SHI 07.25.18 Where’s the Beef?

SHI 07.11.18 Will the FED Quit Early?

July 11, 2018I Have No Beef Here!

July 27, 2018

“Right here. Take a closer look at the photo.”

Beef in warehouses is piling up. According to the USDA, red meat and poultry stored in ‘cold-storage’ warehouses tipped the scales at 2.5 billion pounds in June. Just slightly below the all-time record. Because of increased production and reductions in exports, the US is swimming in frozen beef.

Are steak houses simply not selling enough T-Bones? Have high-priced steaks lost their sizzle? Why am I grilling you like the? Will the bad puns ever end?

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will continue to be true for years to come.

Is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is almost $80 trillion today. US ‘current dollar’ GDP almost reached $20 trillion during Q1, 2018. We remain about 25% of global GDP. Other than China — a distant second at around $11 trillion — the GDP of no other country is close. The objective of the SHI10 and this blog is simple: To predict US GDP movement ahead of official economic releases — an important objective since BEA (the ‘Bureau of Economic Analysis’) gross domestic product data is outdated the day it’s released. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

Nope. That’s not it. As you’ll see below, our steakhouses are doing just fine.

But don’t let anyone tell you business is easy. Buoyed by a stronger US economy and rising incomes in Asia and Latin America, demand for beef increased here and internationally. Seeing opportunity, farmers, ranchers and meat-packers expanded facilities to meet demand. The USDA is predicting the industry will produce a record 102.7 billion pounds of meat this year.

“The more you store, chances are you’re going to have to export more of it,” said Altin Kalo, a commodity analyst with Steiner Consulting Group. “Even with the tariffs, there’s only a certain amount of product you can shift into the domestic channels.”

So, it’s not a domestic demand problem. It’s an export problem. Supplies are piling up … and so are the pallets of frozen meat at Zero Mountain in Arkansas. So what’s a farmer or rancher to do?

Apparently, they can borrow money from, or sell their products to, the USDA.

According to Dan Glickman, Agriculture Secretary during the Clinton administration, there are several statutes available to the U.S. Department of Agriculture that could be used to help farmers, including programs through the Commodity Credit Corp. The CCC, a federal agency set up during the Great Depression, could potentially buy surplus farm products and support growers.

Tariffs are already restricting exporting and sale of US agricultural products. Farmers and ranchers are hurting. The US can — and may — buy the “surplus” to help. What a mess.

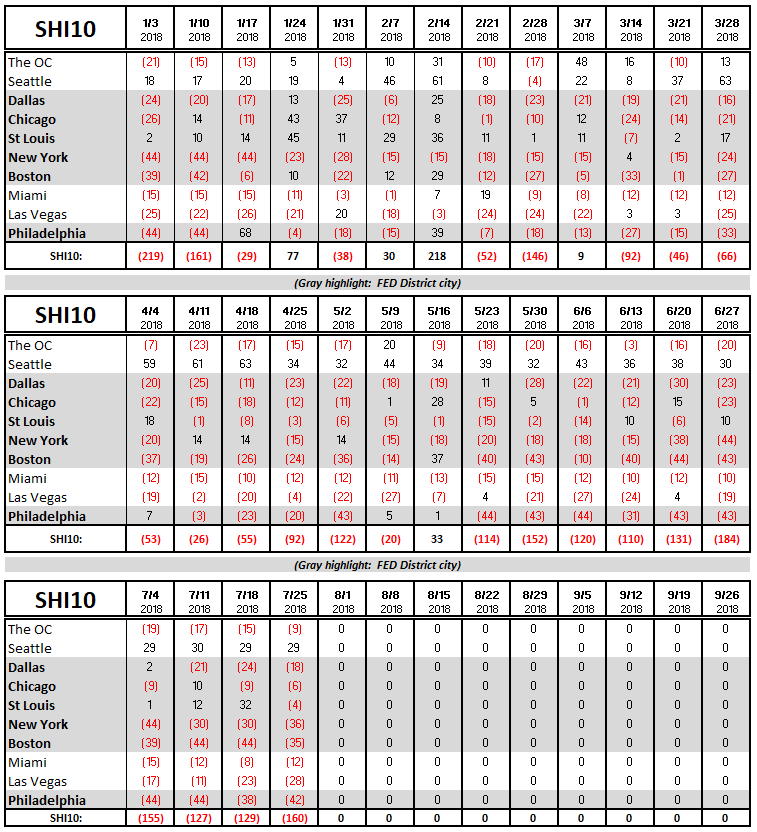

On the other hand, you could help and eat more steaks. Go ahead: Make a reservation at your favorite steakhouse. Speaking of the steakhouse, let’s see how they’re doing this week. Below is the long-term trend chart. Notice the number for July 18th — when I was on vacation — are now shown:

The numbers are fairly consistent. SHI markets where reservation demand is typically light continue to follow that trend. And cities where expensive steaks are in vogue — such as Seattle, Chicago and St. Louis — continue to reflect strong steakhouse reservation demand.

I find the SHI results in NYC, Boston and Philly to be quite interesting. Clearly, weak steakhouse demand is not the result of a weak economy. A quick review of the most recent FED ‘Beige Book‘ confirms this fact. Here are the city ‘highlights’ from the Beige Book published on July 17th:

- New York

The regional economy continued to expand at a moderate pace, and labor markets have remained tight. Input price increases have remained fairly widespread, and selling prices continued to increase moderately. Housing markets have continued to firm, on balance, while commercial real estate markets have softened a bit.

- Boston

Business activity continued to expand at a moderate pace, with contacted manufacturers, retailers, hotels, and software and IT firms reporting year-over-year increases in revenues. Some contacts saw higher prices and lower margins. Contacts reported difficulty hiring in skilled occupations.

- Philadelphia

Economic activity continued to expand at a modest pace. With tightening labor markets, job growth also remained modest, but wages are now rising moderately. On balance, contacts continued to observe modest price increases with few concerns for future inflation. Notably, nonresidential construction activity has begun to decline from its prior high levels.

In each city, economic activity is expanding. Labor markets are tight. Given these facts, one would expect greater steakhouse demand. I wonder if the weak reservation demand we see on SHI10 Wednesday reflects (1) lack of early demand (meaning, by Friday these restaurants are booked), or (2) if these cities simply have a much larger pricey restaurant supply than the other cities we track. Odd. Feel free to share any thoughts you may have on the topic.

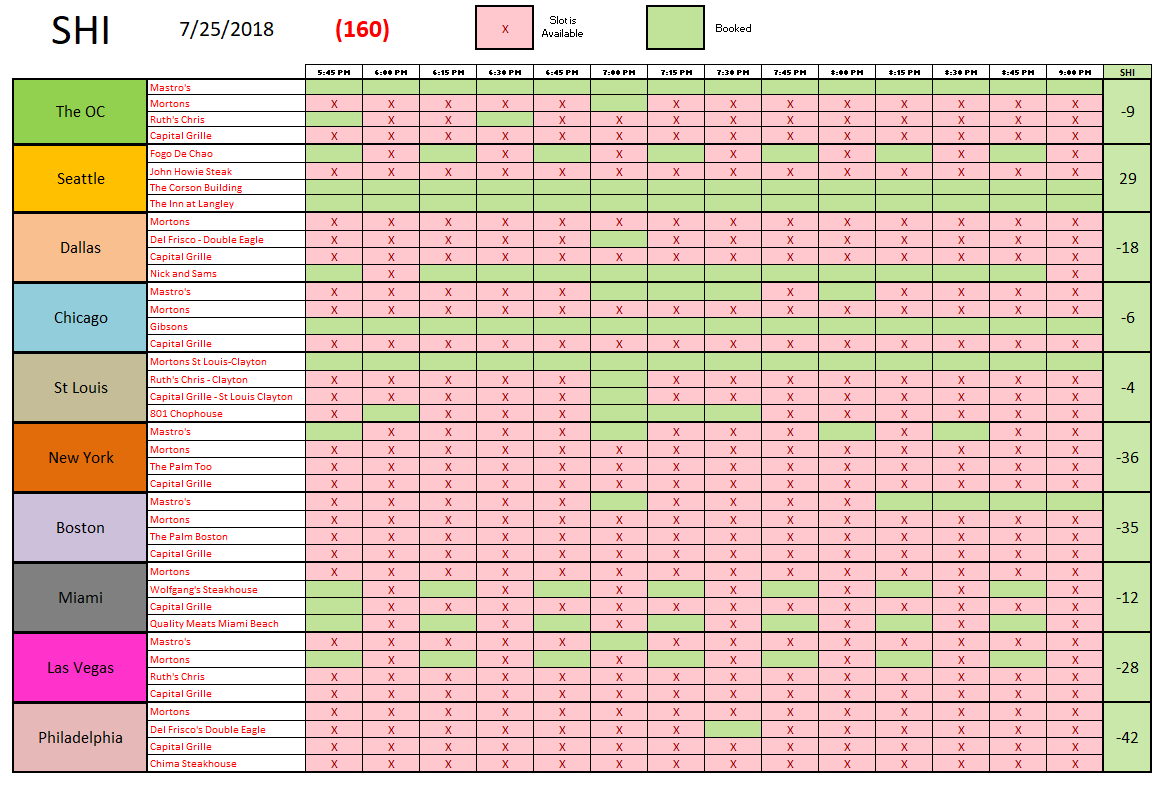

Here is this weeks grid:

The ‘advance’ reading for the Q2, 2018 GDP growth rate is due out in 2 days — on July 27th. You can catch it live on CNBC at 5:30 am CA time. Will the Atlanta FED forecast be closest? Their July 18th forecast is a blistering 4.5% growth rate. Or will the NYC FED be closer? On July 20th, the New York FED staff forecasted a robust 2.69% Q2 growth rate. Or will the SHI10 win the day with a more tepid forecast of 2.2%?

I’ll be watching! How about you?

- Terry Liebman