SHI 1.5.23 — Jobs, Jobs, Jobs. And Money.

SHI 12.28.22 — The Year That Was and Wasn’t

December 28, 2022

SHI 1.11.23 — Economics Used to be Easy

January 11, 2023

By any measure, your investments probably lost value during 2022.

If you were “in the market” during 2022 — any investment market — there was almost no place to hide. Stock markets were down … bond values were down … investment real estate was down … P/E ratios were down and capitalization rates were up. By any measure, it was a tough year for investors.

But it was a great year for jobs. Jobs, jobs, jobs.

Of course, ‘energy‘ investors did great during 2022. Even better than the jobs market. In fact, of the 11 S&P 500 sectors, ‘energy’ was the only sector to finish higher during 2022.

“

Investors hate 2022.”

“

Investors hate 2022.”

With a passion. But it could have been worse. Far worse.

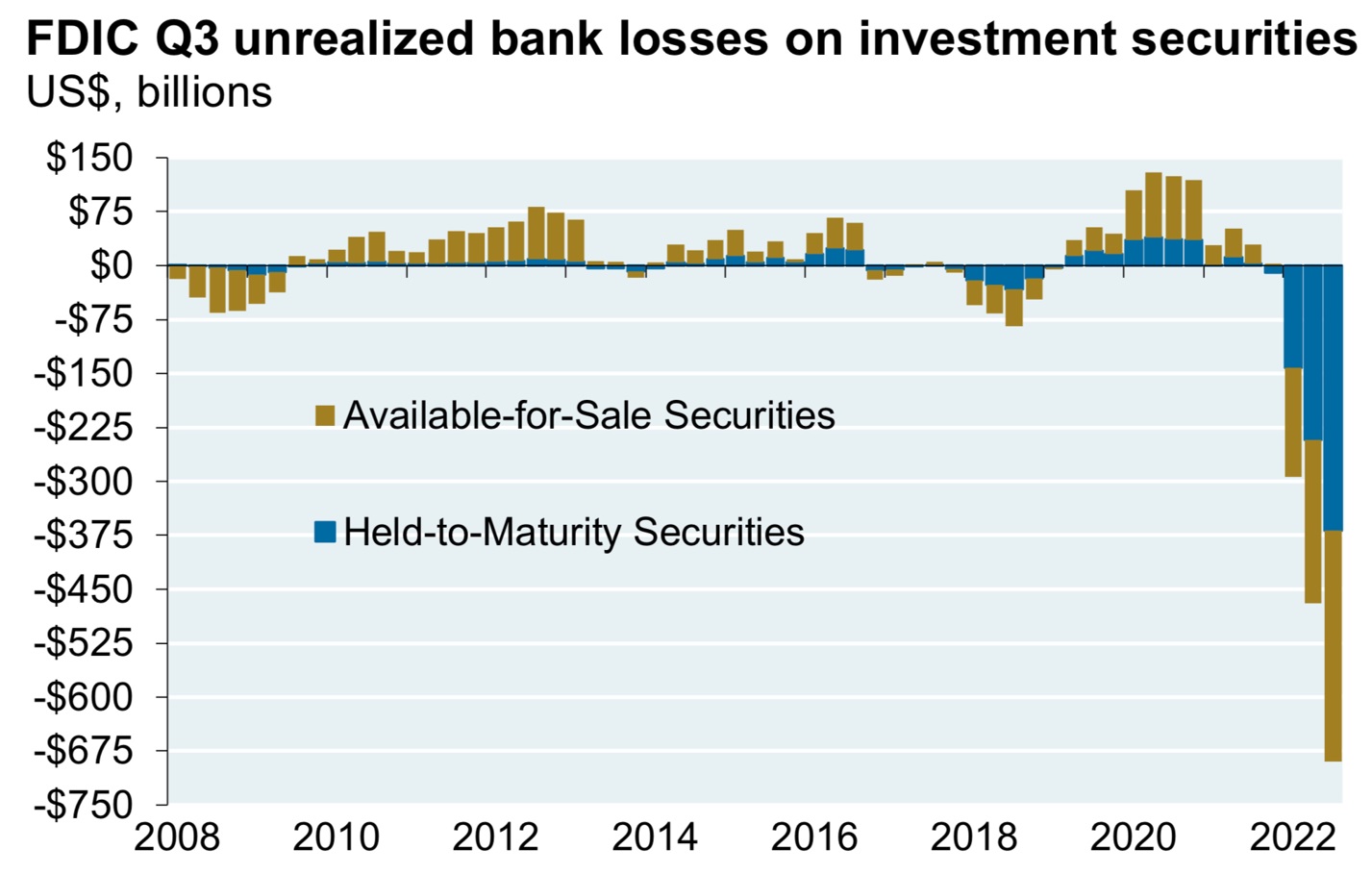

You could have followed American’s largest banks and plowed a bunch of cash into ‘investment grade’ corporate bonds and treasuries. According to the FDIC, “unrealized losses” on America’s bank balance sheets on securities they owned at the end of Q3, 2022 totaled $689.9 billion. Ouch. Yes, you read that right. At the end of Q3, banks had unrealized losses on their bonds exceeding 2/3 of a TRILLION dollars. Holy Canole!

OK, no doubt, that’s bad. But let’s add some perspective here: In the aggregate, America’s commercial banks earned $71.7 billion in Q3. Q1 and Q2 were almost as good. In fact, the banks have collective earned over $50 billion per quarter for years now. That’s more than $200 billion per year in profits. Good. So how deep a hole is almost $700 billion in “unrealized losses” … should American’s be worried about bank solvency? Is our money safe in Chase and Bank of America and other smaller banks? SHOULD WE PANIC NOW !?!? Naah … relax. It will all work out fine.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. At the end of Q3, 2022, in ‘current-dollar’ terms, US annual economic output rose to $25.74 trillion. Thru Q3, America’s current-dollar GDP has increased at an annualized rate exceeding 7%. The world’s annual GDP rose to over $100 trillion during 2022. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the 3 big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

The FDIC, for obvious reasons, closely tracks the performance of America’s banks. Here is a link to the most recent quarterly status report (right click, open a new tab):

https://www.fdic.gov/news/press-releases/2022/pr22082.html

In the section titled “Unrealized Losses on Securities Increased” appeared this comment:

“Unrealized losses on securities totaled $689.9 billion in the third quarter, up from $469.7 billion in the second quarter. Unrealized losses on held-to-maturity securities totaled $368.5 billion in the third quarter, up from $241.8 billion in the second quarter. Unrealized losses on available-for-sale securities totaled $321.5 billion in the third quarter, up from $227.9 billion in the second quarter.”

And you thought you made some bad investments during 2022. 🙂

Consider this chart:

Why did our banks make such poor bond investment choices during 2022? For the same reason you and I did: The FED. After more than a decade of near-zero interest rates, the FED raised interest rates at a faster clip than in any prior cycle. Smart or dumb, risk-adverse or speculative, I suspect nearly every investor was adversely impacted in 2022. Except for oil investors … which I’ll discuss a bit more below.

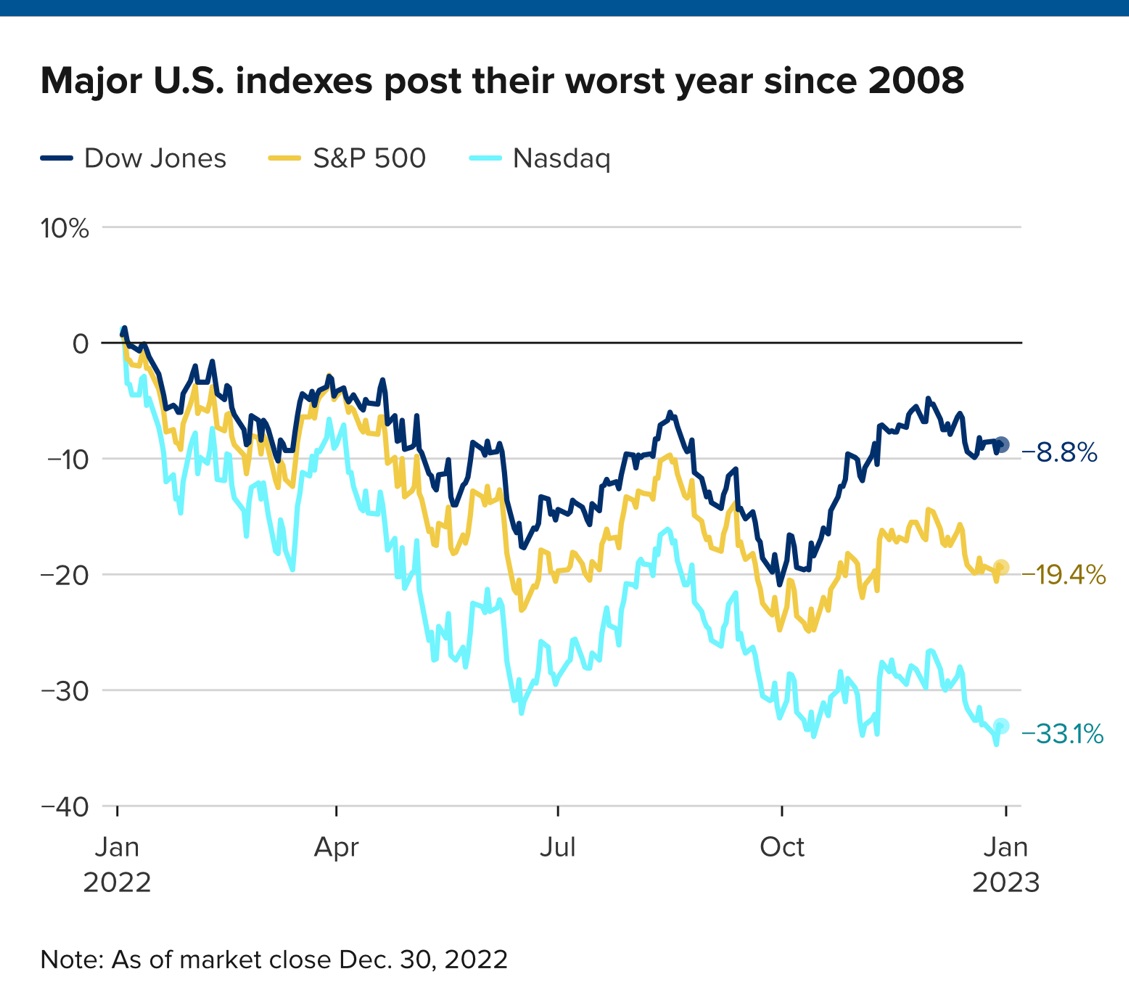

Of course, some people did worse than others in 2022. Technology investors were hammered. $1 dollar invested in Cathy Wood’s ‘ARK Innovation ETF‘ in January of 2022 would be worth about 33 cents today. Double ouch. The performance of the three (3) major US indexes was wildly inconsistent:

Isn’t that amazing? I thought so.

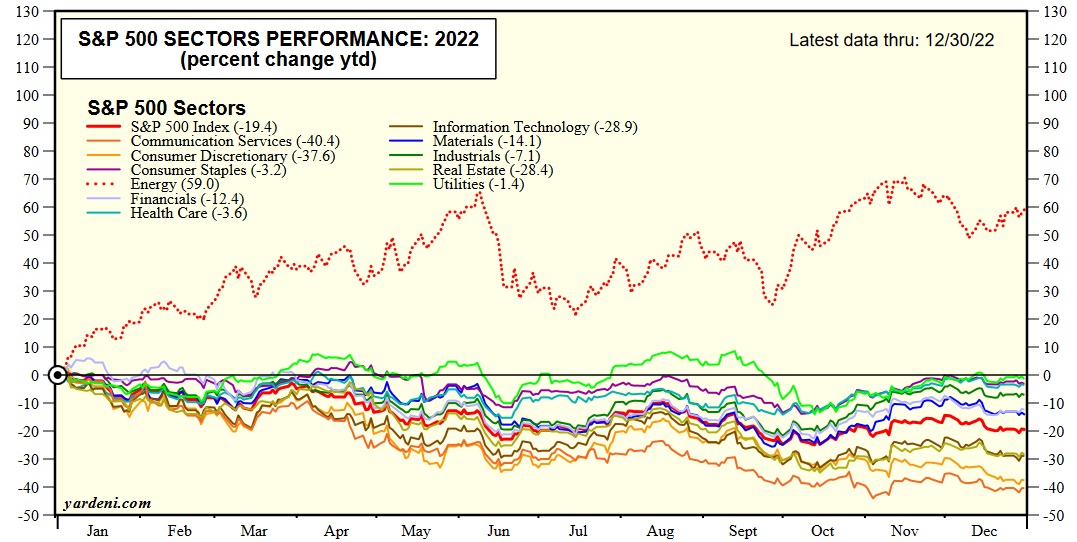

It is a rare year when the S&P500 index loses close to 20% in value. But the story doesn’t end there. As we dig a bit deeper and see the performance of the 11 individual sectors, the divergence is even more staggering. Consider the graphic image below, courtesy of our friends at Yardeni research:

“Communication Services”, “Consumer Discretionary”, “Information Technology” and “Real Estate” were all slammed in 2022 with value declines of about 40%, 38%, 29% and 28%, respectively. Six other sectors didn’t do too badly. And thanks to Putin’s horrific attach on Ukraine, oil company stocks did quite nicely during 2022 — up about 59% for the year.

Things change. Right? Remember the per-barrel price back in early 2020? Negative? That’s right. Occidental’s stock price slid to about 10 bucks. It trades at over $60 today. Warren Buffet is quite happy with his Occidental investment these days. 🙂

The banks, on the other hand, are not overly happy with their bond investments. But it’s your fault. You gave them too much cash. Yes. I’m talking to you:

Remember to ‘right click’ and open in a new tab. Anyway, this link will bring you to a FED ‘notes’ piece called

Excess Savings during the COVID-19 Pandemic

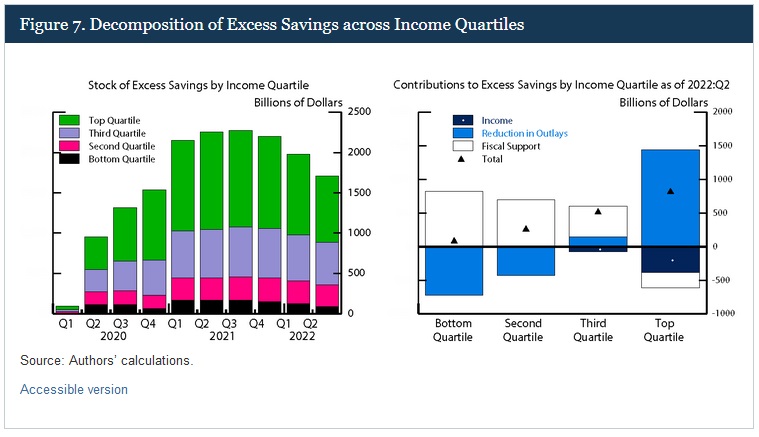

Where do you suppose all those excess savings went? Right. Into the banks. They had to do something with all that cash we gave them! They couldn’t stick it all in the mattress — they ran out of mattresses! Take a look at this graphic, Figure 7 from the FED piece:

You have to love the FED-speak: “Decomposition of Excess Savings across Income Quartiles.” Yeah, I know. Fortunately, the image is fairly self-explanatory. The GREEN is the top 25% income group. It is no surprise they saved the most during the pandemic. How did they save the most? Take a look at graphic on the right. Correct. They didn’t spend it. “Reduction in Outlays” is how the FED characterizes it. Ironically, the income to this group shrunk significantly during the pandemic. Again, make sense. Poor rich people.

Anyway, let’s get back to the banks. They had a huge cash influx. So they bought bonds. Of different durations. The shortest duration group fit easily into the “Held-to-Maturity” securities, meaning that these bonds will return 100% of the amount invested upon maturity. Most of the unrealized losses fall into this bucket — about $370 billion. So eventually, when these securities mature, these losses evaporate. The balance of the losses — about $320 billion — reflect the current “mark-to-market” value loss the backs would take if they sold these securities at current market prices. Something, I suspect, they have no current plans of doing. These are high quality, income producing assets. Why sell?

Which brings us full circle back to the dismal 2022 stock market. Neither the individual investor or American’s banks actually lost a penny in 2022. Unless you sold your stocks or bonds. Both gains and losses are only realized upon sale. Right? So, like the banks, your losses are unrealized. Assuming the financial markets recover in the not too distant future, your unrealized losses could diminish … and even become unrealized gains! That’s right — you might actually “make money” in the stock market! I know … crazy talk, right? Hope springs eternal. 🙂

The jobs market, of course, did the best during 2022. Amazon tried to hire everyone. You think I’m kidding? Well consider these numbers, courtesy of CNBC: At the end of Q4, 2019, Amazon employed 798,000 people. Less than 2 years later, at the end of Q3, 2022, that number had increased to 1,544,000! During this time, Amazon alone added close to 3/4 of a million workers to their payroll. Wow! And Meta and Salesforce both added 30,000 new folks to payroll in the same time-frame.

Perhaps it’s not surprising, then, that once again the JOLTS report — job openings, labor turnover — continues to surprise. Released earlier today, the JOLTS report tells us “the number of job openings was little changed at 10.5 million on the last business day of November.” Little changed indeed. The November number was almost identical to the October number. And the November, 2022 number — 10.458 million — is almost identical to one year ago, November of 2021, which reflected 10.922 million job openings.

I believe this is the FEDs most vexing problem. If asked, I suspect the FED would agree that their efforts in 2022 have brought home values and rents “under control,” took the froth out of the financial markets, and tamped-down consumer inflation. The only sever and lingering problem is JOBS! Drat! There are simply too many of them … and too many employers are still looking to add more!

But this too is likely to change. Amazon, Meta and Salesforce are now planning more cuts — not more hiring. I think we’ve seen ‘peak employment’ for this cycle. 2022 may have been a great year for the jobs market, and a really bad year for the investment markets, but 2023 is likely to play out quite a bit differently. Grab some popcorn and stay in your seat … this is gonna get interesting.

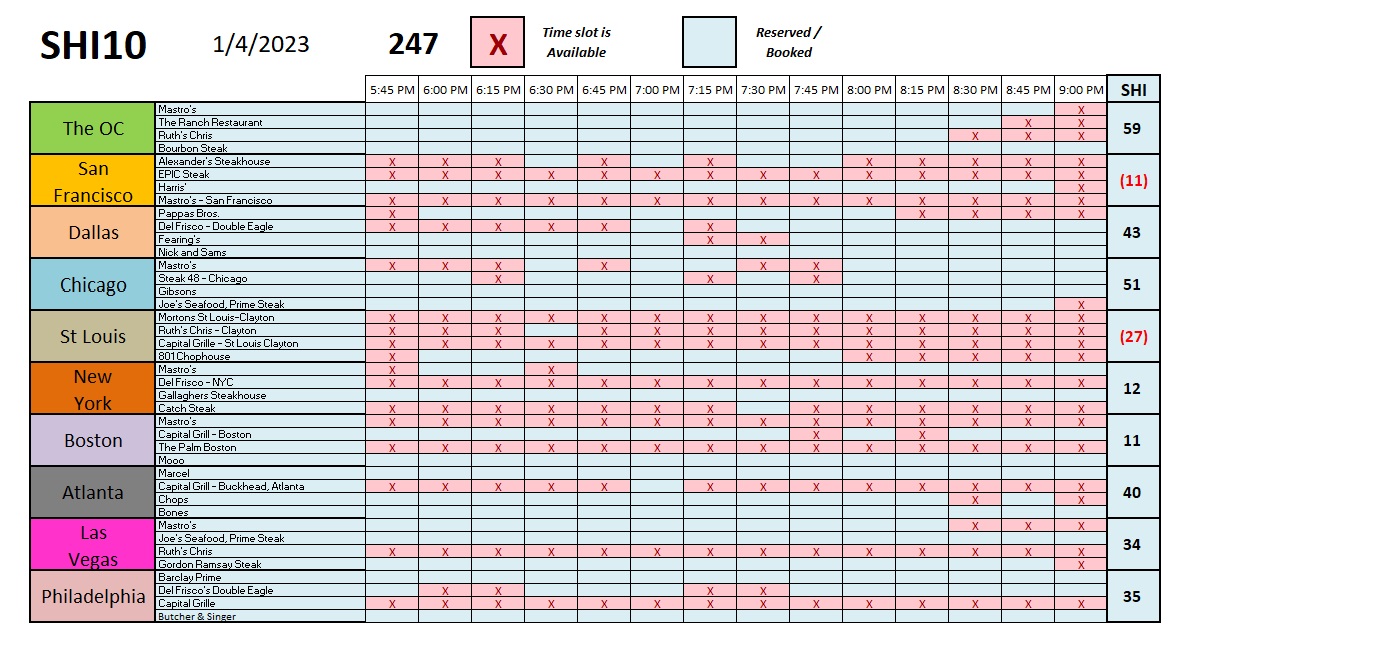

To the steakhouses? Here is this weeks SHI10:

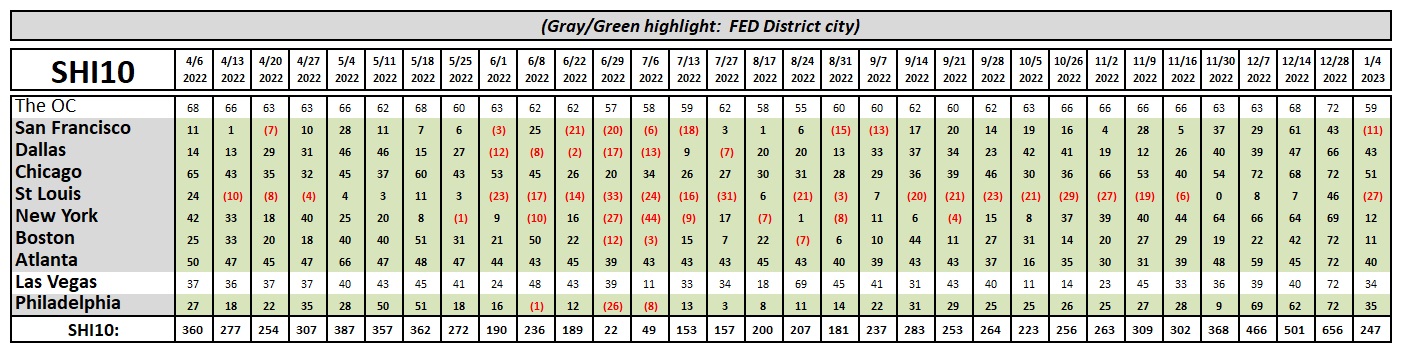

Clearly, ‘New Year’s Eve’ happens only once a year. Today’s SHI10 — reflecting expensive eatery demand exactly one week from NYE reflects much softer demand for this coming Saturday. San Francisco and St Louis — our two “S” cities — both turned negative this week. There are plenty of open tables there. The OC remains resilient, demand in Dallas is strong, and the other cities are a mixed bag, as usual. Here’s the longer term trend report:

Yep … this is definitely a weaker week than last week. Keep in mind that in all the years I’ve been tracking expensive steakhouse reservations, Q1 is often weak. Thus, I’m not at all surprised to see the significant slide in demand.

Earlier today, the FED released the minutes from their mid-December FOMC meeting. Some highlights:

“Participants generally concluded that there remained a large imbalance between labor supply and labor demand, as indicated by the still-large number of job openings and elevated nominal wage growth. Participants commented that labor demand had remained strong to date despite the slowdown in economic growth, with a few remarking that some business contacts reported that they would be keen to retain workers even in the face of slowing demand for output because of their recent experiences of labor shortages and hiring challenges.“

See? They remain concerned about excessive labor demand. Very concerned. And on the issue of reducing the Funds rate later in 2023 … they commented:

“No participants anticipated that it would be appropriate to begin reducing the federal funds rate target in 2023. Participants generally observed that a restrictive policy stance would need to be maintained until the incoming data provided confidence that inflation was on a sustained downward path to 2 percent, which was likely to take some time. In view of the persistent and unacceptably high level of inflation, several participants commented that historical experience cautioned against prematurely loosening monetary policy.”

Hmmm. No participants. Not even one. Interesting.

When pressed on this issue by a financial reporter who commented the FOMC‘s conviction to only raise rates in 2023 — but not consider a rate cut — Powell commented,

“Well, you have to understand. The FED MUST CRUSH INFLATION before wage expectations and inflation get out of control! WE MUST! Even if the economy stumbles, WE WILL NOT LOWER RATES IN 2023! Even if 1 million people lose their homes to foreclosure, shortly thereafter becoming homeless, WE WILL NOT LOWER RATES IN 2023! In fact, even if our rate increases CRUSH the US economy, DESTROYS our financial markets, and American’s are in misery, WE WILL NOT LOWER RATES IN 2023!”

OK. I made that whole thing up. Powell said no such thing. Because these comments are patently absurd. Of course the FED will change direction if incoming economic data warrants a direction change. It’s worth remembering that in 2021 the FED and their “participants” said they weren’t even thinking about thinking about raising rates. And yet they did. Shortly thereafter.

My point? Things change. They are saying what they should … at this time. And if unemployment spikes and the economy begins to struggle, I suspect so will the FED speak. And FED rate reductions will follow shortly thereafter.

Enjoy the popcorn. 🙂

<:> Terry Liebman