SHI 10.21.2020: Coming Soon!

SHI 10.14.20: How to Spend $2.2 Trillion

October 14, 2020

SHI 10.28.2020: Tomorrow is the BIG DAY!

October 28, 2020

There is nothing showing at the Aurora Theater in New York City. Because the theater remains closed since the beginning of ‘The Great Lockdown.’

Equally troublesome, there doesn’t appear to be anything coming soon. Why? Well, when ‘Hollywood‘ takes an 8-month hiatus from filming and production, whatever the reason (in this case, of course, COVID lockdowns), there’s not much “in the can” and ready to be shown on the big screen. Or any screen, for that matter. And because most people are afraid to sit in a (crowded) movie theater, studios are holding back films that are ready for release. What a mess.

Movie theaters are clearly in the group of “the biggest losers.” Like cruise ships and Broadway, they face staggering obstacles in the coming months and years. Other parts of the economy, by comparison, are faring much better. Its definitely a mixed bag out there.

“

How will the Global Economy recover from COVID?”

“

How will the Global Economy recover from COVID?”

The International Monetary Fund just updated their “WORLD ECONOMIC OUTLOOK.” With a sub-title: ‘A long and Difficult Ascent.’ Indeed. It’s an interesting read … and ONLY 204 pages so dive in! OK, ok, I understand … no worries, I’ll just summarize it for you. But for those hearty souls who love this kind of stuff, here the hyperlink …

https://www.imf.org/~/media/Files/Publications/WEO/2020/October/English/text.ashx?la=en

… and in the blog below you’ll find my summary.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Before COVID-19, the world’s annual GDP was about $85 trillion. No longer. It shrank. Until recently, annual US GDP exceeded $21.7 trillion. Again, no longer. According the the Q2 final numbers, annual US GDP is down to $19.5 trillion. We can thank the Great Lockdown for this one. But what has not changed is the fact that together, the U.S., the EU and China still generate about 70% of the global economic output.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

Like the Aurora Theater, the economies in the world’s developed countries have taken a massive hit from the COVID inspired shutdowns. Unlike the media, I will not say that COVID caused these economies to shrink; no, the cause was not COVID. The economic malaise is the result of the shutdown inspired by COVID. The shutdown was a choice. A country could have chosen to ‘remain open,’ as Sweden did.

For public health purposes, governments mandated that people remain in their homes and businesses close. No alternative choice was considered. Except in Sweden.

Arguably, perhaps, our leaders made the only intelligent choice: Perhaps a complete and protracted shutdown was the only possible way to prevent runaway disease and deaths. But I’ll leave this discussion, for now, to those who struggle with such choices … and we’ll let our leaders and the history books assess the results.

Like a coin, every choice has a “flip side” or a trade-off. Once option ‘A’ is selected, option ‘B’ is not longer an option. The Great Lockdown was the choice made by most of the developed world … and the world must now deal with the implications of that choice.

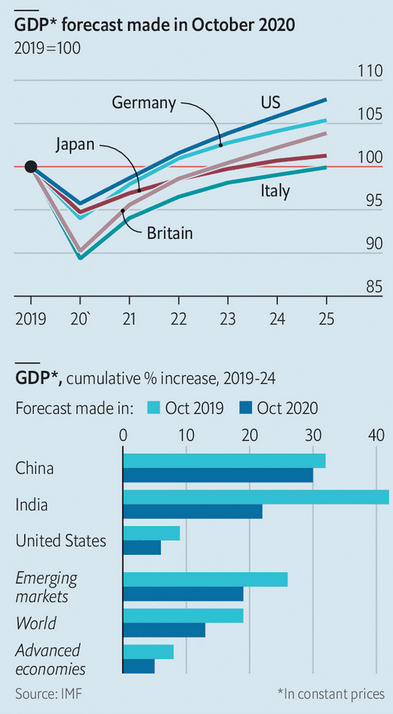

The chart to the right is not from the IMF report. It is actually cut from an Economist magazine article that discussed the IMF forecast. But I found it to be a great summary of the forecast:

- <> Global growth is projected at a negative 4.4% during 2020.

- <> 2021 will bounce back, with the global growth rate reaching 5.2% in 2021.

- <> The US will recover the quickest: America’s GDP will return to the 2019 level in 2022.

- <> Germany, too, will pass its 2019 GDP numbers in 2022.

- <> Japan and England, however, will not fully recover until 2023.

- <> Italy, unfortunately, will not exceed their 2019 performance until 2025.

The second part of the chart to the right is also quite interesting. Take India, for example. One year ago, in October of 2019, the IMF believed India’s economy would surge more than 40% by 2024. They now believe India’s economy will grow much slower … probably achieving only about 1/2 the growth previously expected.

It’s interesting to note the IMF expects the ‘emerging markets’ (EM) to be more resilient. They forecast about a 25% reduction in EM GDP thru 2024.

And how is China’s economy expect to perform? They stand alone. China is forecast to be the only one of about 190 countries across the globe that will feel very little long-term impact from the Great Shutdown.

The IMF summarized their findings as follows:

“We are projecting a somewhat less severe though still deep recession in 2020, relative to our June forecast.

The revision is driven by second quarter GDP outturns in large advanced economies, which were

not as negative as we had projected; China’s return to growth, which was stronger than expected; and

signs of a more rapid recovery in the third quarter. Outturns would have been much weaker if it weren’t

for sizable, swift, and unprecedented fiscal, monetary, and regulatory responses that maintained disposable

income for households, protected cash flow for firms, and supported credit provision. Collectively

these actions have so far prevented a recurrence of the financial catastrophe of 2008-09.”

And on the topic of sovereign debt and interest rates, they had this to say:

“Moreover, sovereign debt levels are set to increase significantly even as downgrades to potential output

imply a smaller tax base that makes it harder to service the debt. On the plus side, the prospects of low

interest rates over a longer period, alongside the projected rebound in growth in 2021, can help alleviate

debt service burdens in many countries. To ensure that debt remains on a sustainable path over the

medium-term governments may need to increase the progressivity of their taxes and ensure that corporations

pay their fair share of taxes while eliminating wasteful spending.”

In other words, you can expect your federal (and state) income tax rates to increase. Probably fairly soon.

Moments ago, the FED released the October 21, 2020 ‘Beige Book.’ Once again, permit me to summarize:

-

- <> Economic activity continued to increase across all FED Districts,

- <> Manufacturing generally increased, housing markets continued to experience steady demand.

- <> Commercial real estate conditions continued to deteriorate, with the exception being warehouse and industrial space.

- <> Restauranteurs expressed concern that cooler weather would slow sales, as they have relied on outdoor dining.

- <> Banks reported that delinquency rates may rise in coming months, citing various reasons; however, delinquency rates have remained stable.

Once again, it’s a mixed bag.

The bottom line: The US and other developed nation economies continue to heal. The direction of growth is up … but the path is serpentine. And different industries continue to have vastly different experiences. The worst should be behind us, but we’re not out of the woods yet.

- Terry Liebman