SHI 1/17/18: Where is Inflation?

SHI 1/10/18 The SHI10 and FED Districts

January 10, 2018

SHI 1.24.18: The Rate of Return on Everything

January 24, 2018

Where is inflation?

Central bankers continue to be puzzled by inflation. Or, more precisely, by the lack thereof.

With a global economy fully aligned and growing in sync for the first time in many years, inflation remains the missing puzzle piece. Where is the higher inflation central bankers and investors are expecting?

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will continue to be true for years to come.

Is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is almost $80 trillion today.

At last count, US ‘current dollar’ GDP is about $19.5 trillion — about 25% of the global total. Other than China — a distant second at around $11 trillion — no other country is close.

The objective of the SHI10 and this blog is simple: To predict US GDP movement ahead of official economic releases — an important objective since BEA (the ‘Bureau of Economic Analysis’) gross domestic product data is outdated the day it’s released.

Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of the total. In fact, the majority of all US GDP increases (or declines) usually result from (increases or decreases in) consumer spending. This is clearly an important metric. The Steak House Index focuses right here … on the “consumer spending” metric.

I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been. Thereby giving us the ability to take action early.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI, but we’ll explore related items of economic importance.

If the SHI index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

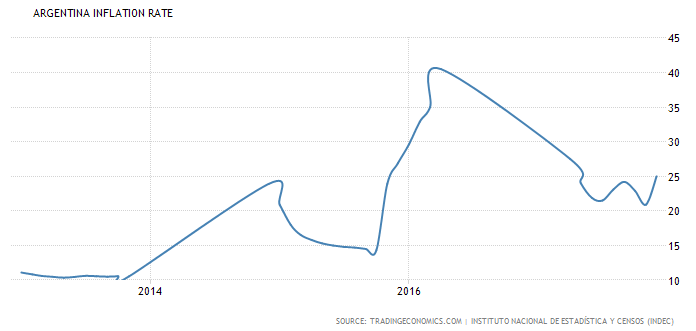

Where is Inflation? South America is the short answer.

Brazil, the largest economy on that continent, with an annual GDP around $3 trillion, has moderated from an inflation rate of over 10% in 2016 to just under 3% today. Economy number 2 — Argentina — has a horrible inflation track record with CPI increases currently running over 25% per year. A 5-year graph of their CPI rate history resembles the path of an aimlessly wandering centipede:

North of the equator, however, the developed world continues to show scant signs of inflation. In the EU, China, and Japan — the 2nd, 3rd, 4th largest economies, in order — inflation remains muted. The most recent annual inflation figures, respectively, are 1.4%, 1.8%, and 0.6%.

To be clear, the UK economy — #5 on the list — is now inflating at over 3% per year, thanks to their bonehead ‘Brexit’ choice. 🙂

And here in the US, the inflation rate does seem to be creeping up, slightly. But not as much as bond investors fear. Traders are now anticipating a sizable increase.

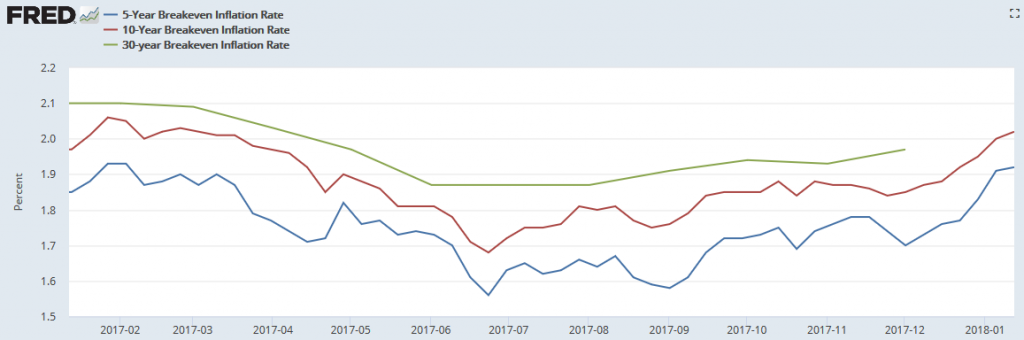

You may have heard the phrase “Breakeven Inflation Rate” (BIR). In simple terms, the BIR is a measure of expected inflation derived and calculated from two (2) ever-fluctuating Treasury bond rates, including an ‘inflation-indexed’ security. Bond investors — for very good reason — constantly worry about inflation. They should: An increasing inflation rate destroys long-term returns for bond holders.

All BIR maturities (5, 10, and 30 years) reflect significantly higher inflation expectations since mid-2017:

And recently, the 10-year treasury has climbed to its highest level since March. From a low in September of 2.07, the 10-year is now over 2.5%.

Why? Simple: They share concern that the US and global economies are strong, getting stronger every month, and may — oh no! — grow too fast! Like the porridge in the fairy tale, “Goldilocks and the Three Bears,” bond investors always hope for a “just right” scenario, but fear an economy that might be “too hot.”

Today’s low unemployment rate and the newly-enacted tax act are fueling some of these concerns. As is the recent weakness in the dollar against the currencies of our trading partners.

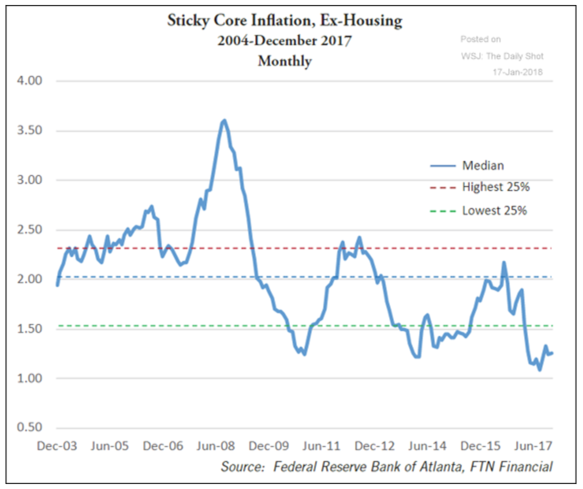

The most recent CPI press release which showed “shelter” costs increasing 0.4% in December and 3.2% for 2017 over all. But here’s the problem with statistics. The devil is always in the details. And it’s worth noting that according the the Bureau of Economic Analysis (BEA), the CPI and PCE calculations “weigh” housing costs very differently. For the CPI calculation, housing accounts for 42.2% of the calculation. In the PCE, only 23.6%. Which means that while housing costs are clearly increasing across the US, the inflation-measure used by the FED — the PCE — will reflect a significantly lower inflation number.

Extracting housing inflation from the CPI equation, we see that non-housing inflation is at it’s lowest level in decades. Take a look at a very recent “sticky CPI” calculation from the Atlanta FED (“sticky” measures slow-to-change CPI components):

The biggest concern, of course, remains potential wage inflation. Yet, once again, it remains in hibernation. Last Friday, the Bureau of Labor Statistics (BLS) released their most recent “Employment Situation Summary.” In that report, they said:

“In December, average hourly earnings for all employees…by 9 cents to $26.63. Over the year, average hourly earnings have risen by 65 cents, or 2.5%.”

Clearly, wage inflation growth, in spite of the continuing low unemployment rate, remains quite muted.

So what’s the worry? Simply that this situation will not remain as it is. That over time, current conditions will re-ignite inflation. Is this a valid concern?

Yes. To some extent. Taking the issue to the extreme — a zero percent unemployment rate — and we’re likely to experience wage inflation. But in today’s economy, the role of US ‘human’ labor in the inflation equation remains complex and somewhat inexplicable: If US businesses continue to “substitute” non-US labor and automation as an alternative to hiring humans, the outcome is anything but certain. I continue to believe we will not experience robust wage inflation. Mine is a contrarian view … but I’ll stick with it.

For now, I firmly believe, inflation will remain in the southern hemisphere. I don’t think it will head north any time soon. Let’s now take a look at the SHI10.

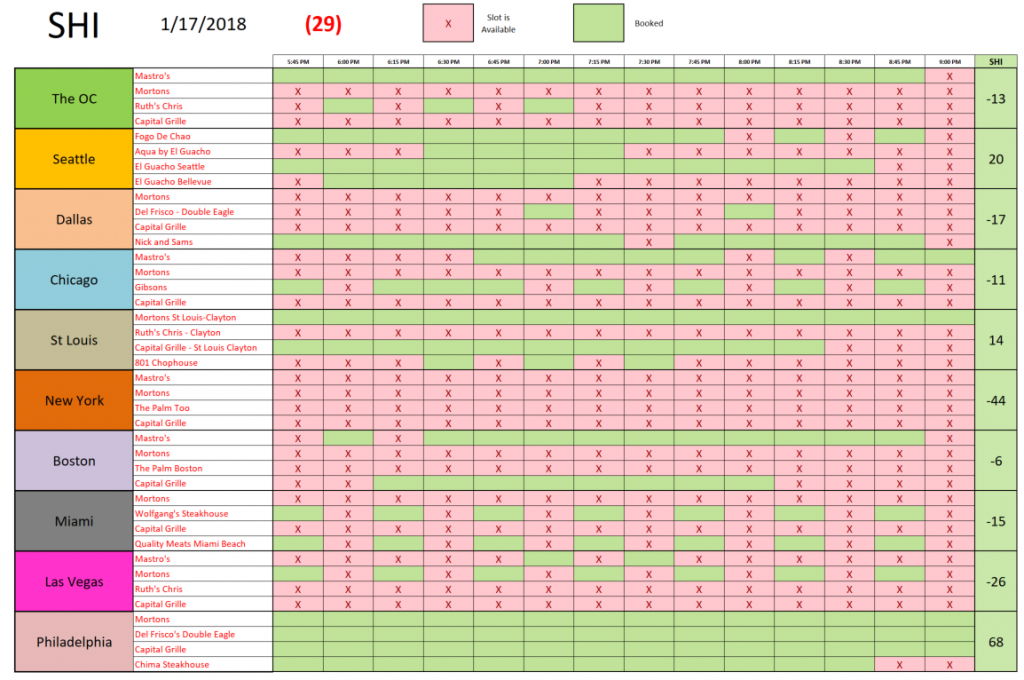

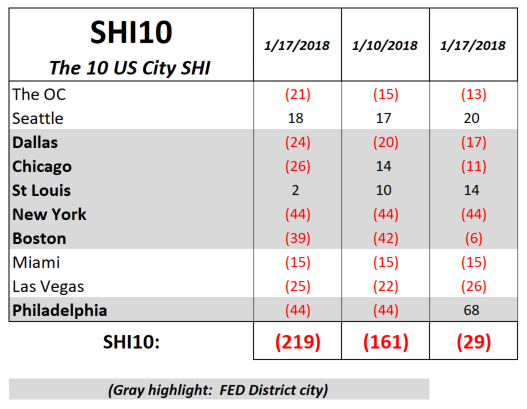

Well, this is an interesting week. Take a look at the chart below — and, more specifically, Philadelphia:

Last week, Philadelphia was wide open. This week, of 56 reservation time slots on Saturday, the 20th of January, only 2 tables remain open. Apparently, everyone is tired of cold weather and staying home! A smokin’-hot, fresh off the grill, T-Bone is just what the doctor ordered! Frankly, I’m skeptical this data is accurate … but after two OpenTable searches, this is the outcome. So we’ll go with it.

New York, on the other hand, continues to be a surprise. For some reason — again, perhaps the weather — every time slot in every restaurant we’re tracking is available. Odd. Sure, NYC has a bunch of great steakhouses, but the trend so far this year seems unusual to me.

Regardless, this week the SHI10 is a negative (-29) — a significant improvement over last week. Here’s our trending report:

It’s worth noting that the most recent FED ‘Beige Book’ report was released moments ago. Their summary, entitled ‘Overall Economic Activity’ said:

“Reports from the 12 Federal Reserve Districts indicated that the economy continued to expand from late November through the end of the year, with 11 Districts reporting modest to moderate gains and Dallas recording a robust increase. The outlook for 2018 remains optimistic for a majority of contacts across the country. Most Districts reported that non-auto retail sales expanded since the last report and that auto sales were mixed. Some retailers highlighted that holiday sales were higher than expected. Residential real estate activity remained constrained across the country. Most Districts reported little growth in home sales due to limited housing inventory. Nonresidential activity continued to experience slight growth. Most manufacturers reported modest growth in overall business conditions. Reports indicated that some manufacturers increased capital expenditures over the reporting period. Most reporting Districts noted continued growth in transportation activity. Loan volumes in many Districts were steady. Among reporting Districts, agricultural conditions were mixed and energy contacts described a slight uptick in activity.”

On the topic of inflation, they had this to say:

“Most Districts reported modest to moderate price growth since the last report; exceptions were Chicago, which noted that prices increased only slightly while San Francisco noted price inflation was down slightly. Reports of pricing pressures were mixed across the country although several Districts noted increases in manufacturing, construction, or transportation input costs. Firms in some Districts noted an ability to increase selling prices. Retailers in some Districts reported modest price increases and there were reports of rising home prices across most of the country. Agriculture and energy commodity prices were mixed.”

My take-away from the Beige Book report:

- Economic results in 10 of the districts are improving and Dallas is on a tear.

- Optimism is high for more of the same as 2018 unfolds.

- Inflation remains muted.

I agree. There are no economic storm clouds on the horizon here in the US. One that gives me brief pause outside the US is the Chinese housing market … but for now, I’ll leave my comment here. It’s something to watch.

Until next week, take care.

– Terry Liebman