SHI 1.5.22 – Have Your Steak and Eat it Too!

SHI 12.15.21 – Land of the Free. Home of the Brave.

December 15, 2021

SHI 1.12.22 – Is Greed Good?

January 12, 2022

Happy New Year … and welcome back!

Welcome to the Steak House Index, where not surprisingly, steak plays a big role. Well, perhaps not steak so much as reservation demand at the most expensive of steak house restaurants in America.

“

Steak? Cake? What are we talking about here …. “

“Steak? Cake? What are we talking about here …. “

Yes, that photo is just gross. But when I found an article in a recent Economist issue, titled “The World Ahead in 2022,” which somewhat put steak in the spotlight, in a manner of speaking, I had to share.

The article itself was fascinating, discussing all types of budding technologies the authors expect we may see or experience beginning in 2022: Things like ‘solar geoengineering‘ to counter rising global temperatures; ‘container ships with sails‘ to reduce energy demand; ‘3D-printed bone implants‘ that should be available for human implantation in 2022; ‘flying electric cars‘ could soon be a reality, with one company planning to offer ‘air-taxi’ service at the 2024 Paris Olympics; of course, artificial reality of ‘the metaverse‘ is closer to becoming a reality; and, finally, ‘artificial steak‘!

That’s right: Artificial steak! Well, in a manner of speaking. It is real steak, but artificially made. Unlike the ‘plant based’ artificial meats available today, this is the real deal. Sort of.

About 70 different companies are now “cultivating” a variety of meats in bioreactors, using cells taken directly from animals without harming the animal. Inside the bioreactor, cells are nourished in a soup rich in proteins, sugars, fats, vitamins and minerals; popping out in 2022 should be chicken, blue fin tuna, turkey, bacon and … steaks! It’s entirely possible that this year, or next, you’ll have the choice at Mastros: Instead of the traditional fare du jour, how would you like a perfectly grilled filet mignon on your plate — made without harming the cow?

So, for you vegetarians out there: If you’ve avoided meats because of the harm done to animals, here’s some good news! Yes, you can have your steak and eat it too! It’s a win win!

What does this have to do with economics? Frankly, very little, I’m afraid. I just found it fascinating. But down below, I’ll cut into the meat of the matter. 🙂

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. Significantly. In fact, in the 6 months of Q2 and Q3, growth nominal terms exceed $1.1 trillion of economic activity. The world’s annual GDP is expect to end 2021 near about $93 trillion. Annualized, America’s GDP settling in at $23.17 trillion — still around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are your big players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

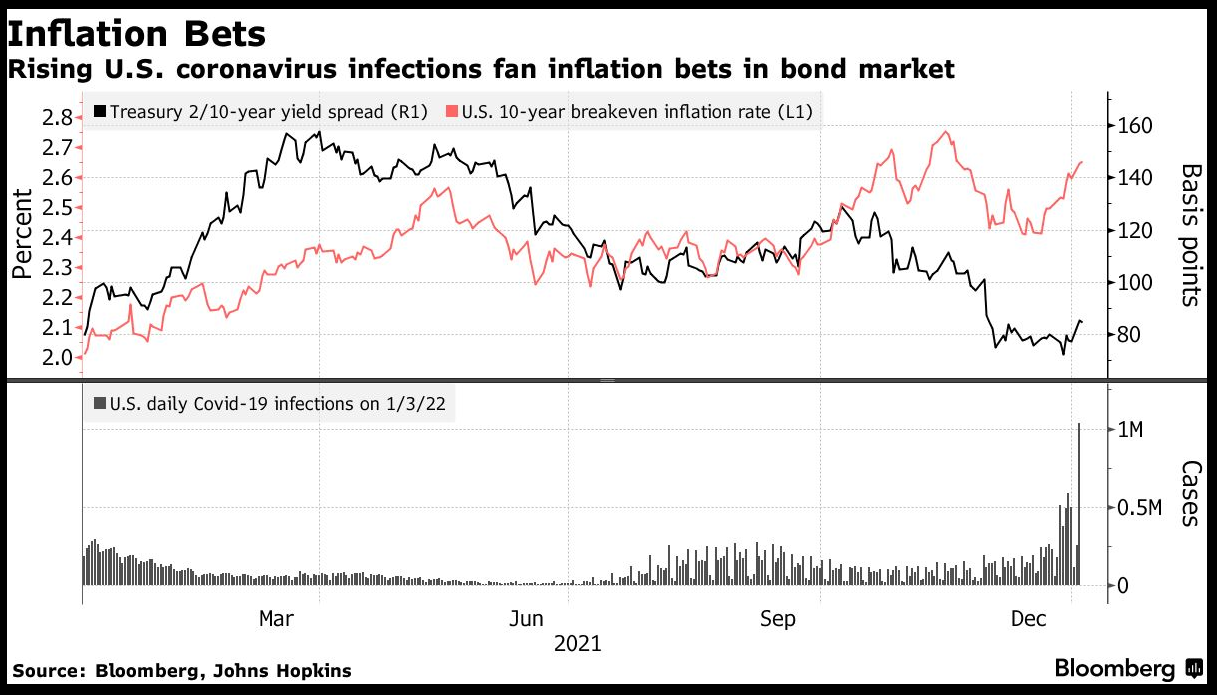

The global financial markets are always interesting. Take the 10-year Treasury, for example. Closing out 2021 at a yield close to 1.5%, just days later this yield is up to close to 1.7%. The oft-quoted reasons include the FED slowing bond purchases, their forecasted 2022 rate increases, and “shrinking balance sheet” discussions highlighted in today’s FED minutes release (from the prior meeting). It’s worth noting the balance sheet currently exceeds $8.75 trillion. But none of those “reasons” are new — in fact, with the exception of balance sheet shrinking, these topics have been kicked around for months.

So why the 20 basis point increase in the 10-year treasury in the past week? Over at Bloomberg, they would have us to believe coronavirus is responsible. Why not, right? We may as well blame Covid for this, too; along with every other current societal ill.

it’s just one more thing to hate about Covid! 🙂

Here’s an interesting graphic, courtesy of Bloomberg:

The ‘pink’ line — the color of a rare T-bone — shows the movement in the US 10-year T over the past year. It’s interesting to note that after a near-term bottom of 1.2%, the yield has been rising. And, it does appear, that the rate rise is highly correlated with US covid-19 infections (bottom graph.) Ostensibly, per Bloomberg, because Omicron is expected to further disrupt supply chains, triggering further shortages, and in a market of relatively stable — or growing — demand for goods and services, additional supply shortages will push up short-term inflation.

Maybe. It’s certainly possible. And this talk-track adds more fuel to the fire of the “inflation is not transitory” debate.

I’m not convinced. I still believe that consumer price inflation is, in fact, transitory. Because transitory is not a matter of months — I believe its a matter of measuring over a year or two. Sure, the supply chain disruption is a very serious short-term problem. But I still believe it is short-term. Used car prices will come down. Other prices, too, will decline when supply chains heal. “Owner’s equivalent rent” however may remain fairly high for a while … and I feel this may be one of the most persistently inflationary components of the CPI and the PCE.

Rent in this case is housing rent. But rents are also skyrocketing in the industrial real estate sector. Industrial, fulfillment, and logistics space are all in warehouses. And demand for this type of real estate is thru the roof.

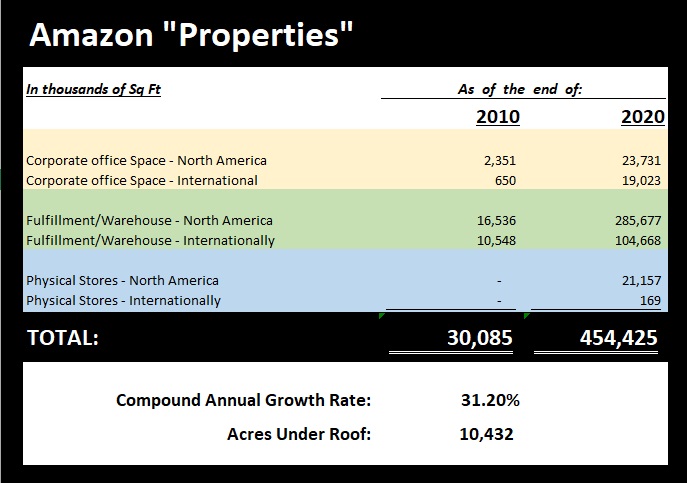

Many feel Amazon is responsible for the demand surge and rental rate increases. Their accumulation of logistics space, both here in American and around the world, has been downright voracious. Take a look at the comparison below — where we see 2010 and 2020 Amazon occupied space side-by-side:

I took these numbers directly from Amazon public reports filed with the SEC so I know they are audited and accurate. Over the past 10 years, Amazon has grown their occupied space from a little over 30,000 square feet to over 450,000 — a 15X increase. Wow. Amazing.

Is Amazon inflationary?

They certainly have contributed to increased demand and cost within the warehouse/industrial space. In the past 10 years, their 15X increase in occupied space calculates to a 31.2% annual compound growth rate. In 2010, globally Amazon occupied a total of just over 30 million square feet of space – a combination of office and logistics space. Of course, the logistics space was the vast majority. Fast forward 10 years to 2020 and Amazon reportedly occupied over 454 million square feet of space — that’s over 10 thousand acres of space! Again, logistics space was the vast majority … and a new category called “Physical Stores” showed up in the Annual Report. Space, I suspect, is related to Whole Foods – but this is a supposition on my part.

“They’ve been affecting things since 2015,” commented Juan Arias, CoStar Group senior consultant for industrial/logistics. “In 2020, they greatly increased the speed which added to their distribution footprint by 50%.”

That is a staggering statistic. But then again, so is an annual compound rate of growth of 31.2%

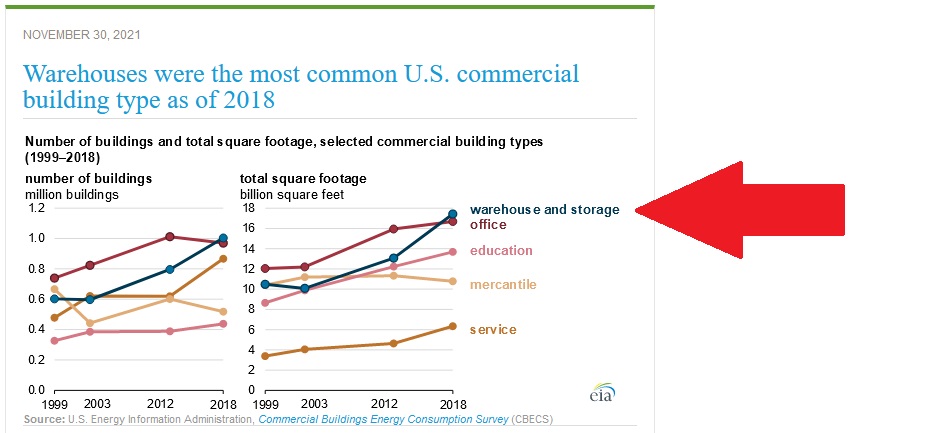

What percentage of all the US “warehouse” type space does Amazon now occupy? I’ve been unable to answer that question precisely. But this gets us close: According to a report from the US government’s Energy Information Administration in November of 2021, during 2018 “warehouse and storage” commercial real estate overtook “office” space in total market share. Take a look:

Summarizing, according to the EIA, here in the US ‘warehouse and storage‘ space increased in size during 2018 to just under 18 billion square feet. As of the end of 2020, Amazon occupied about 285 million of those square feet — only about 1.58% of the total. So clearly Amazon has not been the sole culprit behind the massive demand growth for industrial space.

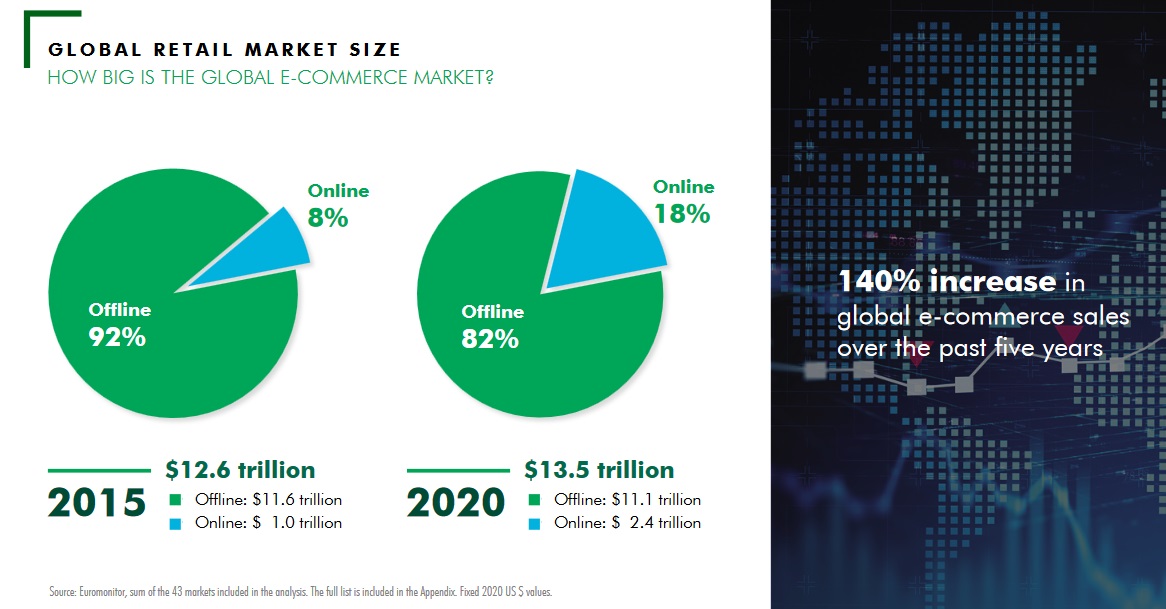

But they are clearly exacerbating the supply / demand imbalance … and they may become a HUGE part of the problem in the future. Consider this graphic:

Between 2015 and 2020, globally E-commerce sales increased from 8% of total retail sales to 18%. This is no fad my friends – this is a trend. And it is accelerating. And as we all know, Amazon is right at the heart of the trend. As is Walmart. And Target. And Home Depot. and Costco. And just about every other major retailer.

But let’s stick with Amazon for the moment. Let’s play the “what if” game. Let’s estimate that the pool of warehouse space in the US increased to 20 million square feet by 2020. Reviewing the Amazon graphic above, we see that when 2021 began, Amazon occupied about 285 million square feet of “warehouse” space in North America – only about 1.4% of the total industrial/logistics space in the US. (Remember, this is an estimate only, as we’re not sure of the 2020 total warehouse space number.) But here’s the point: Assuming E-commerce sales continue to grow exponentially, at least for the foreseeable future, if Amazon’s insatiable demand for warehouse space continues to grow at over 30% per year, within 10 years their footprint will grow another 15X. Meaning, Amazon will occupy over 4.3 billion square feet of warehouse space by 2030. If the supply of US construction of warehouse space increases by, say 5 billion square feet during that same time period, Amazon will occupy about 17% of total US warehouse space in 10 years.

Right, this is wild … and can’t possibly become the reality in 2030. Or can it? 🙂

It’s unlikely that one company could impact the US and global logistics space market like that. And in fact, the more Amazon grows, the more unlikely it becomes. Because in this scenario, the supply / demand imbalance would be impossibly huge. And other disruptions would develop. Ports would be even more clogged. Roads would become near-impassible because of truck traffic. Etc.

But here’s the interesting part: Amazon knows their successes have created their own set of problems.

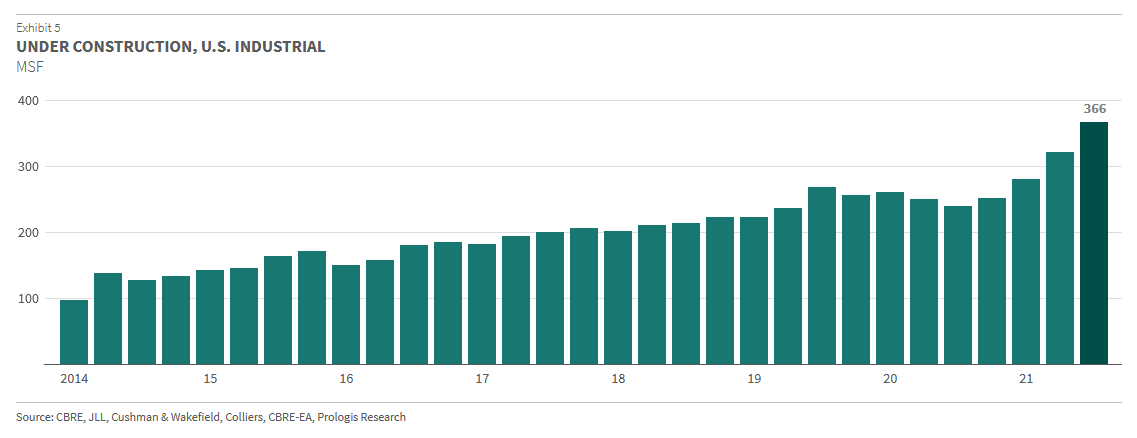

The largest owner of logistics space is Prologis. As of December, 2020, they owned almost 1 billion square feet of warehouse space in over 4,700 buildings in 19 countries. They are massive. And a couple months ago, they posted research on their website titled, “SPACE EFFECTIVELY SOLD OUT.” In other words, if you’re looking for industrial logistics space, good luck, because it’s all gone. Absorbed. Occupied. Supply has expanded significantly, but demand is stronger:

That darker green line above is the 3rd quarter of 2021 … and it represents 366 million square feet of new space! In just one calendar quarter. In the past four (4) quarters, the US has added 1.221 billion square feet of logistics space to existing supply. In just one year.

Here’s the article if you wish to read it: https://www.prologis.com/news-research/global-insights/space-effectively-sold-out

So how can Amazon maintain their growth trend in the face of these obstacles? I assume they will solve this problem in the same way they are solving their transportation issues. They will do it themselves. Don’t be surprised to see Amazon expand their footprint in the logistics space construction business. In years to come, Amazon will probably become one of the largest real estate developers in the world.

It’s interesting that at a time when residential rents are soaring, too, that marketplace cannot seem to add sufficient residential housing supply to temper the rental increases and meet the demand. At least not yet. In the interim, home rents will continue to rise and push up consumer price inflation. But consumer goods will not be a significant part of the consumer inflation issue. In spite of the ever increasing demand for logistics space — and the significant cost increase — the consumer goods companies are wringing cost out of their supply chains at every turn, with sheer size and automation.

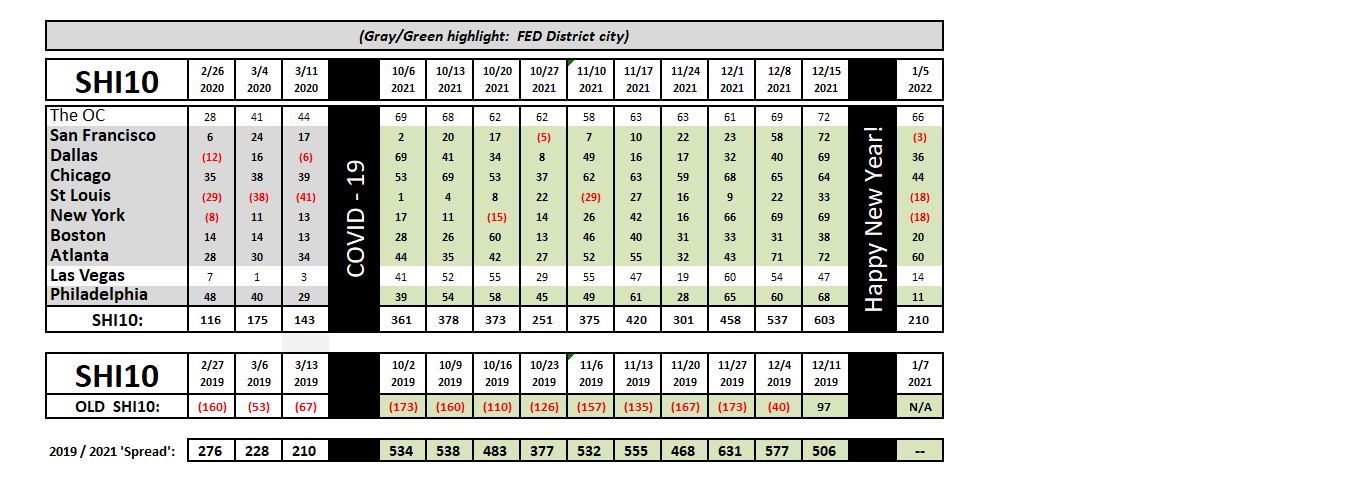

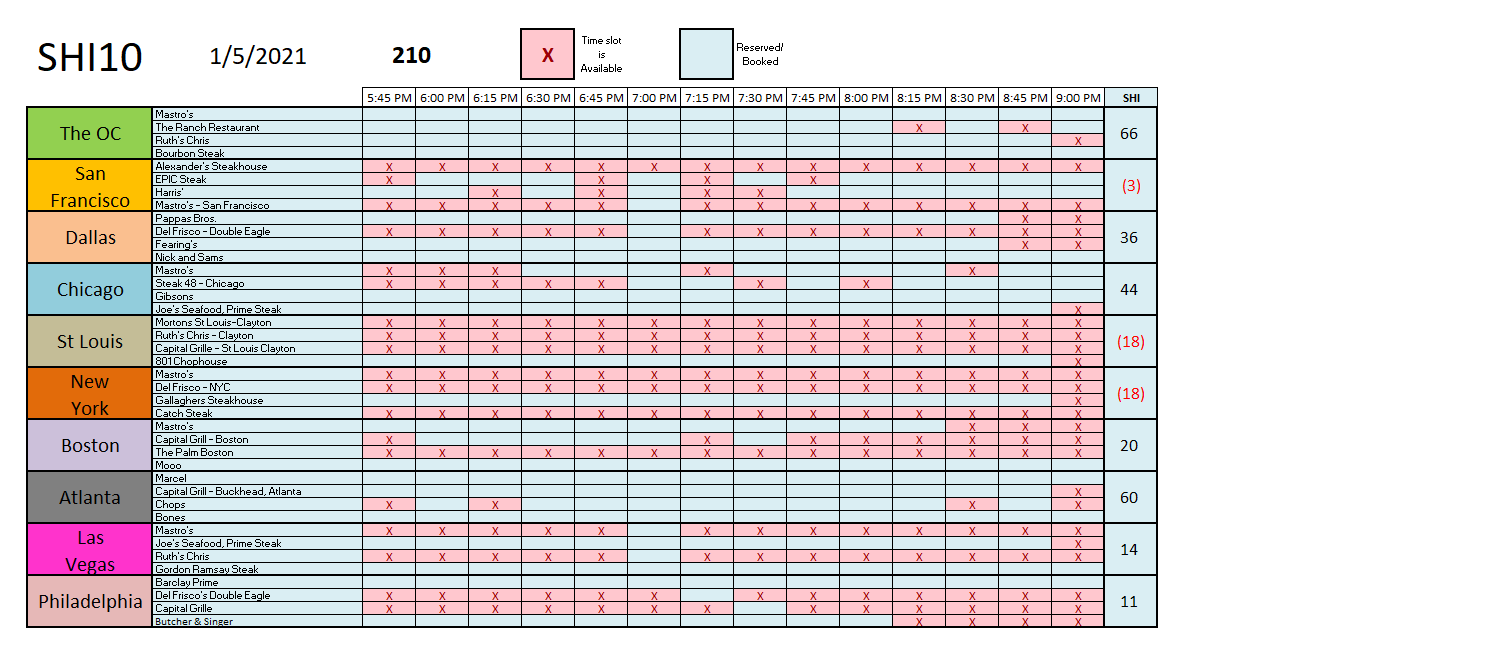

Let’s head to the steak houses. Today’s SHI10 reading is quite a bit lower than the EOY readings in December. But that’s not unusual.

Expensive steakhouse reservations demand remained strong here in the OC and in Atlanta, but demand in our other SHI10 marketplaces was down for this coming Saturday. I don’t find this fact overly surprising given the unrelenting spread of Omicron. I suspect many folks have decided to grill-at-home this weekend:

I began today’s blog saying the financial markets are always interesting. Today was not a kind day to stocks or bonds. Yields were up and stocks were down. Why? We’ve come full circle: The minutes of the last FED meeting suggest they may be more worried about inflation than I am. Which spooked the markets. As I’ve said before, you don’t want to fight the FED … so if they are worried, you should be worried too. But I’m not yet convinced we have much to worry about. I need more inflation data, over a longer time-frame. But in the interim, expect volatility to remain in all things — used car prices, apartment rents, industrial space rents, etc.

But at the same time, corporate earnings after tax have never been higher. Don’t take my word for it, right click on the link below and open it in a new window:

https://fred.stlouisfed.org/series/CP

After-tax earnings are soaring. I expect this trend to continue this year. This is the flip-side of the inflation issue: When prices are up, companies make more money. No big surprise there. The steak houses may show demand weakness for this Saturday next, but our US economy continues to roar ahead. Challenges are numerous, but make no mistake: These are the roaring 20s! Pop the champagne!

<-> Terry Liebman