SHI 06.27.18 Out of Alignment

SHI 06.20.18 Just Ship It

June 20, 2018DO NOT OPEN LINK

July 4, 2018

“The US stands alone. In at least one respect.”

As you know, the majority of my focus tends to be on the US economy. And while our economy remains the foundation for global finance, economics and supply chains, the trajectory of the US economy is also affected by the economies of other developed nations. Today, no developed nation is self reliant.

US economic results are impacted by the health of our economic trading partners. Just as they are impacted by ours. Perhaps even more so given the negative trade balance President Trump has brought to the forefront of US consciousness in the past few months. We import a lot of stuff from other countries. Just think about all the German cars you see on the road.

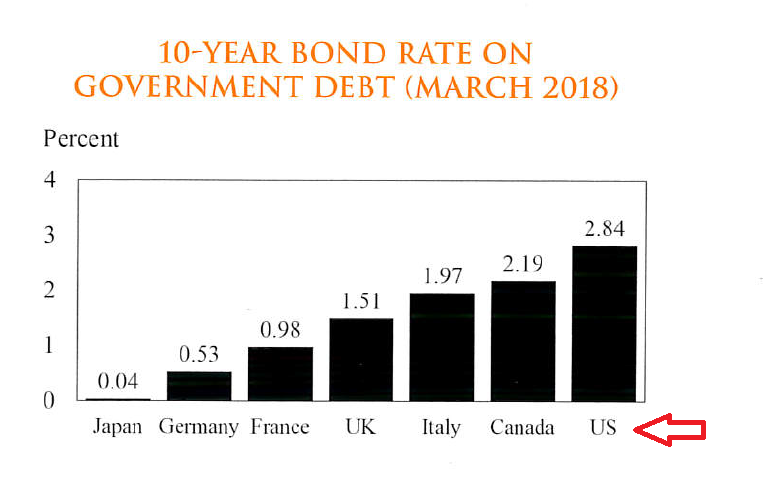

Below is a nice chart I took from the “40th Anniversary “Economic and Business Review” produced by Chapman University in June of this year:

The chart shows the 10-year bond rates for the countries shown from earlier this year. Japan is right at zero. And the US 10-year Treasury rate is at the other end of the spectrum.

We arguably have the largest, strongest economy on the planet … which suggests our debt should be both the lowest risk and sold at the lowest rate … but the opposite is the case. Our debt is sold at the highest rate compared to our trading partners above.

Moody’s is a credit rating agency. They have rated US debt as “Aaa” — the highest possible rating. The UK has the same credit rating as the US. And they have a 10-year bond rate about 1/2 of ours. Japan, on the other hand, is rated “Aa3” — three ‘rungs’ lower than US and UK debt. Yet the Japanese 10-year rate is effectively zero.

And then we have Italy. A beautiful country where wine flows like water. Their Moody’s credit rating is “Baa2.” This rating is only two levels above “Non-investment grade. Speculative.” And 8 rungs below the US debt rating. Their debt is almost classified as “junk.” Yet their 10-year yield is below 2.00%. Almost a full percentage point below the US rate.

To me, this is really odd.

Why is this important? For many reasons. I’ll talk more about this in the blog.

The FED has suggested they will raise rates three (3) more times this year. I don’t think they will. We may have 1 more rate increase in our future … but I believe that’s it. Global economic conditions will impact future FED rate decisions. Current global growth trends may cause the FED to cease rate increases sooner than they are presently suggestion. Which I believe would be a good thing:

- US GDP growth is strong right now. But economies in the EU, Japan, Germany and the UK may be slowing a bit.

- ‘Quantative Easing’ by the ECB continues in Europe.

- The Japan picture remains hard to explain. Many of their interest rates remain below zero. The 1-week ‘Tokyo interbank offered rate,” known at TIBOR, is just a sliver below zero.

- Emerging markets, smaller economies heavily reliant on the USD for funding, are struggling.

The bottom line: Our economy is strong. But we stand alone.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will continue to be true for years to come.

Is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is almost $80 trillion today. US ‘current dollar’ GDP almost reached $20 trillion during Q1, 2018. We remain about 25% of global GDP. Other than China — a distant second at around $11 trillion — the GDP of no other country is close.

The objective of the SHI10 and this blog is simple: To predict US GDP movement ahead of official economic releases — an important objective since BEA (the ‘Bureau of Economic Analysis’) gross domestic product data is outdated the day it’s released.

Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric.

The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

To me, the whole interest rate thing is a bit odd.

Think of a country credit rating like your FICO score. The higher the FICO score, the theory goes, the lower your cost of borrowing. The US has one of the highest possible credit scores, and we pay the highest cost for our debt. This is definitely odd. Why?

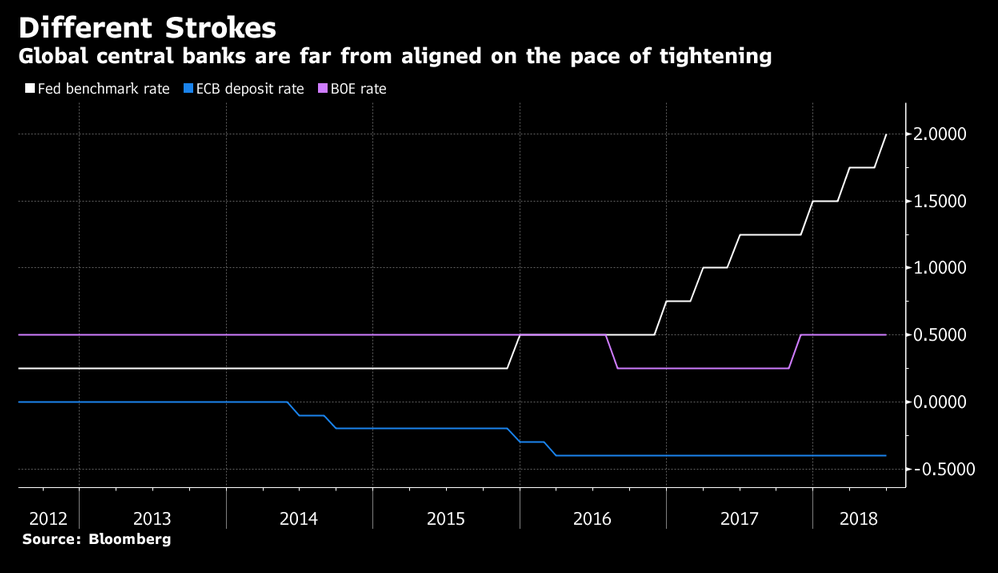

It’s also interesting to note US central bank rate increases are NOT being duplicated elsewhere. In fact, the opposite is true. During much of the time the FED has been raising the benchmark rate, the European Central Bank (ECB) and the Bank of England (BOE) have actually been reducing rates:

Again, why?

I believe US 10-year debt is more expensive because of our annual deficit. In 2017, the deficit (as a % of GDP) was about 3.5%. This fiscal year it may eclipse 5%. Ouch. The European Union deficit (collectively), by comparison, was less than 1%. The buyers of our debt are a little worried. Not too much, mind you, but just a bit. Frankly, I think buyers of Italian 10-year debt should be far more worried. But according to the OECD, their 2017 annual deficit was only about 2.3% of their GDP.

So which country’s debt subjects the owner to greater risk? Italy or the US? Hmmm……

Ironically, FED rate hikes increase the US annual deficit. Over time, every 25 basis point FED rate increase results in about $40 billion more in annual interest on US debt. Meaning the 7 rate increases since the end of 2015 is likely costing the US Treasury about $280 billion more each year. Ouch again.

This notwithstanding, I continue to believe US 10-year debt is over-sold. There are as many reasons for the 10-year rate to fall as rise in the next 6 months.

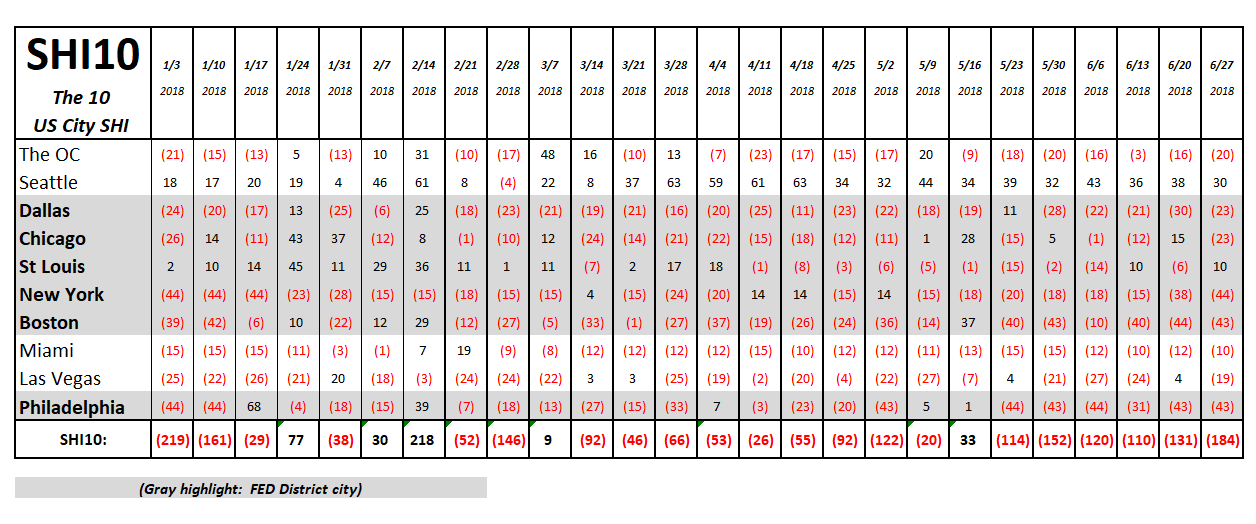

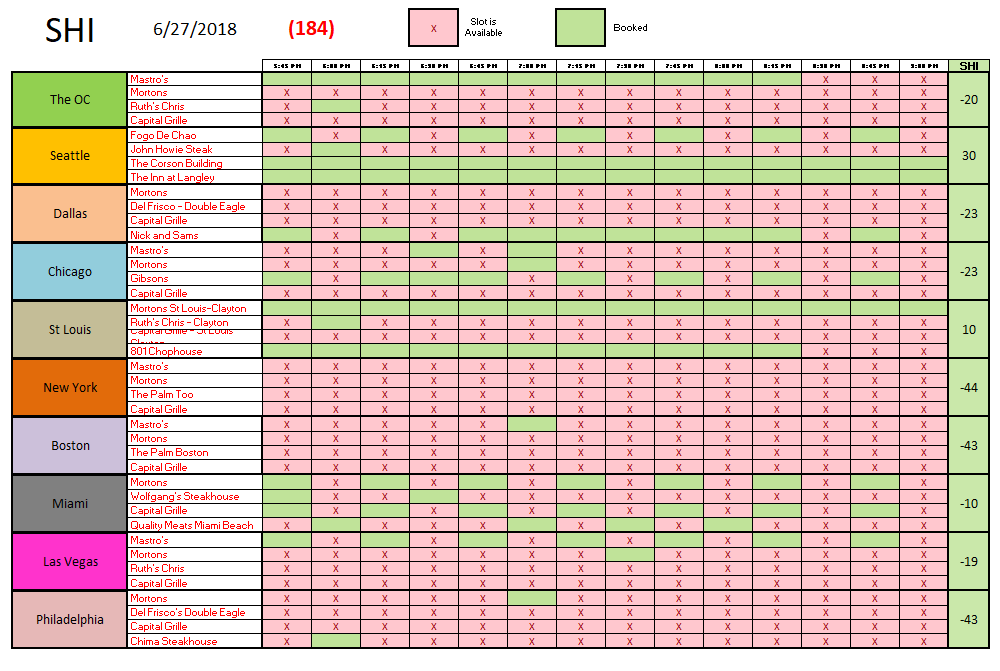

Let’s move to the steak houses! Wow … reservation demand at our pricey eateries has certainly fallen this week:

Demand remains fairly consistent here in the OC and St Louis demand has picked up a bit.

But expensive steak house reservations this Saturday night have plummeted in Chicago and Las Vegas … and NYC, Boston and Philly remain at or near the lowest possible SHI level. Once again, the story the SHI10 is telling is not a pretty one. This week’s SHI10 reading — a negative 184 — is the lowest reading we’ve seen since January 3rd. Here are this week’s results:

It’s interesting. On one hand, the Atlanta FED is forecasting smokin-hot GDP growth for Q2: 4.5% in their latest GDPNow reading from earlier today. On the other hand, the SHI10 is predicting solid, but more tepid, growth, likely in the 2s.

Who is right? Which prediction will prove to be more accurate? The excitement is palpable! 🙂

Well, maybe not. But it’s certainly interesting. Thanks for tuning in.

- Terry Liebman