SHI 08.15.18 This Turkey is No Filet Mignon

SHI 08.08.18 Affording In the Middle of Nowhere

August 8, 2018

SHI 08.22.18 Open a Restaurant

August 22, 2018

“Turkey has yet to Finnish slipping in Greece.”

Sorry. I couldn’t help myself.

It’s a shame more countries aren’t named after food. Imagine the fun we could have if all the post-USSR countries sported names like ‘Brisket‘ or ‘Calamari‘ or ‘Jello.’

But, alas, we have only one: Turkey. Well, I guess ‘Chile’ qualifies, too, right? So we have 2!

Turkeys are reputed to be the dumbest animal on the planet. That’s unlikely to be true, as sponges, starfish and jellyfish don’t even have brains. They must be the dumbest. But if the news out of Turkey has any truth to it, Turkey’s President, Recep Tayyip Erdogan, must be one of the dumbest leaders on the planet. Economically speaking, of course. And he supposedly has a brain.

It might be tough to pick a ‘stupid’ winner, however, since the Venezuela President Nicolas Maduro has been vying for that prize for some time now. Maduro has destroyed his country. I think we should change Venezuela’s name to ‘Jellyfish.’ But I digress. Today we’re talking about that other bonehead leader, Erdogan, and his epic stupid economic moves. Erdogan qualifies as the biggest turkey of them all.

Here’s the bottom line:

- Turkey had the chance to join the EU and the euro. They’ve now blown it. It will probably never happen.

- According to 2017 IMF rankings, Turkey had an annual GDP of about $850 billion and ranked 17th in the world. The sum of the GDPs of the 16 countries above Turkey in this ranking totaled $78.6 trillion. Turkey’s GDP is about 1% of this number. Barely a rounding error.

- But to investors in Turkish debt or equities, it does matter. There is a lesson here: Invest in ’emerging markets’ at your own risk. Turkish investments will not turn out well … as I discuss below.

- Like the bird itself, Turkey doesn’t matter. Except around Thanksgiving. Any impact on global financial markets will be short lived and irrelevant.

- Don’t get me wrong: I like turkey. But, hey, THIS is the Steak House Index. I have to stay focused. 🙂

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will continue to be true for years to come.

Is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is about $80 trillion today. US ‘current dollar’ GDP now exceeds $20.4 trillion. In Q2 of 2018, We remain about 25% of global GDP. Other than China — a distant second at around $11 trillion — the GDP of no other country is close.

The objective of the SHI10 and this blog is simple: To predict US GDP movement ahead of official economic releases — an important objective since BEA (the ‘Bureau of Economic Analysis’) gross domestic product data is outdated the day it’s released. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

Some time ago, I wrote a blog entitled “How to Ruin a Country in 15 Years.” I’m guessing the President of Turkey read my post. Because Erdogan seems to be following Maduro’s economic script in his own country. Here’s a link to my Venezuela post: https://wp.me/p8f7f1-Kb

Erdogan became prime minister of Turkey in 2003. At that time, economic conditions in Turkey were improving. Turkey was working hard to build a sustainable economy, predictable GDP growth, and limit deficit borrowing.

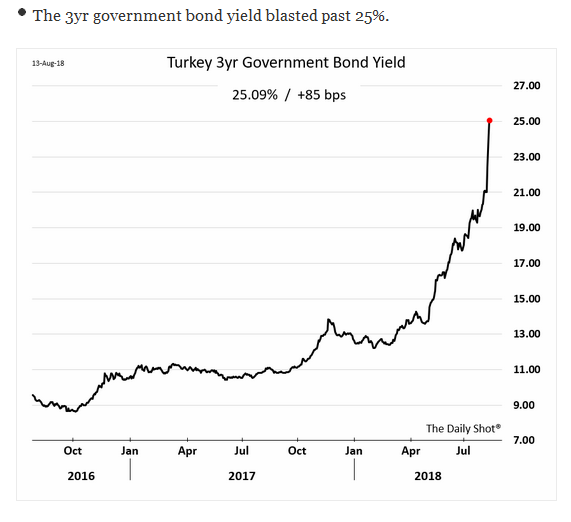

It wasn’t that many years before when their 1-year treasury bill yielded over 100% per year. Soon after the IMF gave Turkey a “thumbs up” on their economic reforms, the yield quickly dropped to 40% per year. Things continued to improve as the years passed. The European Union considered adding Turkey as a member of their currency — if Turkey could control their inflation and deficit spending. Turkey’s 10-year debt fell to below 6% per annum.

No longer. Today, Turkey’s debt is rated as ‘junk.’ Primarily because Erdogan has a faulty foundational economic belief: He contends high interest rates are the cause of inflation, not the result of inflation. He is wrong. Very wrong. And his hubris will make life very, very difficult for all Turks in years to come.

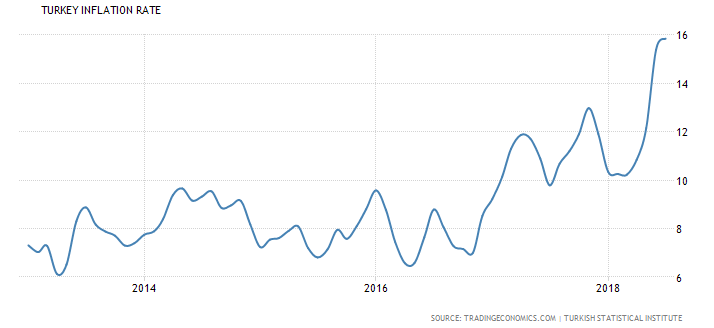

Once again, Turkey’s inflation rate is soaring. If history is any guide, this is only the beginning. Global financial leaders and lenders now seem to agree. The markets are telling us they have decided Turkey will do nothing to stem the problem. They seem to have lost faith in Erdogan and Turkey’s economic policies.

Confidence in a country’s financial leadership shows up in financial markets. Traders vote with their dollars. Or euros. Or lira. On July 24th Turkey’s central bank announced they would keep their “headline” rate unchanged. With the headline rate already at 17.75%, the central bank decision told the markets Erdogan would not use short term rates to battle inflation. Even as their June CPI eclipsed 15.4% — triple Turkey’s “official target inflation rate.”

The US experienced a similar challenge in the 1970s. At that time, US GDP exceeded 40% of global GDP. By the end of that decade the FED chairman decided enough was enough and over the next few years increased FED rates dramatically. For almost a decade, US interest rates remained elevated far above long-term trend lines. But the medicine worked: Inflation was tamed and, over time, interest rates came back to earth.

So far, Erdogan doesn’t seem to agree with the FEDs playbook. Again, Erdogan has gone on record contending high interest rates are the cause of inflation, not the result of inflation. He is very wrong.

To be fair, Turkey did recently increase their headline rate up to 17.75%. Until May, the official rate was only 8%. It’s been at or below 8% since 2010. It’s important to remember that Turkish interest rates have been high for decades: Their headline rate has averaged 59.02% from 1990 thru 2018!

The all time high? 500% in March of 1994. Yes. That’s 500% per year. Invest $100 in a CD … and one year later your CD is worth $600! Why were rates so high? That same year, inflation was running above 130%.

All of which might make you wonder why anyone is surprised by this latest turn of events. Perhaps the turkeys here are the lenders who offered low-interest rate loans to Turkey’s government, banks, and businesses in the first place. But Turkey worked hard to get its financial house in order and has been lobbying hard since 2000 to join the euro. Until recently, the global financial community gave them the benefit of the doubt.

But no longer. It looks like investors have finally lost confidence in Turkish debt. Things have been bad for a while … they just got worse. The market value of Turkey’s debt has plummeted and investors holding Turkish debt are getting killed:

For example, this is from a Bloomberg report:

“Dollar-denominated June 2028 bonds of ‘Turkiye Is Bankasi AS’ lost 27 percent, while ‘Akbank TAS’s March 2027’ securities declined 23 percent. High yields in the secondary market may mean that issuers will wait for asset prices to stabilize before testing the waters, even though they have $17 billion foreign-exchange debt coming due by the end of next year, according to data compiled by Bloomberg.”

When losses like this occur, investor run for the hills. Turkey won’t be issuing any new dollar-denominated debt for a while. No sane investor will buy it. Which will make financing their $13 billion annual budget deficit plus $17 billion of (foreign exchange) debt much more difficult — if not downright impossible. It’s possible someone might buy Turkish debt if the offered interest rate is high enough … but it would have to be exceptionally high. And the debt would have to be dollar-denominated. No investor will take the currency exchange risk.

Which is problem number two. And this is probably the bigger problem. Because that $13 billion annual deficit is about to get a LOT bigger.

Turkey’s bigger problem is the currency relationship between the Turkish lira and the US dollar. Their currency has lost a ton of value. It is plummeting toward earth at an accelerating rate of speed. According to Turkey’s Central Bank, the ‘official’ USD/Turkish lira exchange rate in 2016 was about 3. Today it’s about 6. Double. Said another way, anything you want to buy in the world that’s priced in dollars costs twice as much in Turkish lira in 2018 as it did at the end of 2016. Ouch.

Turkey has borrowed about $300 billion in foreign currency. Currencies such as US dollars and euros. Turkey borrowed in dollars or euros, but must use their local currency, the lira, to repay the debt when due. And that repayment will now cost 2X.

Here are a couple of charts from the Bank for International Settlements (BIS) showing the foolish acceleration in Turkey’ foreign borrowings denominated in US dollars:

All told, companies and the government of Turkey owe about $100 billion of debt denominated in US dollars. Repaying that debt, when due, at today’s exchange rate will cost about $200 billion in lira. Double ouch.

Financially speaking, this will end badly for Turkey. Very badly. Geo-politically, too, conditions in that part of the world just got a whole lot worse. But for the financial markets, this is a blip on the screen only.

I say we drink copious amounts of wine, eat thick, juicy, expensive steaks, and move from turkeys to cows! You with me? How are the steakhouses doing this week? Let’s take a look.

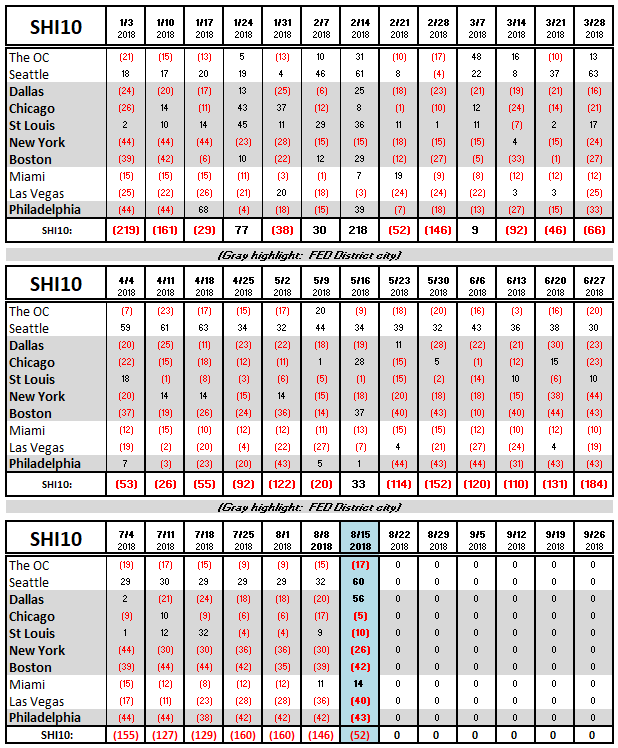

The grill is hot and so is Steak House restaurant reservation demand! This week we see a sizable surge in demand. The cows in Seattle and Dallas better post more ‘eat mor chikin‘ billboards, because pricey steak restaurants in these 2 cities are almost fully booked this coming Saturday.

As you’ll see in the longer term trend report below, reservation demand in Dallas skyrocketed this week when compared to the prior 5 SHI reports. In fact, we have to travel back in time by 6 weeks to find a positive SHI reading in Dallas.

Last week, the Dallas SHI was a negative 20. This week, a positive 56. That’s a 76 point swing. In one week. Impressive. It makes me wonder what might be driving this demand surge. It’s almost like everyone in Dallas woke up this morning and decided Saturday night would be a perfect time to spend $600 on a NY Steak dinner! Let’s book a table for 4!

Here’s the long-term trend report:

Of the 10-cities in our SHI10, reservation conditions improved meaningfully in Seattle, Dallas, and Chicago. In all other cities, except St Louis, reservation demand remained about the same. All in all, a good week for the SHI and a bad week for the cow community.

Earlier today, the Atlanta FED released their latest GDPNow forecast for Q3: 4.3%. The latest NY FED ‘nowcast,’ from 8/10, is a more pedestrian 2.57%. This week’s SHI10 also seems to be indicating robust economic conditions continue across the US.

It’s been said you can’t soar like an eagle when you surround yourself with turkeys. This week’s SHI10 takes exception with this expression — our economy seams to be soaring with the eagles. In spite of the turkeys in Turkey.

- Terry Liebman

{kind=link}