SHI 12.6.23 – ‘Tis the Season

SHI 11.29.23 – Sorting Thru The Tea Leaves

November 29, 2023

SHI 12.13.23 – 2024 Predictions!

December 14, 2023

The ‘Holiday Season’ is upon us.

And pricey steakhouse reservation demand is showing it’s strength.

“

Steak and Christmas. A rare combo.”

“Steak and Christmas. A rare combo.”

Yeah that was a poor attempt at a pun. 🙂

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding … FED rate increases notwithstanding! At the end of Q2, 2023, in ‘current-dollar‘ terms, US annual economic output rose to an annualized rate of $26.84 trillion. After enduring the fastest FED rate hike in over 40 years, America’s current-dollar GDP still increased at an annualized rate of 4.7% during the second quarter of 2023. Even the ‘real’ GDP growth rate was strong … clocking in at the annual rate of 2.4% during Q2. No wonder the FED is concerned.

The world’s annual GDP first grew to over $100 trillion in 2022. According to the IMF, in June of this year, current-dollar global GDP eclipsed $105 trillion! IMF forecasts call for global GDP to reach almost $135 trillion by 2028 — an increase of more than 28% in just 5 years.

America’s GDP remains around 25% of all global GDP. Collectively, the US, the European Common Market, and China generate about 70% of the global economic output. These are the 3 big, global players. They bear close scrutiny.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

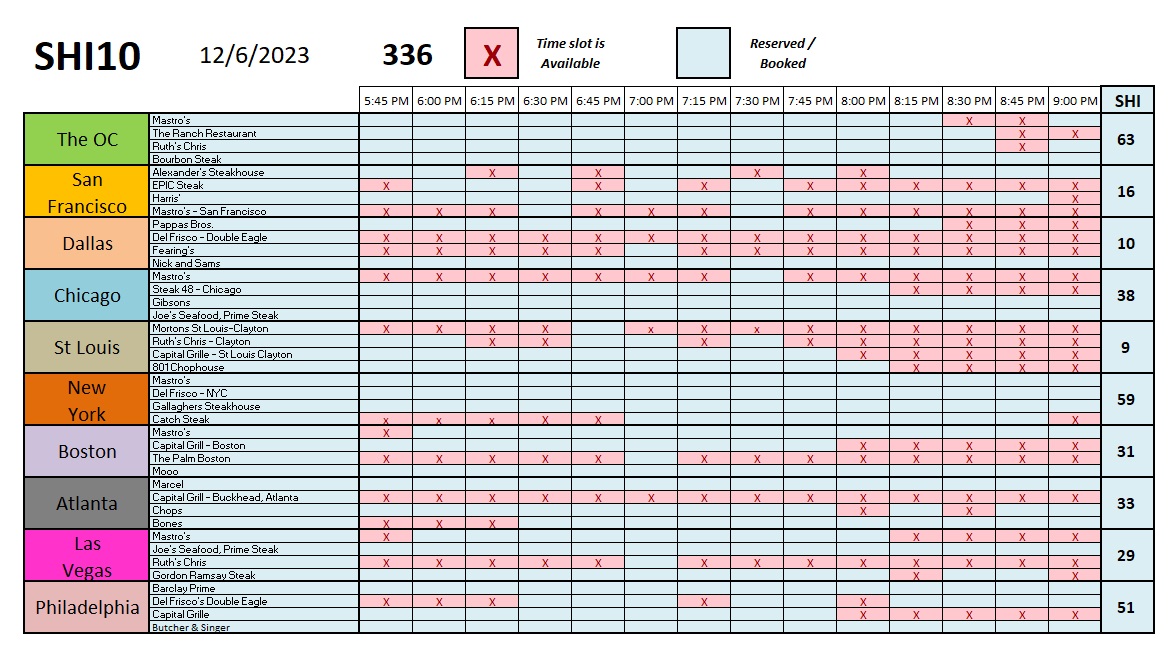

Not much new this week … economically speaking. Yeah, sure the FED keeps rattling their sabres; GDP ‘nowcasts’ are trending down; employment indicators reflect increased weakness; etc, but these trends are all expected and pretty well baked in previous blogs. What isn’t fully baked is this weeks SHI10 reading. Check out this move:

We haven’t seen a 336 since May — about 6 months ago. But don’t get too excited. The SHI spike simply reflects seasonality. Every year, around this time, the SHI10 trends up and typically remains high thru New Years Eve. The slowing GDP forecasts and hiring slowdowns tell the opposite, and more ominous, story. This Friday, the next installment of the ‘non-farm payroll’ numbers come out. I’ll be watching … and I’ll discuss the GDP trends, labor, and other related trends in detail next week.

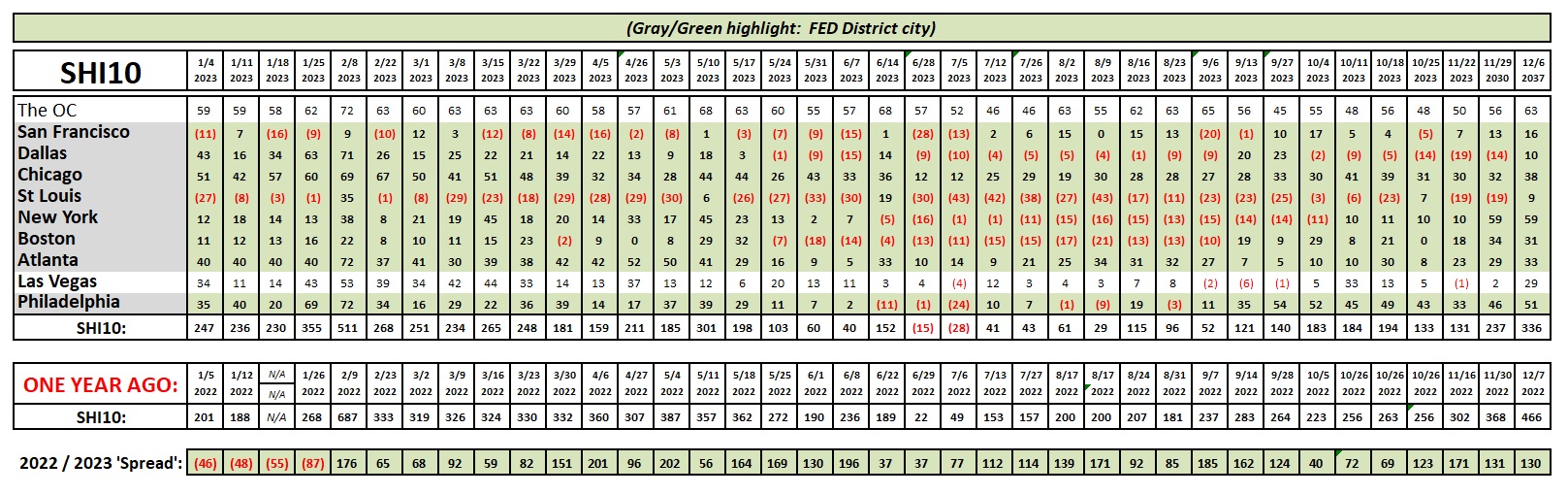

Sizzling steaks and Jingle Bells. A perfect pair. Here’s the longer-term trend report:

The ‘spread’ tells the story: Even though the SHI10 is up more than 200 points in 2 weeks, the ‘spread’ of 2023 over 2022 remains fairly flat.

Happy Holidays all!

<:> Terry Liebman