Reading the Tea Leaves

The May 18 Steak House Index Update

May 18, 2016“Nowcasting” the GDP

May 20, 2016The FED speaks … and the markets react.

On the 18th, the FED released the ‘minutes’ from their April meeting. Want to read them? Here you go:

https://www.federalreserve.gov/monetarypolicy/files/fomcminutes20160427.pdf

Why you should care: The US stock and bond markets moved meaningfully after the minutes were made public. Stocks down, bonds yields up. It’s been said, “Don’t fight the FED…” because you will lose. So we must pay close attention to FED commentary, thoughts, discussion. But what did they say … and what does it mean?

Taking action: The FED raises rates to intentionally slow US economic activity. To reduce GDP growth. To slow inflation. To slow labor growth. ‘Quantitative Easing’ is a condition intended to grow all these things. Increasing interest rates is intended to have the opposite effect.

If you’re an investor, consider the thoughts below…as you make investment decisions. If you’re a business owner, develop your own strategic plan for your business if the FED does move the interest rate. In other words, be informed. And be prepared.

THE BLOG: Every sophisticated investor on the planet watches the FED for signs. Everyone. Because they should.

The question on everyone’s mind: Will they raise rates in June? What might prompt such a move? And what will happen as a result?

The FOMC minutes, released on the 19th, gave us deeper insight into their thoughts and discussions. On page 12, the members summarized their feelings:

“Most participants judged that if incoming data were consistent with economic growth picking up in the second quarter, labor market conditions continuing to strengthen, and inflation making progress toward the Committee’s 2 percent objective, then it likely would be appropriate for the Committee to increase the target range for the federal funds rate in June.”

Reading this, many investors concluded a FED June rate increase is back on the table. Let’s explore a bit more.

We have an “if/then” statement from the FED. The three (3) ‘ifs’ are:

- a pick-up in economic growth;

- a further increase in inflation toward the 2% target; and,

- further strength in labor market conditions.

Interesting. Does this look precise to you?

Well, not to me. Other than the 2% inflation target, no numbers are mentioned. In fact, even that metric is not specific. They used the qualitative word “progress” even here.

Which is the problem with reading these particular tea leaves. They really don’t say anything – at least nothing with any level of precision. In other words, the minutes are not an assurance of a rate hike … nor are they an indication of high probability. They simply state the obvious: An increase is possible.

The FED remains data dependent.

Which means we need to look at the data. Let’s start with labor. Yes, this market is firming. Sort of. I used this graphic in a prior blog, but let’s revisit it:

The theory is once the unemployment rate falls below the ‘natural’ rate of unemployment, the labor market will shift from excess labor into labor shortage. As students of economics, we all know that when this happens the price of “the thing” where demand exceeds supply will go up. Makes sense.

But will we really be in a shortage situation? If the official unemployment rate falls below 4.8%, are we truly in a labor shortage situation?

I copied the graph below from the most recent “US Economy in a Snapshot” released by the NY FED earlier today. Take a look:

OK…yes, the unemployment rate (the blue line…measured against the left axis) has fallen significantly. Excellent. But take a look at the gold line, measured against the right axis. This line, the “Employment to Population Ratio”, tells a different story.

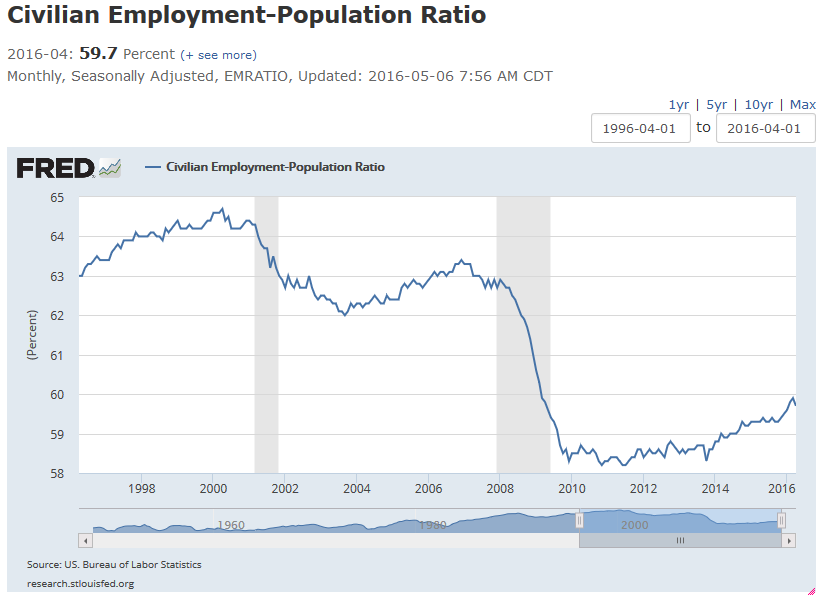

Here’s a 20 year history of this metric, again provided by our friends at the St. Louis FED:

The most recent peak – December of 2006 – was a ratio of 63.4%. The trough, December of 2009, was 58.3%. Said another way, 58.3% of “working age labor force” (age 16 to 64) was gainfully employed in December of 2009.

Today? We’re up to 59.7%. A full 3.7% below the most recent peak in 2006. So, are we at – or almost at – the full or ‘natural’ employment rate?

I say no. Public commentary aside, the FED must know this – and must consider this as they make their decision in June. To me, the labor data still indicates NO CHANGE in interest rate policy.

OK, how about inflation? Well the CPI (all items) is moving up. Excluding “food and energy” to find ‘core’ inflation, the 12-month period ending April of 2016 showed a 2.1% increase. Including food and energy, a 1.1% increase. Will the CPI increase further in the next few months? Almost certainly. Why? Energy.

In the last year, the energy component of the CPI has decreased in ‘cost’ by 8.9%. As the per barrel cost of oil went down, do did our energy cost. Right? Cheaper gas? And that effect is now, somewhat, reversed. So the CPI will be increasing further in coming months.

The FED, however, puts more stock in the changes in the PCE, the “personal consumption expendature” measure. During 2015, the ‘core’ PCE increase – for the firest 10 months – was 1.3%. In November and December: 1.4%. And in January and Feburary, of 2016, it increased to 1.7%. But in March, it fell back to 1.6%.

And the ‘all-items’ PCE has been above 1% only 1 month of the last 15! Once again, to me, the inflation data still indicates NO CHANGE in interest rate policy.

I’ve talked extensively about my belief that GDP growth will remain below trend. I expect this to continue. Even the BEA feels GDP growth will remain ‘below’ potential thru 2020 – trending at 1.8% per year:

Absent a rapid acceleration in GDP growth, once again the FED has no compelling reason to increase rates. Once again, I don’t see it. GDP data still indicates NO CHANGE in interest rate policy.

Of course, it’s possible we could see rapid and significant improvement in some or all of these metrics. Let’s watch closely. But I think this is unlikely.

And don’t get me started on what’s happening over seas! If the FED brings data from Europe (the EU), China and Japan and into the equation, a US rate increase definitely is not in the cards. Not in June.

- Terry Liebman

2 Comments

[…] ← Reading the Tea Leaves […]

[…] https://terryliebman.wordpress.com/2016/05/19/reading-the-tea-leaves/ […]