”

They further reported, “…companies are reporting earnings that are 18.2% above estimates, which is also above the 5-year average of 7.3% and above the 10-year average of 7.1%.”

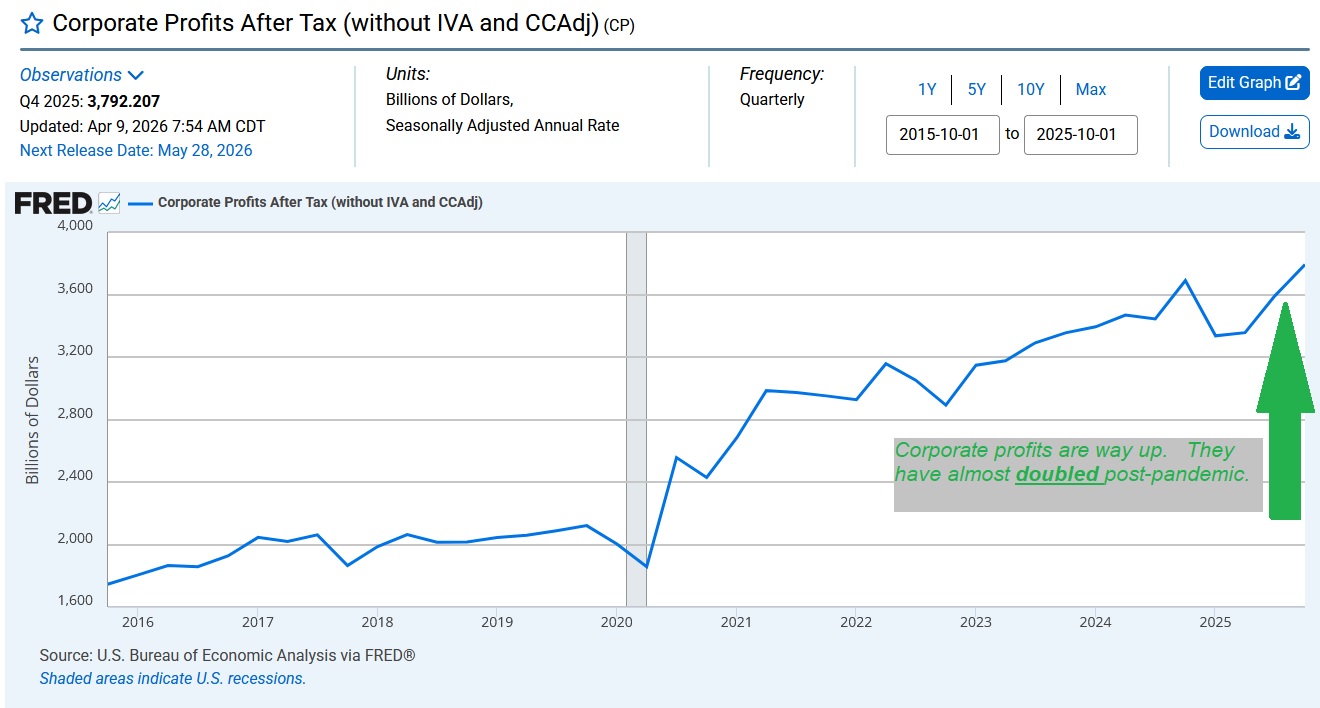

Is this an early manifestation of budding improvements in corporate operating efficiency and productivity? Perhaps. Projected corporate earnings are rising at rates rarely seen in this country in the past 50 years. Here’s a chart showing the growth in US corporate profits over the past 10-years. But the acceleration beginning last year is even more impressive.

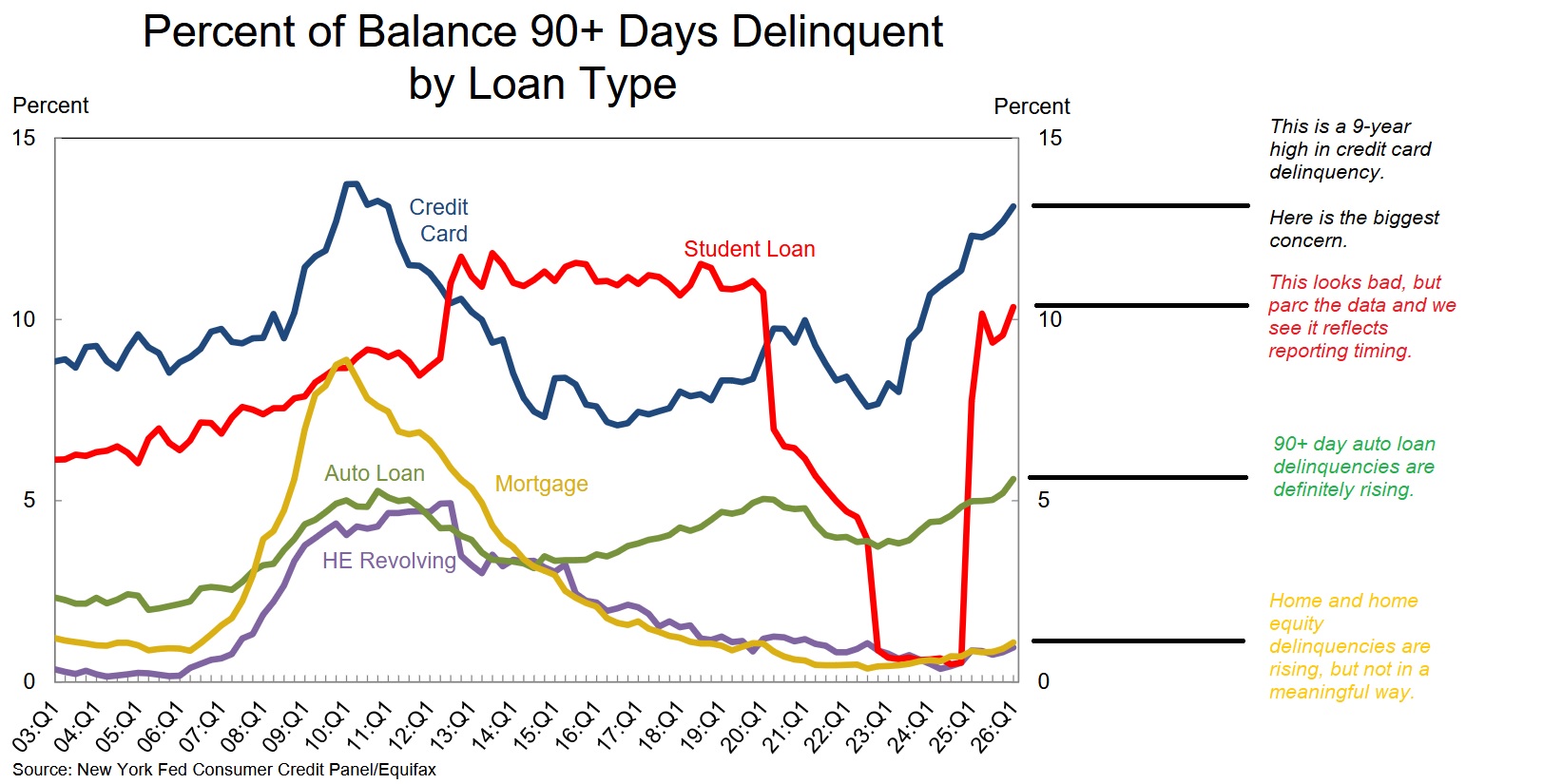

But as the singer Paul Simon once famously quipped, “One man’s ceiling is another man’s floor.” Could the explanation for increasing corporate profits be the result of consumer stress? I suspect many economists might argue that point, especially in light of Tuesday’s report from the New York FED titled “Quarterly Report on Household Debt and Credit, 2026:Q1.” The report shares a credit picture with growing concerns: While aggregate debt levels were stable, 90+ day delinquencies have now reached a 9-year high. The most troubling segment is credit cards.

With a 90+ day delinquency – what the FED calls “serious” delinquency — running 12.7% today, this is a clear signal that the consumer is stressed. For context, three years ago that “serious” delinquency was only 4.57%. The FED has now characterized this condition as a “pointed concern” – a meaningful change from its prior tag, “cautious observation.” The FED is now of the opinion that while the “average” American is doing OK, a sizable “tail” of the population is in a debt spiral.

The FED digs a bit deeper, breaking the US into four geographic quartiles based on median income levels in zip codes. There they find that delinquency in the “bottom income quartile” has spiked to 15%, while the “top” quartile has a serious delinquency rate of just 3%.

It’s easy to understand if we consider that many Americans are paying for “necessities” like groceries or rent with credit cards, often unable to pay off the accumulated debt at the months’ end, and finding themselves stuck with credit card APRs of 25-30%. That sounds like a debt spiral to me too.

Moving the discussion back to the stratosphere, it’s difficult to predict how these dynamics play out. On one hand, early indications suggest that the integration of AI tools into corporate America is generating positive results in profit and efficiency. The biggest companies in the world are collectively spending staggering sums on AI data centers and related CapEx. Companies and countries alike seemingly face existential risks if they fall behind. Most experts seem to agree … this is the new frontier.

On the other hand, some segment of the consumer population is meaningfully stressed today. More than in recent years. The steady, unrelenting growth of 90+ day delinquencies is both clear and ominous. Does this trend have to potential to derail the US economy and nudge us into a recession?

No. I don’t think so. Not yet.

Let’s jump over to the steak houses and see what they tell us.

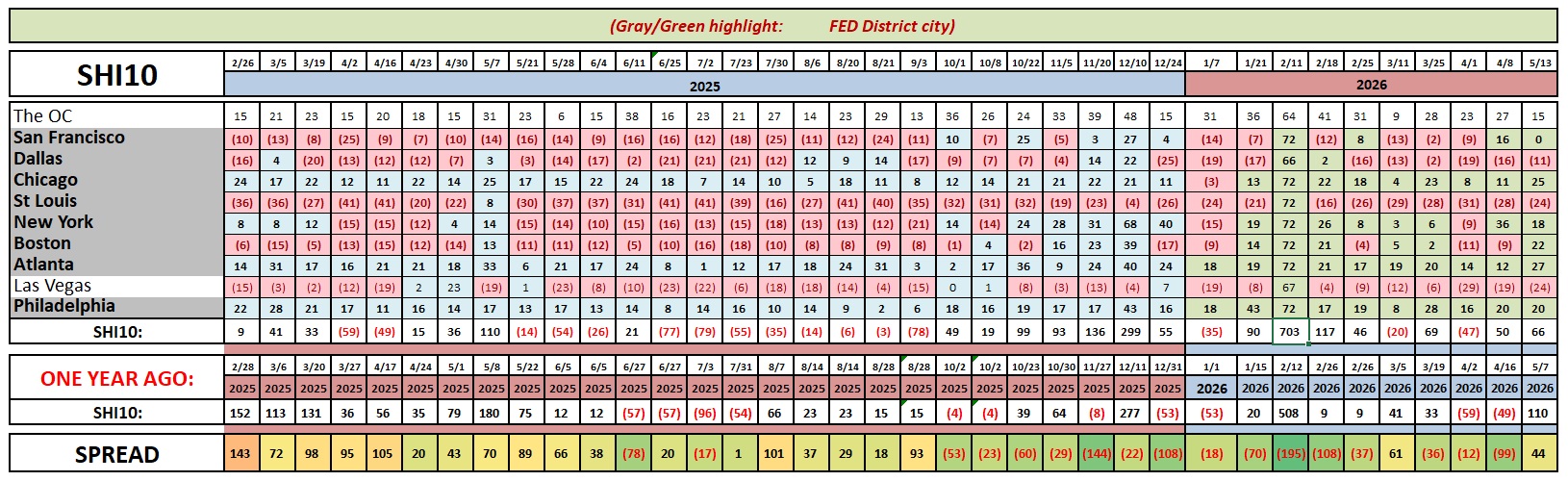

Frankly, there’s not much new here. Reservation demand appears quite stable. Here’s the longer term chart.

I’ve mentione Ed Yardeni in prior blogs. Dr. Yardeni is a Yale PhD in economics and the founder of ‘Yardeni Research’ is he remains quite optimistic about the direction of our economy in the aggregate. He’s not a “permabull” like many other economists. He takes the data as it comes, evaluates it, and presents his well-researched and founded opinions and forecasts from that research.

In his “Yardeni Quicktakes” update from last week, he suggested, “We have nothing to fear but nothing to fear.” Hmmm…OK, got it.

But I think we have plenty to worry about, doc. Conflicts abound! The world is a messy place right now. Regardless, I do agree with his comments about the “fearless consensus of industry analysts” who have the job of forecasting US economic performance and corporate profitability.

Dr. Ed’s comment on the analysts:

They raised their earnings growth expectations for 2026 that month and continued to do so, up to 21.4% currently. They’ve also been raising their expectations for the level of 2027 earnings, but the growth rate for next year has declined in recent weeks to 16.9% simply because this year’s upward estimate revisions have been so strong! That’s mostly because companies have beat their estimates during Q4-2025 and now Q1-2026.

He calls the earnings beats and growth a “melt up,” further commenting, “The latest earnings results and CEO commentary leave no doubt that American consumers continue to spend.” Perhaps.

Moving from the stratosphere back to ‘ground level’ for a moment, earlier today the Federal Reserve Board released their annual survey and report titled Economic Well-Being of U.S. Households in 2025. The survey, completed in October of 2025, polled about 12,000 adults. The results indicate that overall American’s believe the labor market remained “solid.” Price increases remained the most common financial concern. Unsurprising. That said, 73% of the adults polled reported they were either doing OK or living comfortably. Interesting. One of the most enduring questions in the survey asks if the respondent could pay for an “unexpected $400 expense” with cash or the equivalent. 63% said they could. This number is unchanged from the prior year. Again, interesting.

To read the report,

CLICK HERE

Ultimately, I believe the direction and future of the US economy is determined by trends that are systemic rather than important. The evolving trends within the credit space are important, but they are not systemic. The AI spending boom, measured in trillions of dollars over several years, is systemic – even transformational. As are the implications to countries and businesses.

Consumer spending, of course, is a systemic driver of GDP growth. History has shown that credit problems will blunt consumer spending over time. However, as spending propensity spreads across all income quartiles, and as America’s net worth (as reflected in the FED z.1 report) is downright staggering: The March 19th report shows household net worth reached $184.1 trillion in Q1 of last year, propelled by growing real estate and stock market valuations. Half of that amount is owned by our 64 million ‘Baby Boomers.’ Both empirical and anecdotal evidence suggest they are spending plenty of that wealth as they enjoy their retirements.

Feel free to worry about the economy. I do — it’s a complex beast. But I remain convinced that we remain on solid footing over all. 🙂

<( Terry Liebman )>