SHI 3.2.22 – Rising Uncertainty … Uncharted Waters

SHI 2.23.22 – Keep Calm and Don’t Panic

February 23, 2022

SHI 3.9.22 – The Problem with Forecasting

March 9, 2022

My grandfather was born in Ukraine.

Fortunately for me, his family chose to emigrate to the United States around 1900, making my father a first-generation American by birth. Even more fortunate for me, my father chose to settle in California after leaving the Army, making me a first-generation Californian by birth.

I am certain I have many relatives in Ukraine. I’ve never met them, and don’t even know their names, but neither fact diminishes my admiration for the people of Ukraine and their bravery in the face of overwhelming adversity, my personal condemnation of Russia’s senseless invasion and targeting of civilians, and my hopes for a quick end saving many lives and futures.

But as this is a economic and financial blog, my remaining comments will view current event thru an economic lens.

“

Russia’s invasion fosters economic uncertainty.”

“Russia’s invasion fosters economic uncertainty.”

And financial markets hate uncertainty.

In a world where information is instant and ubiquitous, it’s easy to see that almost everyone universally condemns Russia’s attack of Ukraine. The big standout, perhaps not surprisingly, is China. But I think they have another agenda. I’ll discuss that later. For now, let’s focus on current events and the resulting uncertainty that is roiling the stock and bond markets, here and abroad, jet-fueling a spike in the prices of global commodities, almost certainly pushing up inflation, and making the FEDs job far, far more difficult and throwing doubt on the continued expansion of our economy.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. Significantly. During 2021, nominal growth clocked in at $2.1 trillion. The US annual economic output was just under $23 trillion for the full year. The world’s annual GDP rose to about $95 trillion at the end of 2021. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

So often in this blog, I’ve repeated the phrase, “May you live in interesting times …”

Let’s see … in just the past few years we’ve experienced negative interest rates during a global pandemic, which resulted in widespread closures and economic distress, triggering massive monetary and fiscal response that dumped unprecedented liquidity into world economies while, at the same time, supply chains broke down, causing supply/demand disruptions, massive price spikes, CPI inflation levels unseen for more than 4 decades, corporate profitability at levels not witnessed since the last century, and, finally, an invasion and land war in eastern Europe — something the world hasn’t witnessed in almost 80 years.

Did I miss anything? 🙂

Yeah, I probably did. May we live in interesting times indeed.

Countries around the world are almost universal in their condemnation of Russia, which is taking the form of severe economic sanctions against Russia and military assistance for Ukraine. Even Switzerland, the ‘neutralist’ of all, has condemned Russia and frozen Russian bank accounts. All of which begs the question, at least for the purpose of this blog,

What does this all mean for the US economy?

As the barrel price of WTI approaches $110 while I write this blog, I can honestly answer who knows? Sure, until today, I’ve remained somewhat optimistic about the direction of the US economy. GDP growth in 2021 was stellar — absolutely spectacular. I did not expect a repeat in 2022. But I did expect GDP growth above trend. Now, as the final month of Q1, 2022 begins, I am increasingly concerned about the headwinds. With all the variables floating around in today’s economic calculus, accurately predicting a near-term result or direction is impossible. That hasn’t stopped many economist from making predictions. But I feel the word ‘accurate’ is important here. I can’t see how any forecast right now could possibly be accurate.

For example, what impact does a $10 per barrel increase in the price of oil have on an-oil importing economy? According to Again Capital, a $10 per barrel price increase increases the daily cost for oil by:

= > Japan: $25 million

= > India: $40 million

= >China: $110 million

Permit me to repeat the important part: This is the daily cost increase to those nations. In other words, each of these nations are now importing a whole lot of inflation and a drag on their GDP. Remember that imports have a negative impact on GDP. Exports are positive … imports are negative. And since the per-barrel price of oil hasn’t increase only by $10 … but more like $50 per barrel since late last year, these countries will struggle economically. China’s economy is taking about a half-a-billion-dollar hit each and every day.

That’s a billion every 2 days … or $3 1/2 billion a week. Sure, they are a $17 trillion economy, but at this price, their economy will pay a steep price.

Ironically, from a GDP perspective, the oil price increase here in the US is relatively neutral. Are you shocked? Sure, everyone will pay more at the pump, more for heating oil, and businesses will pay more for energy, but in 2020 the US became a “net annual petroleum exporter” according to the EIA. Which means, on balance, rising oil prices is a net positive for GDP if not for its inflationary effects. Even if a rising price of oil boosts the nominal GDP, a rising CPI would increase the ‘deflator’ when real GDP is calculated. Thus, on the whole, rising or falling oil prices have a relatively neutral impact on real US GDP these days. Our economy has come a long way since the oil shocks of the 1970s.

Another global inflationary shock from Russia’s invasion will be felt in food prices. Ukraine — and Russia for that matter — is a huge wheat exporter. With that export in doubt, wheat prices — like oil — are way up. Pile this likely price increase on top of the meatpacking plant price increases highlighted in Biden’s “State of the Union” address last night, and we see some serious headwinds to food-related CPI increases in coming months. Checking out at the grocery store is likely to cost even more.

So … gas prices are heading up … food prices are heading up … and interest rates are heading up. In testimony in front of the House earlier today, Chairman Powell suggested that he supports a 1/4% FED funds rate increase in March. Expect one. It will happen.

And finally, we have the FEDs ‘Beige Book’ also released earlier today. Of note on this topic:

Prices charged to customers increased at a robust pace across the nation. A few Districts reported an acceleration in prices. Rising input costs were cited as a primary contributing factor across a broad swath of industries, with elevated transport costs particularly significant. Labor cost increases and ongoing materials shortages also contributed to higher input prices.

Firms reported an increased ability to pass on prices to consumers; in most cases, demand has remained strong despite price increases. Firms reported they expect additional price increases over the next several months as they continue to pass on input cost increases.

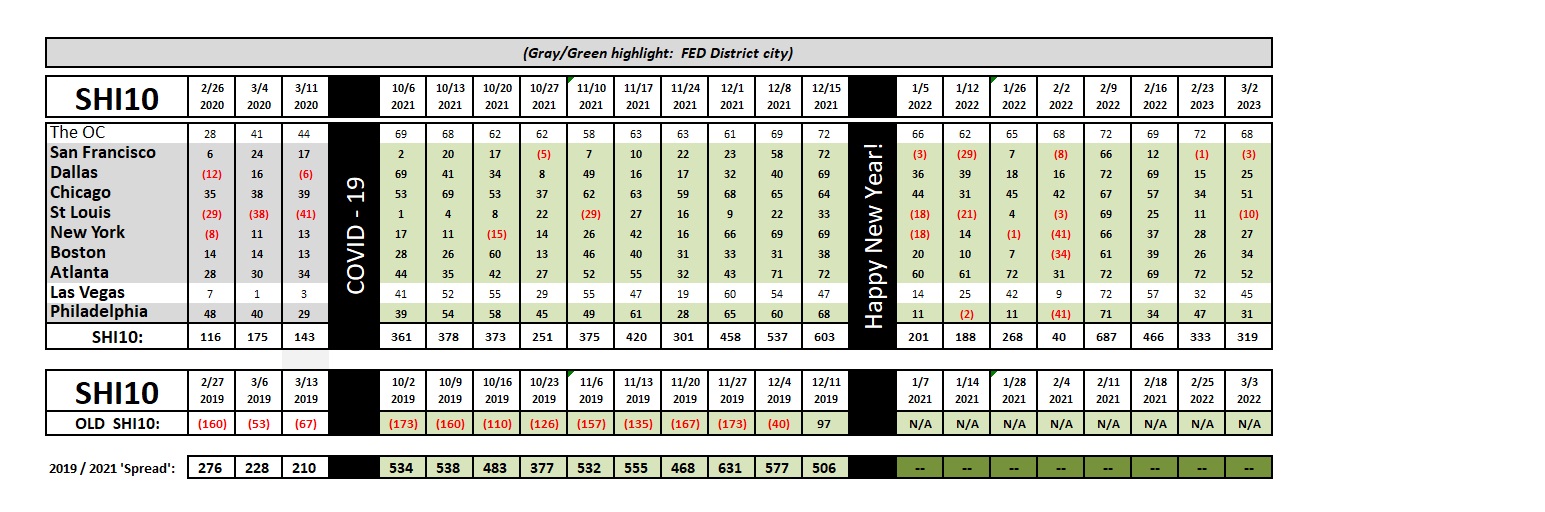

In summary: Prices are up … prices are going up … and corporate profits are up. The consumer is beat-up, causing us to wonder if they can continue levels of “consumer spending” needed to support the US economy. Remember, they are 70% of the whole game. Will GDP also maintain its positive growth trend from last year? The jury is definitely out today. Let’s see what the steakhouses are telling us. Here’s the trend report:

Well, so far, reservation demand at our pricey restaurants remains robust. That “dinner-for-4” at Mastros that cost $400 last year is probably costing $500 today. But our expensive eateries remain in high demand. By their behavior, affluent eaters and consumers remain optimistic and positive. Here’s the weekly SHI10 report:

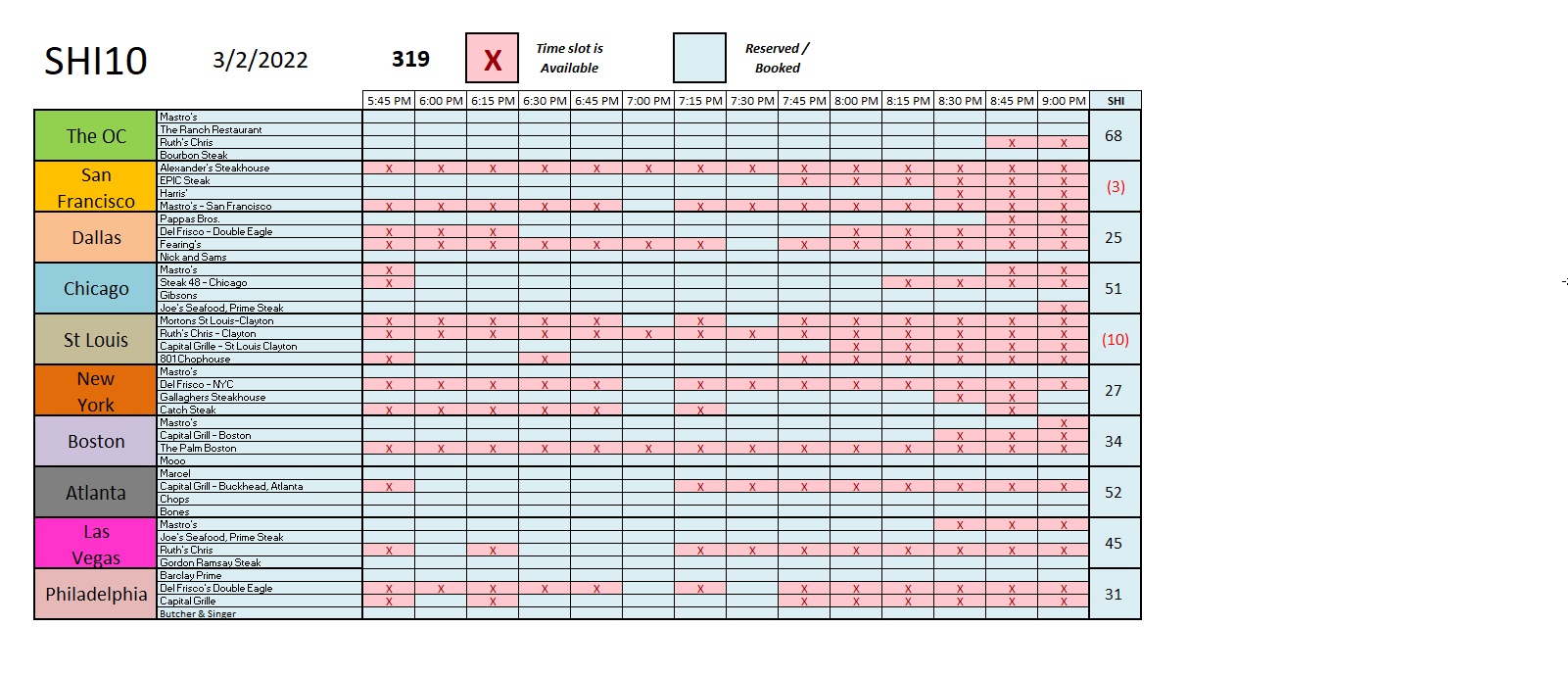

Steak lovers here in the OC have yet to put down their knives and cancel reservations for this Saturday. Only 2 open reservation slots remain. Demand is more mixed across the country, but an overall SHI10 reading of 319 remains robust by historic standards.

Today I make no predictions — beyond a 1/4% rate FED funds rate increase in March. Our economy faces legitimate headwinds today. Can real GDP continue to grow in these conditions? Stay tuned! And good luck, Ukraine.

<:> Terry Liebman