SHI 1.26.22 – “… What a Stupid Son of a Bitch.”

SHI 1.12.22 – Is Greed Good?

January 12, 2022

SHI 2.2.22 – This Doesn’t Happen Every Day

February 2, 2022

Well. THAT was interesting.

Above, I’m quoting President Biden from a press conference earlier this week. You may have seen the clip.

Apparently, President Biden is not a fan of stupid questions: “Do you think inflation will be a political liability?,” a reporter yelled out. Gee, really? Duh. In this case, folks, I’m gonna have to agree with the President. What a stupid son of a bitch. 🙂

“

Yes, inflation is always a political liability.“

“Yes, inflation is always a political liability.“

Interestingly enough, core inflation really is not a political outcome. Note I said “core.” Meaning I’m primarily stripping out energy price variations. Because energy prices can be directly impacted by politics. And often are. In my opinion. And thru the lens of “oil price stability,” the current administration has made some strategic errors. Again, in my opinion.

Most other major components of the CPI, I believe, are far less impacted by politicians and political choices. Sure, politicians can legislatively impact things like food prices, apartment rents, and many other CPI items; but, more often, price movements are the result of supply and demand relationships. And as we all know, those relationships are definitely impacted by things like pandemics, supply chain disruptions, etc. 🙂

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. Significantly. In fact, in the 6 months of Q2 and Q3, growth nominal terms exceed $1.1 trillion of economic activity. The world’s annual GDP is expect to end 2021 near about $93 trillion. Annualized, America’s GDP settling in at $23.17 trillion — still around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are your big players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

I don’t think I’ve ever talked about the same US president in two (2) consecutive blog posts. But I couldn’t resist. Like a perfectly grilled filet mignon, Biden’s comment is both rare and juicy. 🙂

When was the last time we heard a sitting president use such, well, “colorful” language? Right, from President Trump. But before Trump? Probably never, right? I’m of the opinion we can’t blame Biden for being a bit touchy and peevish on the issue of inflation. And stupid reporters, for that matter. Because, as we all know, throughout history, whenever possible, a President and his administration often take credit for a strong economy, low unemployment rates, and stable prices. And, whether responsible or not, they are blamed for the opposite. Like today’s rather high consumer price inflation.

Frankly, if I were Biden, I’d probably be trumpeting recent wage growth. (No pun intended.) Nominal wage growth hasn’t been higher in years. Americans are taking home far bigger paychecks today than they were pre-pandemic. In fact, according to the St Louis FED, the “average hourly earnings” of all employees grew by over 8% during April of 2020. Which seems odd to me, frankly, given the massive job layoffs around that time triggered by the pandemic response. I suspect this number must include government subsidies. Regardless, during 2021, two months saw earnings growth above 5%. Perhaps Biden can claim credit for this excellent statistic? 🙂

But a challenge facing the current administration is the simple fact that while hourly earnings may be up, prices at the grocery store and gas pump are up even more. Adjusting the ‘noninal’ wage increases for the effects of inflation, take-home pays are actually lower than they were in 2021. Consider this chart from the U.S. Bureau of Labor Statistics:

Yes, during 2021, “real” wages for all American’s actually declined by 2.4%. Ouch.

Permit me a warning here. Depending on the source, this data can be reported quite differently. Not surprisingly, I suspect politics may play into the graphic image the author uses. For example, I did not create the graph above — the U.S. Bureau of Labor Statistics did. No politics here. The source data (left click, open in a new tab):

But I’ve seen a number of similar graphic images — ostensibly from reliable sources — that suggest “real” earnings, which is to say earnings after adjusting for the effects of CPI inflation, have been negative in many of the past 10 or 11 years. According to the DOL (above), this is not true. Yes, “real” wages fell during 2011 and 2012. But inflation-adjusted wages actually grew year-over-year from 2013 until this past year.

Recently, nominal wages have been growing like a weed. Nominal wages are WAY up during the past two years. But real wages were down significantly in 2021. Why? Because in 2020, the “CPI-U” grew by only 1.4%. In contrast, during 2021, the CPI-U grew by 7%. So, doing the math, if the 12-month change in “real” wages during 2021 was a 2.4% decline, that means the nominal wage increase during 2021 was 5.6%. Pretty good, right? Sure, but for many Americans it doesn’t “feel” good because food prices, gas at the pump, and apartment rents have all jumped in the past year. Unfortunately for President Biden, significant CPI inflation is a political liability. Just as it can be for every US President.

You may recall that by law, the FED has very specific and precise duties. From the Federal Reserve’s website:

“The Federal Reserve Act mandates that the Federal Reserve conduct monetary policy “so as to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.” Even though the act lists three distinct goals of monetary policy, the Fed’s mandate for monetary policy is commonly known as the dual mandate. “

Interest rates are more of a tool used by the FED to accomplish their 2 mandates here in America: “maximum” employment and stable prices. Right now, the FED is struggling to navigate between the two. On one hand, by many measures, the employment situation has never been stronger (JOLTS report; the U-3 unemployment rate). Ironically, by others, it has rarely been weaker (labor participation ratio; civilian labor force size). Nominal wages are growing faster than they have in many years; and according to the Conference Board, companies are reporting that 2022 “salary increase budgets” are the highest since 2008 — meaning wages across America are expected to grow significantly in 2022.

Which is both good or bad … depending on your perspective, right? Higher wages (nominal) mean Americans are taking home more money … but higher wages also means that wage inflation is higher. What a conundrum. Which event is the greater political liability for President Biden? I’m not sure anyone can answer that one accurately. 🙂

In the final analysis, the FED must grow the US economy to “foster” both price stability and “maximum” employment. GDP must grow to achieve the FEDs goals. In a shrinking economy, it’s easy for persistent deflation to settle in, and it’s hard to keep people employed. You don’t have to take my word for it: Study the difficulties in Japan during the past 20 or 30 years. In Japan, where their population has been consistently shrinking, they have struggled mightily to stoke any inflation, employment gains, or even miniscule GDP growth. But here in the US, so far anyway, we’ve been able to avoid those draconian outcomes. And right now, the FED has to deal with the opposite challenges. Too much … not too little.

I continue to believe much of our current consumer price inflation is related to supply chain bottlenecks.

These will self-correct over time. How much time, of course, is the unanswerable question. In the meantime, we have a lot of Americans who are very unhappy with prices at the grocery store and the pump — which is, of course, a serious political liability for President Biden.

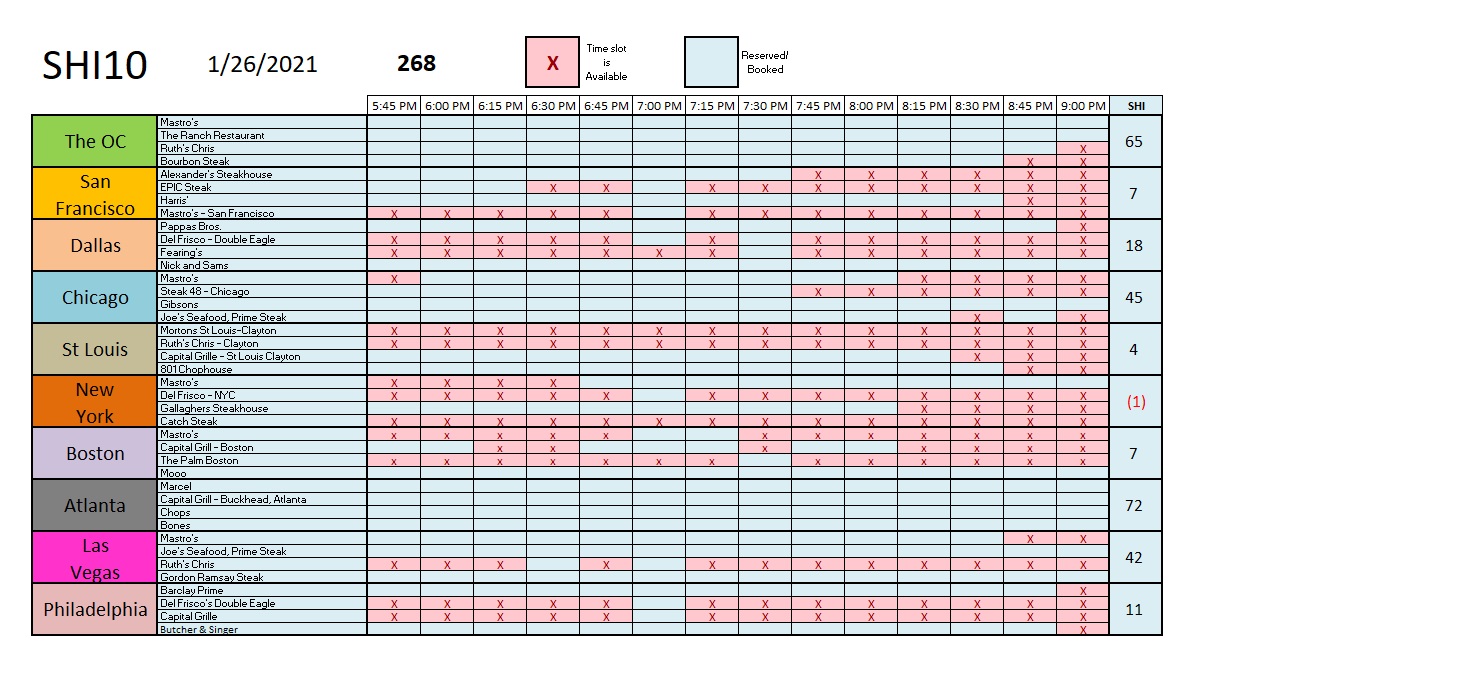

Are affluent Americans getting peevish with the price of a steak at Mastros? After all, according to the Bureau of Labor Statistics, the price of beef was up 20.1% between October of 2020 and October of 2021. Is expensive steakhouse reservation demand declining as a result?

Well, it’s a mixed bag this week. For example, take a look at Atlanta (chart above). Wow! If you don’t already have an expensive eatery reservation at our four (4) Atlanta steakhouses for this coming Saturday, you will not get one between 5:45 and 9:00 pm. These restaurants are fully booked. And here in “The OC,” our pricey grills are almost fully booked. Alternatively, NYC is showing an SHI of (1) — our only negative reading in the chart. San Francisco, St Louis and Boston are also fairly wide open for Saturday. It’s a mixed bag.

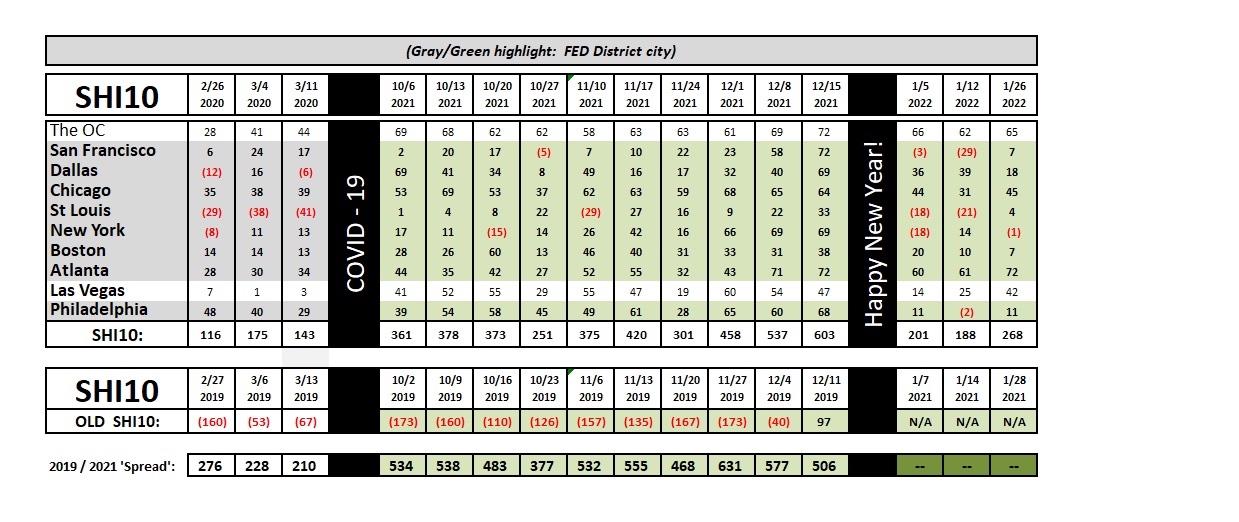

The longer term trend report, however, shows improvement over two weeks ago. (Sorry I missed you last week — I enjoyed a couple of fun ski-days at Mammoth.)

The trend appears positive. The SHI10 is up 80 points from the prior reading. It would appear that beef price inflation is not keeping patrons away this week.

Earlier today, the FED finished their first 2022 meeting. Chair Powell’s comments at the subsequent press conference seemed to worry the financial markets — stocks moved down and long-term interest rates moved up. Powell’s comments like, “The balance sheet is substantially larger than it needs to be,” seemed to spook investors. Ironically, I suspect every financial expert would probably agree with Powell’s statement; so, the nuance, it would appear, seems to be in the delicate balancing act of shrinking balance sheet, increasing rates, and lower inflation, all the while working hard to avoid pushing the US economy into a recession.

Milton Friedman, a luminary monetary economist from about 50 years ago, famously said, “Inflation is always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output.” Given current economic conditions, I suspect Friedman, if asked, would vehemently disagree with the ideas in “Modern Monetary Theory” which suggest that a rapidly expanding monetary base has absolutely no impact on inflation. If nothing else, 2020 and 2021 have proven MMT to be a complete farce. 🙂

The BEA will release its “Gross Domestic Product, 4th Quarter and Year 2021” tomorrow morning. 5:30 am CA time. Get up early and watch the news! It promises to be exciting!

<:> Terry Liebman