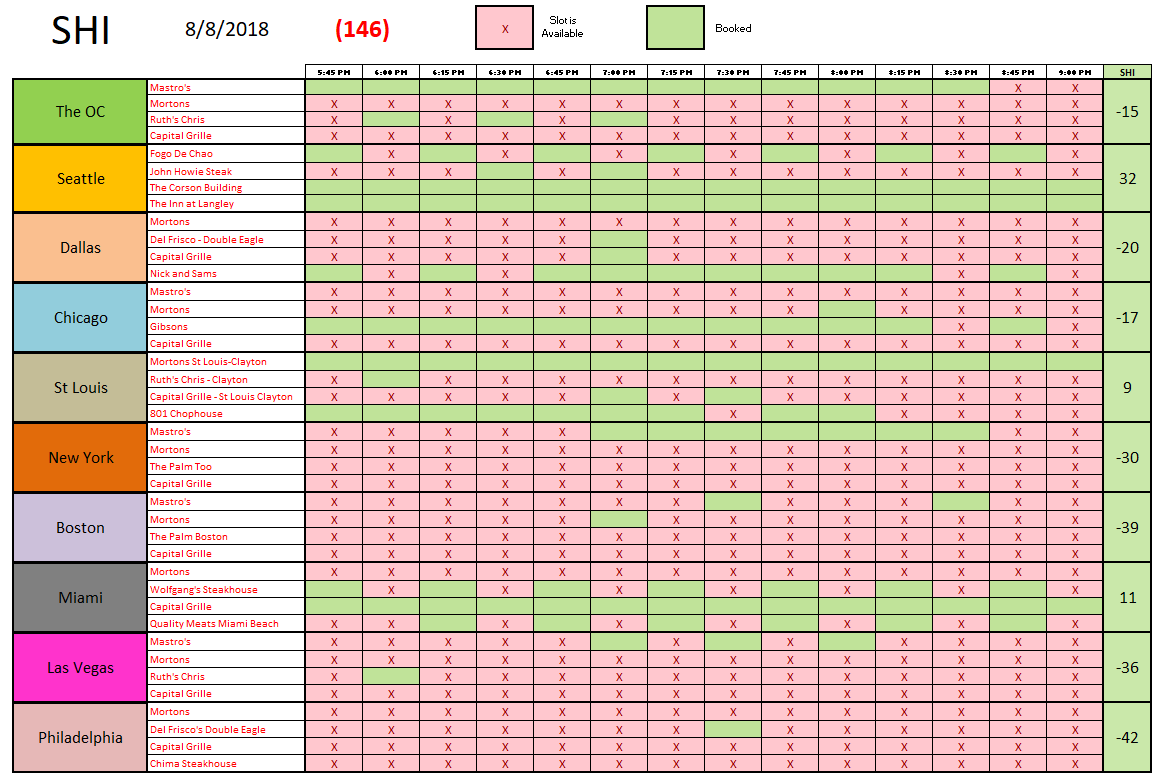

SHI 08.08.18 Affording In the Middle of Nowhere

SHI 08.01.18 Is Our Expansion DOA?

August 1, 2018

SHI 08.15.18 This Turkey is No Filet Mignon

August 15, 2018

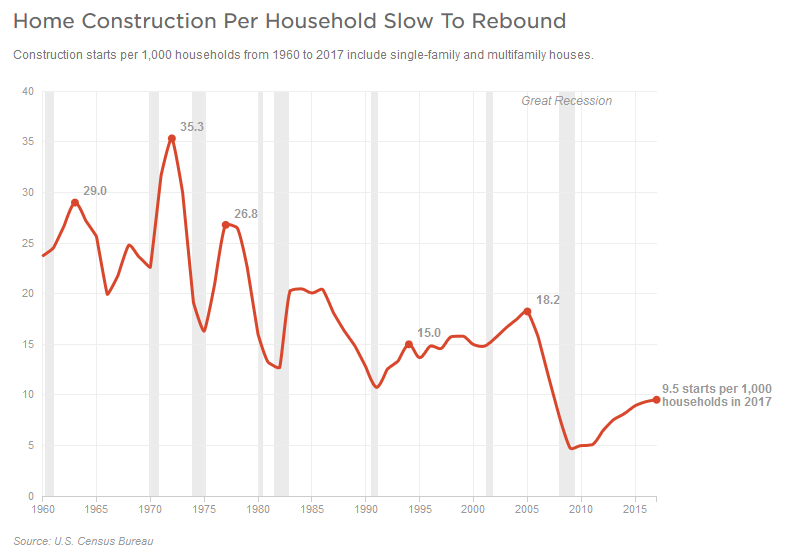

“Like 15 years ago, the American dream of home-ownership is at risk.”

But unlike 15 years ago, the challenge rests more on the supply side. New American households form every year. Kids grow up and (eventually) move out of mom and dad’s basement. A new household is born.

But new home construction is not keeping pace.

50 years ago, the US was growing at a much faster rate. More new homes were needed … and — as we see above — they were built. But not today. Things have improved from 2010, but new single-and multi-family home construction is clearly not keeping pace with the number of new households.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will continue to be true for years to come.

Is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is about $80 trillion today. US ‘current dollar’ GDP now exceeds $20.4 trillion. In Q2 of 2018, We remain about 25% of global GDP. Other than China — a distant second at around $11 trillion — the GDP of no other country is close.

The objective of the SHI10 and this blog is simple: To predict US GDP movement ahead of official economic releases — an important objective since BEA (the ‘Bureau of Economic Analysis’) gross domestic product data is outdated the day it’s released. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

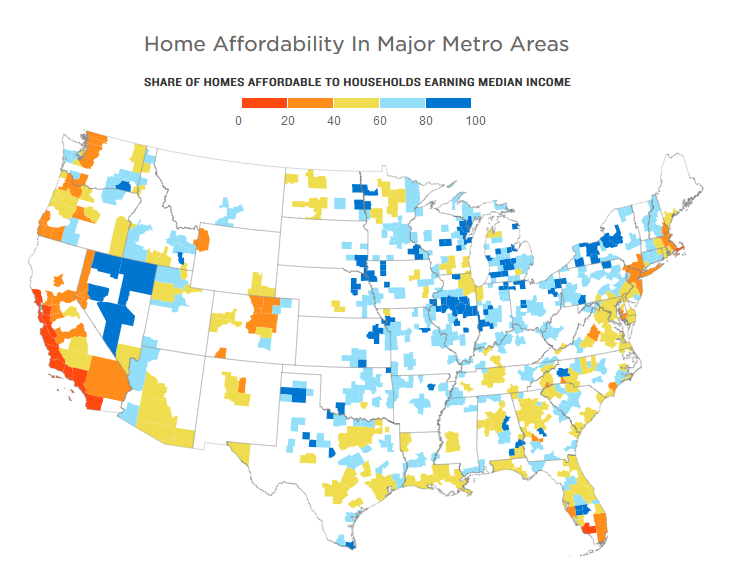

Ironically, there are plenty of homes available, and at very affordable prices, in the “heartland” of America. Also known as the middle of nowhere. Rest assured, I do not make this comment in a derogatory way, only as a reflection of current popular opinion and demand.

The map doesn’t look promising for a new household in California. Even worse, these numbers are from 2016 when both prices and interest rates were lower. Ouch.

Nevada is America’s most affordable state. Except in the western part of the state, along Rockies, where wealthy Californians’ purchase homes, and take residency, to avoid CA state taxes.

But the most affordable area in the US is a large swath of the country of near where the Missouri, Ohio and Mississippi Rivers meet. Take a look at the map: For hundreds of miles in all directions, a household earning the ‘median income’ can afford a home.

Of course, economic growth and new jobs are not plentiful in many of these areas. But if households continue to form at their current rate, and new home construction remains at these low levels — which I expect will be the case — this paradigm may change. Driven by housing needs and quality of life issues, many patches in the Missouri, Ohio, and Mississippi Valleys may begin the attract new industry, new jobs, and new households.

If I wanted to build a single-family home investment portfolio, I would carefully study markets in this area, find the spots where growth is likely, and begin a 20-year strategy.

Steaks, on the other hand, are just as expensive in Peoria as they are in Los Angeles. Let’s see if reservation demand is strong this week.

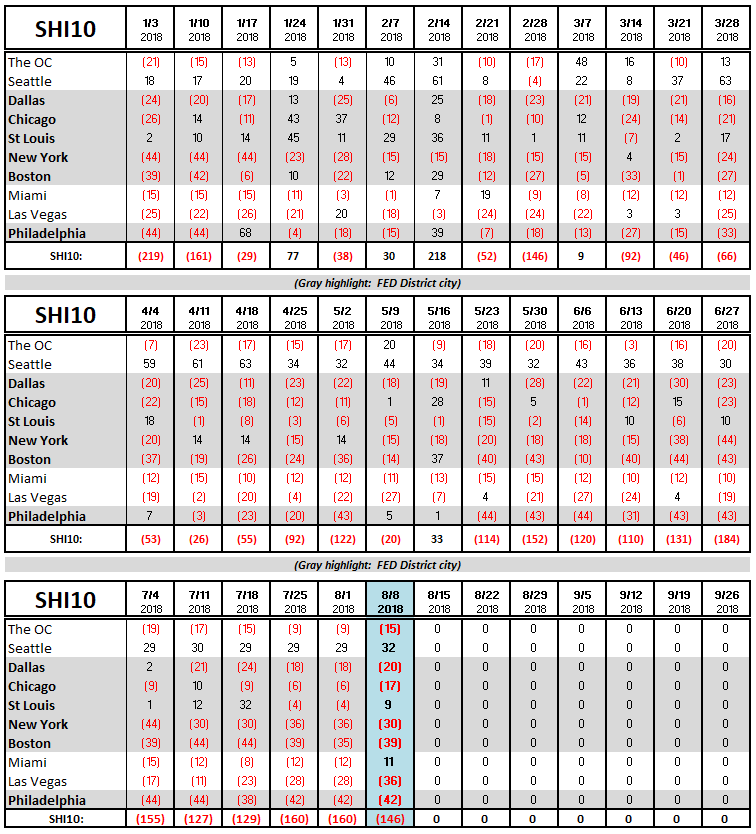

Well, it looks like demand for a seat in our pricey restaurants is about the same as last week. Without exception, all ten markets within our SHI10 saw no significant increase or decrease in reservation demand this week. Here is the 10-city long-term chart:

Here are the current third quarter of 2018 GDP forecasts from the Atlanta and NYC FEDs:

- Atlanta GDPNOW: 8/3/18 — 4.4%

- NY NowCast: 8/3/18 — 2.6%

I find neither forecast to be overly appetizing. Reading the ‘tea leaves’, the SHI10 seems more closely aligned with the NY reading. (Since we are still in the steak houses, I should probably substitute ‘wine labels’ for ‘tea leaves’.) Atlanta was the clear winner for accuracy in Q2, but I don’t think we’ll see a repeat performance in Q3. We’re early in this quarter’s race, but my early Q3 GDP predictions would be in the low 2s. Why? Two reasons.

First, I suspect much of the benefit from the tax cuts and repatriation have now been absorbed into the economy. There is more ‘kinetic’ economic benefit out there, of course, as the US corporate tax rate is now 21%. And billions of dollars remain on the sidelines, in corporate coffers, ready to be invested or returned to shareholders as dividends. But the majority of the benefit from this package has already been realized.

Second, we have serious headwinds coming out of Washington DC in the form of FED rate increases and tariffs. If the FED raises again in September, and the proposed tariffs stick around for a while, both will have the effect of holding down US economic performance.

– Terry Liebman