SHI 1.18.23 – Is Our Economy Slowing?

SHI 1.11.23 — Economics Used to be Easy

January 11, 2023

SHI 1.24.23 — Meat Beyond Impossible!

January 25, 2023

Yes. I believe it is.

But “slowing” is not the same thing as stopping. Or falling … as in a recession. These are very different things.

Think of it this way: Say you’re traveling at 70 MPH on the freeway. You see red brake lights and cars up ahead … so you take your foot off the accelerator — maybe even tap the brakes — and your car begins to slow … 65 … 60 … 50 … 45 … all the way down to 30 MPH. You’re still moving forward, but at a reduced rate of speed. This is analogous to the “economic highway” we find ourselves on. We’re slowing down.

“

The Slowing US Economy is No Surprise.”

“

The Slowing US Economy is No Surprise.”

On our economic highway, of course, there are no cars. No, our slowdown is caused by rhetoric and rates, increases in both courtesy of the FED and other “experts.” A day doesn’t pass without at least one FED Governor jaw-boning about future interest rate hikes … or some economic or financial expert assuring us a 2023 recession is right around the corner. Of course, today’s economic release from the US Department of Commerce added fuel to the fire. Because “Retail Sales” — we just learned — fell in December of 2022! What? Christmas time? Santa, say it ain’t true! Did retail sales actually decline from November? Yep. They did.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. At the end of Q3, 2022, in ‘current-dollar’ terms, US annual economic output rose to $25.74 trillion. Thru Q3, America’s current-dollar GDP has increased at an annualized rate exceeding 7%. The world’s annual GDP rose to over $100 trillion during 2022. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the 3 big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

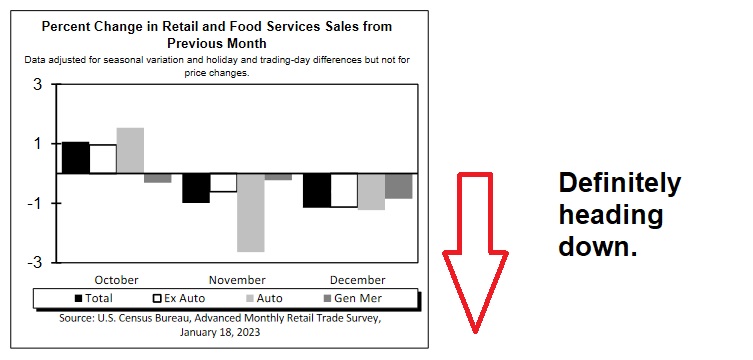

Retail sales, officially known as “ADVANCE MONTHLY SALES FOR RETAIL AND FOOD SERVICES, DECEMBER 2022” declined by 1.1% from November, a month earlier.

The message above is clear. The sale of “stuff” has slowed. Month over month. Year over year, however, they are up about 6%. So while it’s too early to report ‘consumer consumption’ is dead and gone, there are indications of slowing.

Which is not surprising, frankly, given the clear and obvious attempts by the FED to scare the consumer into spending less. And the never-ending “recession-recession-recession” talk in the media certainly has had an effect. From new apartment leases to shiny-new Mercedes, the consumer is making more cautious decisions. And sales are slowing as a result. But they are not down — year over year.

In fact, when comparing 2022 spending levels to those of 2021, total “Retail & Food Services” were up 9.2%. Pretty good. Of course, 2022 ‘Gas Station‘ sales were up almost 30% over the prior year; only ‘Electronic & Appliance‘ store sales were actually down — by 6.3%.

The FED’s ‘Beige Book‘ — a review of business conditions in the 12 Federal Reserve districts — was also released earlier today. Overall, the FED reported that “economic activity was relatively unchanged since the previous report” from about 45 days ago. Interesting. I wonder if they are disappointed? 🙂

The Beige Book shared that ‘employment grew at a modest pace‘ and so did selling prices of goods and services — although the pace of increases appears to be slowing. The words “contracted” and “slowed” were used to describe activity in New York, Philly, Cleveland, Chicago, and Kansas City. In the other FED cities, the Beige Book reported that “economic activity expanded modestly.”

Our economy is slowing. Which, again, is not surprising given the rhetoric and a FED funds rate in the high 4% range. The rate hikes have certainly had an impact — uneven, of course, but an impact nonetheless.

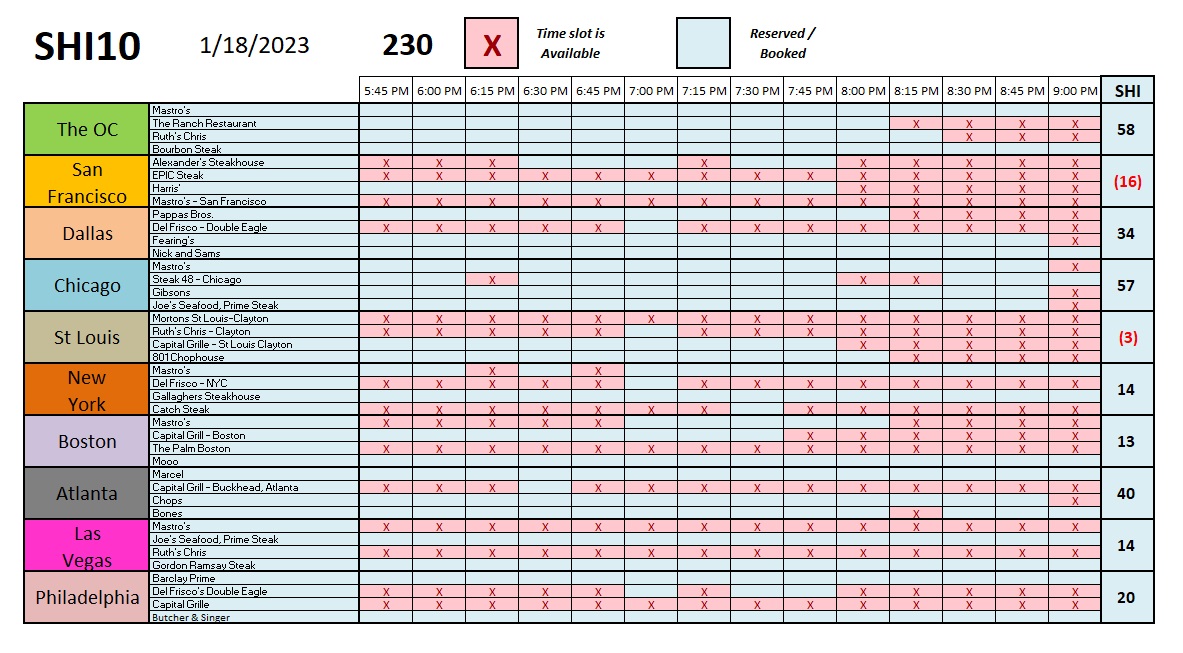

Ironically, reservation demand at our expensive steak houses seems to be undeterred.

So far this year, demand is rather consistent. Thru the lens of the SHI, our economy seems quite steady.

Consider these facts, as we think about a “slowing” consumer spending segment. When pulling today’s SHI numbers, I noticed OpenTable reported that ‘Ruth’s Chris Steak House – Irvine‘ has been “booked” 101 times today; ‘The Ranch‘ 82 times today; and, ‘Mastro’s Ocean Club – Newport Beach‘ a surprising 161 times! And ‘Gallaghers Steakhouse – Manhattan‘? A downright stunning 342 times today!

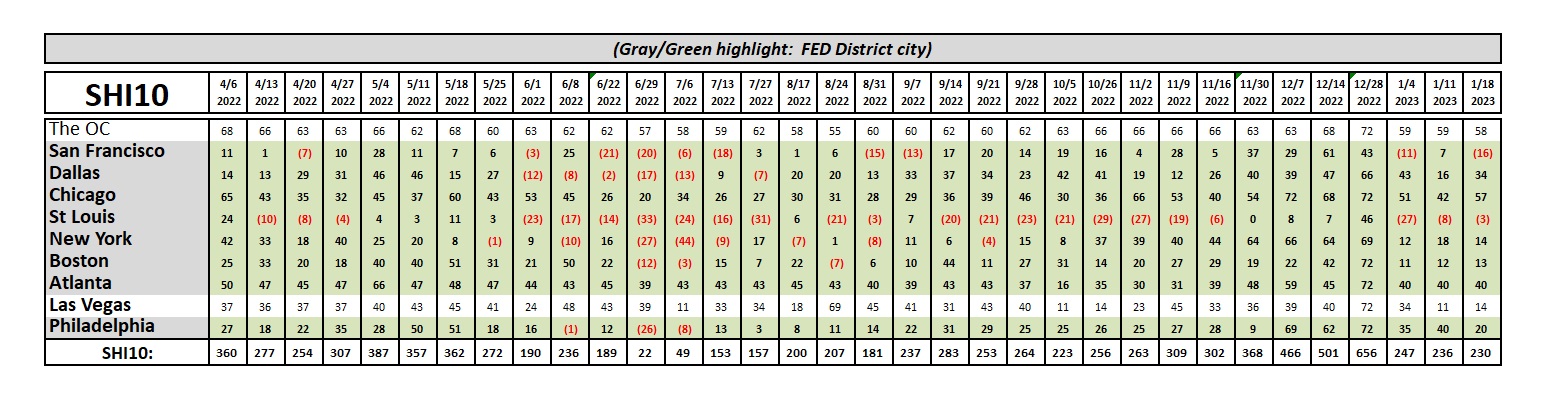

Remember: I pull this data at 11 am. It’s not even lunch time! To me, 161 and 342 bookings before 11 am is an amazing statistic for an expensive eatery where each and every diner will spend a minimum of $150. This doesn’t feel like a slowing economy to me. Here’s the longer term trend report:

This is definitely an economically turbulent time. With so much FED activity and economic expert jaw-boning, the frightened consumer is definitely a little confused. So they are buying less expensive stuff. On the other they seem to love the steakhouses! So how bad can it be, right?

I still doubt we’ll see a recessions in 2023. While the official definition is “2 consecutive quarters of negative real GDP growth”, the National Bureau of Economic Research takes a less rigid stance, considering a recession a “significant reduction” in economic activity, across the whole economy, that lasts “more than a few months.”

By that subjective metric, might we enter a recession this year? Hard to say … but that’s an easier bucket to fill.

<:> Terry Liebman