SHI 12.4.19 – The Issue of Unintended Consequences

SHI 11.27.19 – 400 Years Ago

November 27, 2019

SHI 12.11.19 – Folks are Working!

December 11, 2019

“Have you ever been eaten by a crocodile?”

Neither have I. But, unfortunately, quite a few folks living in Ivory Coast have. Well, they used to live in Ivory Coast.

The country’s first President, Felix Boigny, built a large palace for himself and surrounded it with a crocodile-filled lake. He liked the image the amphibians generated for his administration. And, further more, they were a gift from the dictator-next-door in Mali. He must have been thinking, “How can I turn down such a generous gift?” 🙂

Crocs were not indigenous to the region, but they seemed to like their new home. But in 1993, Felix kicked the proverbial bucket, the country’s new leaders preferred to work in the nation’s commercial capital, leaving the palace ignored and slipping into disrepair. Soon thereafter, the President’s “pets” decided they were hungry, and took off looking for a new home, one where they could find a few Steakhouses and, if not Steakhouses, at least some other tasty morsels. Years passed. Having found copious food sources, they reproduced extensively and now, unfortunately, Ivory Coast has a problem. According to a local teacher, Souaga Gerard, “If you go near the water, they will eat you.”

Which brings me to the topic of today’s blog: Global debt.

Like a croc, debt can literally eat you alive. If you let it proliferate to the point that it can no longer be controlled. Ouch.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will be true for years to come.

But is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is about $85 trillion today. According to the most recent estimate, US ‘current dollar’ GDP now exceeds $21.53 trillion. In Q3 of 2019, nominal GDP grew by 3.5%, following a 4.7% annualized growth rate in Q2. The US still produces about 25% of global GDP. Other than China — in a distant ‘second place’ at around $13 trillion — the GDP of no other country is close. The GDP output of the 28 countries of the European Union collectively approximates US GDP. So, together, the U.S., the EU and China generate about 70% of the global economic output.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

Global debt is an important economic topic. Frankly, it is probably one of the most important.

One’s ability to repay a new debt is typically a critical consideration when making the decision to borrow in order to buy something new. Whether the purchase is large or small, you think about it. Carefully. And if you believe the purchase warrants the additional debt load, you make the purchase.

Of course, this doesn’t mean you are correct. Future conditions may prove that decision to be a bad one. If your income declines for some reason, or the interest rate on that new (or prior debt) increases precipitously, you may no longer be able to “service” that debt. And therein lies the problem with debt. Things change.

Debt is often the one thing that gets individuals and counties into trouble. Throughout history, time and time again, the decision to take on excess debt has led to financial disaster. Look at what’s happening in Argentina right now.

It’s interesting to note, and worthwhile to remember, that for every debt there is a lender. Borrowers can not exist without lenders. Many of the lenders fueling the current borrowing binge are located in Asia — the countries with large trade surpluses. Over the past 5 years, the countries that make up east-Asia have averaged more than $500 billion each year in trade surpluses. And they are willing to lend it out. The International Monetary Fund tracks this stuff. The IMF calculates that:

- Taiwanese life insurers own 18% of all dollar debt issued by non-American banks.

- Japanese banks own about 15% of globally issued collateralised loan obligations, potentially risky securitisations of corporate debt.

- South Korea’s national pension fund, the world’s third-biggest, with nearly $600bn in assets, plans to double its investments in foreign bonds over the next five years.

Clearly, in the far east and elsewhere, lenders are plentiful. And they’re all searching for yield. But the borrower’s ability to repay the debt, at some future date, must also be assessed by the lender. Interest payments are great … but a return of principal is better still. So the lender considers important questions before making a lending decision:

- Should I lend more to this borrower?

- Will this borrower be able to repay the debt?

- What “secondary” source or sources of repayment does the borrower have?

Great questions. Because here’s a fact you probably didn’t know:

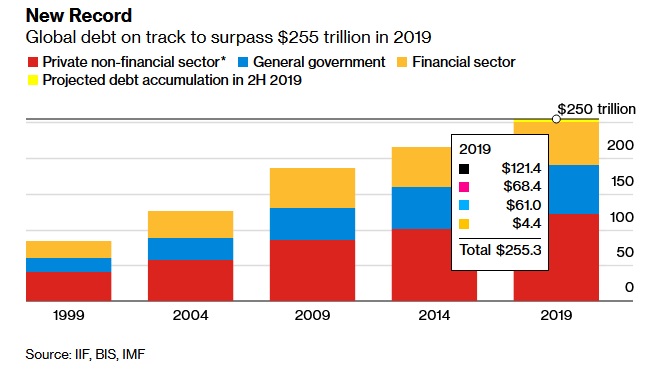

Global debt has reached a new high water mark:

How much higher is global debt, you ask, than in prior years? Here are the numbers:

- 2014: Global debt totaled $215.1 trillion.

- 2009: The year after the Great Recession began, and about 10 years ago, global debt was approximately $186 trillion.

- 2004: About 15 years ago, global debt totaled $126.4 trillion — about 1/2 the current load.

- 1999: 20 years ago, the pile of global debt was a paltry $83.9 trillion.

First, note the number is in TRILLIONS of dollars. To put this in perspective, remember that US GDP is currently about $22 trillion annually. The global GDP is around $85 trillion. Which means the total global debt load is equal to approximately 3X global GDP.

In the past 5 years, the global debt load has increased by about $40 trillion. Let me put that in perspective: $40 trillion dollars is about one half of the entire global economic output for one year! That, my friends, is a lot of debt!

Long-time readers of my blog know that during this same time-frame — between 2014 and today — global interest rates have fallen to the lowest levels the world has ever seen. Ever. In the past 4,000 years rates have never been this low.

-

Have the exceptionally low rates inspired the borrowing binge?

-

Can the borrowers afford to pay the debt service?

-

What else might be going on here?

Yes, these exceptionally low rates have triggered much of the borrowing. Here are some examples:

- Large public corporations with excellent credit ratings have borrowed on the cheap and used the proceeds to buy-back their own stock. Their rationale: If their return on equity significantly exceeds the cost of the debt, they believe the debt is wise.

- Weaker corporations here, in Europe and in China, have issued an increasingly large amount of ‘junk bonds.’ Their rationale: The exceptionally low cost of debt enables them to leverage operations and “juice” their return on equity. Clearly, they believe, the debt is wise.

- Large real estate corporations with excellent credit ratings have borrowed on the cheap and used the proceeds to acquire additional real property assets. Their rationale: If their return on equity significantly exceeds the cost of the debt, they believe the debt is wise.

- Pension funds have borrowed money on the cheap to “juice” their sub-par investment returns. Their rationale: If their return on investment significantly exceeds the cost of the debt, they believe the debt is wise.

- Individuals have used borrowed money to buy cars, houses, etc. on the cheap because the money is cheap! Their rationale: I can handle the payments because I have a great job!

These decisions, in my opinion, perceived as wise today could be something very different if the global economy were to slump. For now, the borrowers all have an excellent plan to pay the debt service. And their plans are sound. As long as corporate stock holds value, real property remains leased, and short-term rates don’t spike, all is good!

Which brings us full circle back to the topic of debt. The biggest borrowers, by far, are countries. Today, many developed countries are unhappy with their GDP growth rates. And many are looking for a fix. For years, “monetary policy” — meaning managing (manipulating) short term rates — was the tool. It is no longer working.

And now there there seems to be rising evidence that countries may be reaching for a new tool: “Fiscal policy.” Meaning instead of using interest rates to “juice” the economy, the country would take on even more debt and invest those newly acquired funds in-country for things like infrastructure improvement.

If you can borrow money at a near-zero interest rate, should you? Japan seems to think so. As I write this blog, they are “preparing” a 13 trillion yen “stimulus package” intended to boost their economy. And since their 10-year BOJ debt yield is currently a negative 0.04 percent — just about zero — does it make sense to take on the debt and invest in infrastructure that should generate some return? After all, it’s easy to beat a zero return on their investment, right?

Probably. Certainly in the short run. But in 10 years that 17 trillion yen must be repaid. It may have been interest-free for 10 years, but now Japan must ‘pay the piper.’ And they already have the highest debt/GDP ratio in the world. Hmmm….

Germany, on the other hand, could easily consider a similar plan. And for them it’s an easy choice. Their 10-year bond yield is currently a negative 0.31%. They could borrow a bunch of euro, invest in infrastructure, and receive annual payments from their borrowers! Wow … that sounds too good to be true! Yet, today it is true. And Germany has one of the lowest debt/GDP ratios in the world. So taking on debt — effectively for free — to increase economic productivity via infrastructure investment makes a lot of sense, right?

Interesting issues indeed. Good choice … bad choice … I guess we’ll know in 10 or so years. Debt. Gotta love it. I’ll leave it here for today … let’s head over to Mastros and see how those T-Bones are selling this week.

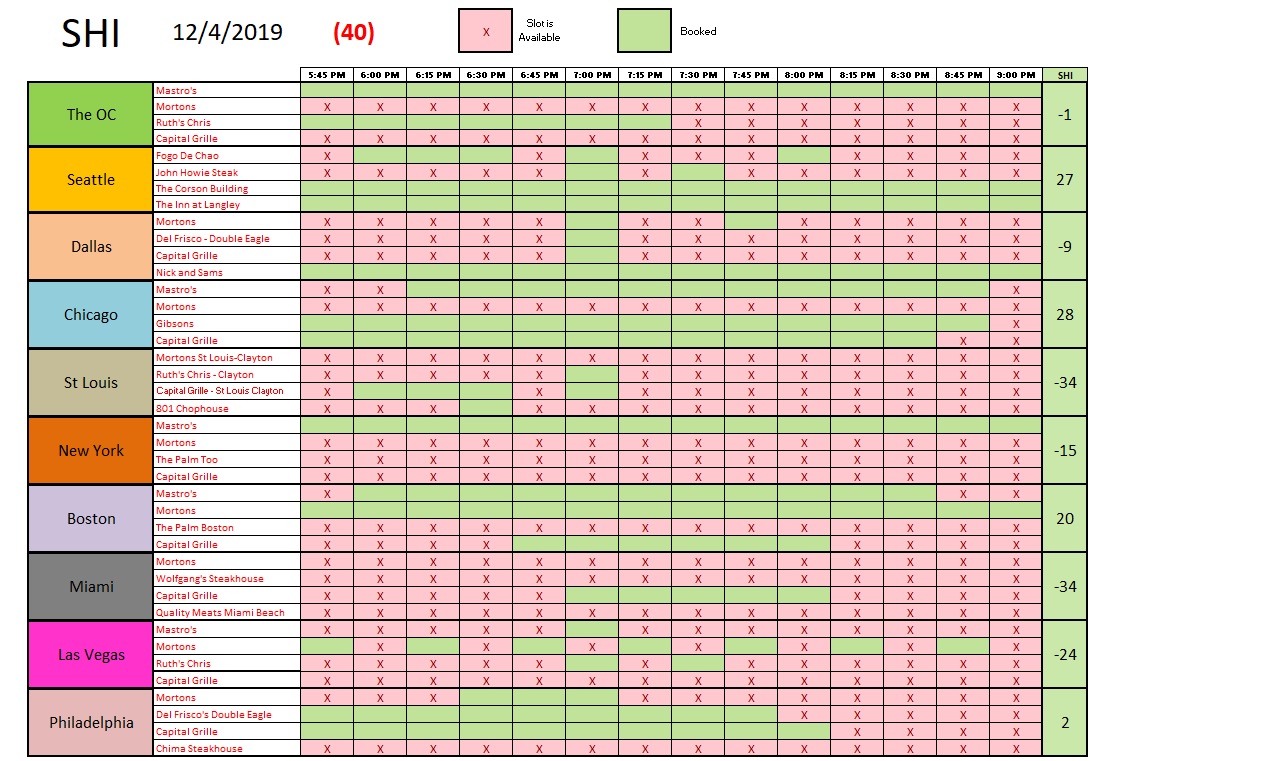

Pretty good, it turns out. Reservations this Saturday at our pricey Steakhouses are flying off the shelf! 6 of the 40 restaurants we track were fully booked this morning at 11 am, for a table for 4 this Saturday. Impressive. Then again, December is usually a pretty good month for the expensive eateries. ‘Tis the season. Let’s take a glance at the longer term trend report:

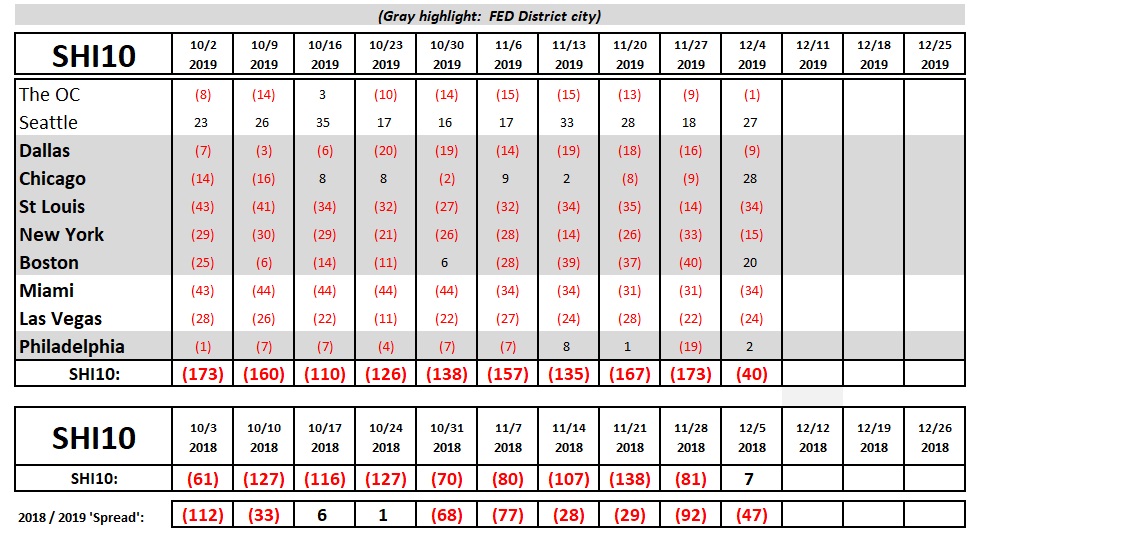

Yep, reservation demand is looking strong for the week. This week last year the SHI was actually in the black! Not this year. But this week’s SHI10 reading is far better than any recent measure.

I wish I could say this improvement suggests an improving economy. I cannot. What I can say is this move is consistent with SHI readings in previous Decembers. December improvement is commonplace … and even with this improvement we’re still far behind SHI readings from one year ago. The SHI10 is telling us that the US economy is doing OK … but not much better than that.

– Terry Liebman