It’s time.

It’s time for my 2024 financial and economic forecasts! Yes!

But first, two housekeeping items. This is my final blog of 2023. Yep. It’s true. No, I’m not angry at Bing (you’ll understand below). But it’s time to enjoy the holidays. Second, this is a L O N G one, folks, so maybe those of you who need a little ‘Steak House Index’ once a week — I know, for some of you it’s like crack — you can read a bit today, a bit in a week, etc. You know, make it last. Like leftovers. Who doesn’t love eating half their Mastros Porterhouse on top of a beautiful salad several days later, right? Just like that.

“

Woo Hoo! He’s predicting the future!”

I haven’t done this since the end of 2020 … when the world was a very, very different place.

Are you curious about my comments from December of 2020? Take a look:

SHI: 12/23/2020: Predictions for 2021

Less than 1 year after the Covid Pandemic began, almost every aspect of our life was touched by Covid, in some fashion. By the time Covid receded from the headlines, nothing was the same. A hurricane, tornado, typhoon came together and hit us all simultaneously and everywhere. No one was spared.

As 2021 unfolded, and many of our expensive eateries locked their doors, I decided predictions in the middle of that storm were impossible. And so after my 2020 forecasts, I put my crystal ball in the closet where it has been collecting dust.

But no longer! The crystal ball is out … dusted off … on my desk … and it’s time for predictions! What, pray tell, will 2024 bring? Let me tell you …

Welcome to this week’s Steak House Index update.

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding … FED rate increases notwithstanding! At the end of Q2, 2023, in ‘current-dollar‘ terms, US annual economic output rose to an annualized rate of $26.84 trillion. After enduring the fastest FED rate hike in over 40 years, America’s current-dollar GDP still increased at an annualized rate of 4.7% during the second quarter of 2023. Even the ‘real’ GDP growth rate was strong … clocking in at the annual rate of 2.4% during Q2. No wonder the FED is concerned.

The world’s annual GDP first grew to over $100 trillion in 2022. According to the IMF, in June of this year, current-dollar global GDP eclipsed $105 trillion! IMF forecasts call for global GDP to reach almost $135 trillion by 2028 — an increase of more than 28% in just 5 years.

America’s GDP remains around 25% of all global GDP. Collectively, the US, the European Common Market, and China generate about 70% of the global economic output. These are the 3 big, global players. They bear close scrutiny.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

2024. It’s right around the corner. And so it’s time for a brief look-back at 2023, and then I can offer up a few opinions on what we might experience in 2024, economically speaking. Ready to go?

‘Artificial Intelligence’ exploded on the scene in 2023. Most believe it’s a game changer. Others see it as an existential threat. Regardless of your opinion on AI’s impact on humanity, pretty much everyone agrees the future will be quite interesting.

So in that vein, I decided to bring AI into the conversation. I asked the AI engine on Microsoft’s ‘Bing’ this question:

How important is artificial intelligence to the world in 2024 and beyond?

It may not surprise you that the AI engine thinks very highly of itself, and its impact on society and the future world, with a few reasonable caveats:

Artificial intelligence (AI) is one of the most transformative technologies of our time. It has the potential to improve many aspects of human life, such as health, education, entertainment, and security. However, it also poses significant challenges and risks, such as ethical, social, legal, and economic implications.

One of the main areas where AI will have a positive impact is health care. AI can help diagnose diseases, recommend treatments, monitor patients, and assist in surgery. For example, Google’s DeepMind has developed an AI system that can detect eye diseases from retinal scans with high accuracy. IBM’s Watson can analyze medical records and provide personalized advice to doctors and patients. AI can also help in developing new drugs and vaccines, such as the ones for COVID-19.

Another area where AI will have a positive impact is education. AI can help personalize learning, provide feedback, and enhance engagement. For example, Coursera uses AI to create adaptive courses that match the learners’ needs and preferences. Duolingo uses AI to teach languages through gamified exercises and chatbots. AI can also help in creating immersive and interactive learning environments, such as virtual and augmented reality.

A third area where AI will have a positive impact is entertainment. AI can help create new forms of art, music, and storytelling. For example, OpenAI’s GPT-3 can generate realistic and creative texts on various topics and genres. AIVA can compose original music based on the user’s mood and style. NVIDIA’s StyleGAN can generate realistic and diverse images of faces, animals, and landscapes.

However, AI also has some negative impacts that need to be addressed. One of the main challenges is ensuring the ethical and responsible use of AI. AI can have biases, errors, and unintended consequences that can harm people’s rights, dignity, and well-being. For example, facial recognition systems can be inaccurate and discriminatory, especially for people of color and women. Autonomous weapons can cause civilian casualties and escalate conflicts. Social media algorithms can manipulate people’s opinions and emotions.

Another challenge is ensuring the social and economic inclusion of people affected by AI. AI can create new opportunities for innovation and growth, but it can also disrupt existing industries and jobs. For example, self-driving cars can reduce traffic accidents and emissions, but they can also displace millions of drivers. Chatbots can improve customer service and satisfaction, but they can also replace human workers. AI can also widen the gap between the rich and the poor, both within and across countries.

Therefore, it is crucial to develop a global governance framework for AI that can balance the benefits and risks of AI for humanity. This framework should include common principles, standards, and regulations that can ensure the ethical, safe, and fair use of AI. It should also involve the participation of all stakeholders, such as governments, businesses, civil society, academia, and users. Moreover, it should promote the education and empowerment of people to adapt to the changes brought by AI.

In conclusion, AI will have a significant impact on the world in 2024, both positive and negative. It will improve many aspects of human life, but it will also pose many challenges and risks. Therefore, it is important to develop a global governance framework for AI that can ensure the ethical, safe, and fair use of AI for humanity.

Yes, clearly, Bing is very, very impressed with itself! And, seemingly, quite self aware.

The tech experts over at Stanford University generally seem to agree.

“Have we reached peak AI? No, say several Stanford scholars. Expect bigger and multimodal models, exciting new capabilities, and more conversations around how we want to use and regulate this technology.”

Interesting. Their expert ‘human’ opinions on the impact of AI in 2024 can be viewed here (right click, open a new tab):

https://hai.stanford.edu/news/what-expect-ai-2024

This idea came to me in a flash: Since I am a human, possessing only human intelligence, and since all humans crave praise, validation and admiration, I decided I’d ask that same AI engine what it thought about the Steak House Index! I was quite certain it would love my blog as much as you, my loyal readers, do!

I asked ‘Bing’ to read the blogs on my site and share its thoughts about my methodology and accuracy, and anything else it would like to share. Bing’s comment: “Sorry, dude, but I can only read something that’s open in one of my tabs.” OK, the “dude” thing is an human exaggeration, but the rest of the message is essentially accurate. So I thought “OK” and opened the blog post below in a new tab …

SHI 11.29.23 – Sorting Thru The Tea Leaves

… and I edited my request to ask Bing to read the opened post and share an opinion. Here is the Bing AI response:

The blog post is about the US economy and the Steak House Index, which tracks the reservation demand at expensive restaurants in 10 cities. The author claims that the US economy is slowing down, but not heading for a recession, based on the latest Beige Book and GDP reports. Here are some of my opinions on the blog post’s accuracy:

- The blog post uses current-dollar GDP as a measure of economic growth, which does not account for inflation or price changes. A more accurate measure would be real GDP, which adjusts for the changes in the value of money over time. Real GDP grew by 5.2% in Q3, which is still impressive, but not as staggering as 8.9%.

- The blog post relies on the Steak House Index as a proxy for consumer spending, which is a major component of GDP. However, this index may not capture the full picture of consumer behavior, as it only reflects the demand for expensive dining, which may be influenced by factors other than income, such as preferences, tastes, habits, or expectations. A more comprehensive indicator of consumer spending would include other categories of goods and services, such as retail sales, durable goods, or personal consumption expenditures.

- The blog post compares the economic performance of different cities based on the Steak House Index, but does not provide any explanation or analysis for the divergent trends. For example, why did Dallas and Las Vegas see a decline in reservation demand, while Philadelphia and Orange County saw an increase? What are the underlying factors that drive the differences in consumer spending across regions? The blog post could benefit from more context and evidence to support its claims.

Apparently Bing doesn’t love my blog. This notwithstanding, I was impressed with the AI assessment. The Bing AI engine definitely understands the essential nature and objective of the SHI. That’s very cool. Sure, like most “economic experts,” it prefers the real GDP metric to my favored ‘current dollar’ number, but that’s to be expected. And by either metric, I’m sure Bing would agree, the 5.2% growth rate in Q3 WAS staggering. The following two bullet points are also on point. Yes, the Steak House Index does not capture the full picture of consumer behavior. I agree. It wasn’t designed for that purpose. As you know, the SHI it simply intended to be an anecdotal barometer for this very large portion of the entire American economy. So Bing’s criticism is accurate and on point.

The “he didn’t provide any explanation for divergent trends” thing? Right, I didn’t. Because I don’t have one. Any explanation would be pure speculation on my part. As you know, we use 40 different expensive steak houses across the entire US in an attempt to diversify the reservation demand response across geography and a large sample. But I have no insight as to why we have seen a “Demand Decline in Dallas” except for the fact that all those capitalized words start with a “D”. That’s statistically meaningful, right Bing? Do you agree, Mr. Bing?

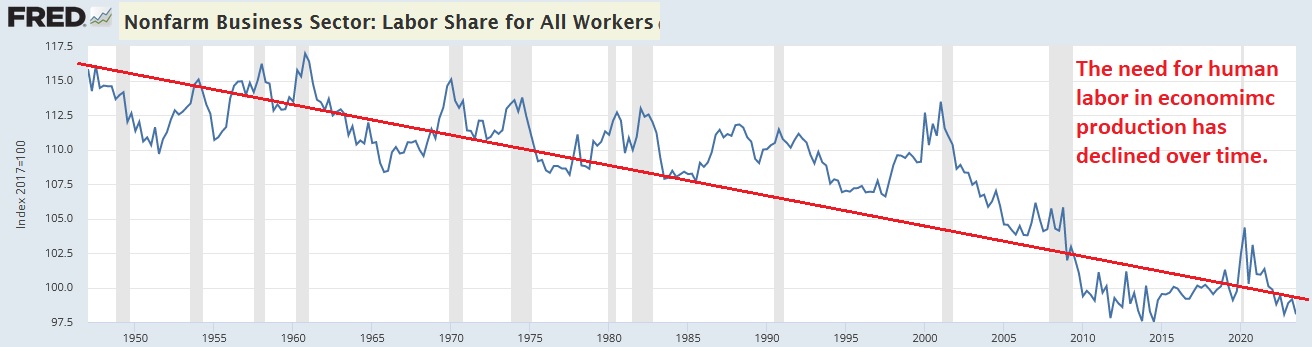

I jest. But I’m 100% serious when I say I agree that AI will change the world. During 2024 I expect the use of AI to explode in ways I suspect most of us are unable to predict. But I will make this prediction: As the use of AI increases, ultimately expanding at an arithmetic rate, the US economy will need fewer humans to generate one additional dollar of GDP.

No, I’m not suggesting there will be less humans working. At last count, the US had about 168 million folks in the labor force — up about 5 million from just before the pandemic hit in 2020. I am not predicting that 168 million will shrink. I’m predicting the trend illustrated by this graph will continue:

If you seek a deeper explanation, open this NBER link in another tab (right click, open in new tab). You’ll recall that ‘NBER‘ is the acronym for the National Bureau of Economic Research, a great economic data source:

https://www.nber.org/system/files/working_papers/w29165/w29165.pdf

Here’s the abstract, for those less inclined to take the deep dive:

“A vast literature seeks to measure and explain the apparent decline in the labor share in national income that has occurred in recent times in the United States and elsewhere. The culprits include technological change, increased globalization and the rise of China, the enhanced exercise of market power by large firms in concentrated product markets, the decline in unionization rates and the erosion in the bargaining power of workers in labor markets, and the changing composition of the workforce due to a slowdown in population growth and a rise in educational attainment.”

Summarizing, if the adoption of AI in 2024 and beyond continues this trend, yet the number of employed humans continues to rise, the only logical conclusion is that (1) American productivity will increase and (2) GDP growth will accelerate meaningfully as AI fully integrates into the US economy. To repeat, if we assume that the labor force will not shrink — and, in fact, is more likely to grow from the current 168 million folks in the labor force — while, at the same time, labor expense as a percentage of GDP continues to shrink, then our GDP growth must accelerate significantly. In fact, to achieve this outcome, it must accelerate far above the current 2.0% annual trend generally forcasted by the FED and other experts.

Interest Rates

The FED released their most recent interest rate guidance on Wednesday at 11 AM (pacific.) Essentially, reading between the lines of FED-speak, they told the world they are done raising rates. In fact, most FOMC members are expecting rates to decline in 2024.

Of course, they left the door open to raise rates further, saying they will raise rates if future data suggests excessive inflation has returned. Don’t worry. It won’t. Inflation is trending downward. In 2024, our CPI rates will fall into the 2s once again. Fear not. Price stability has been restored.

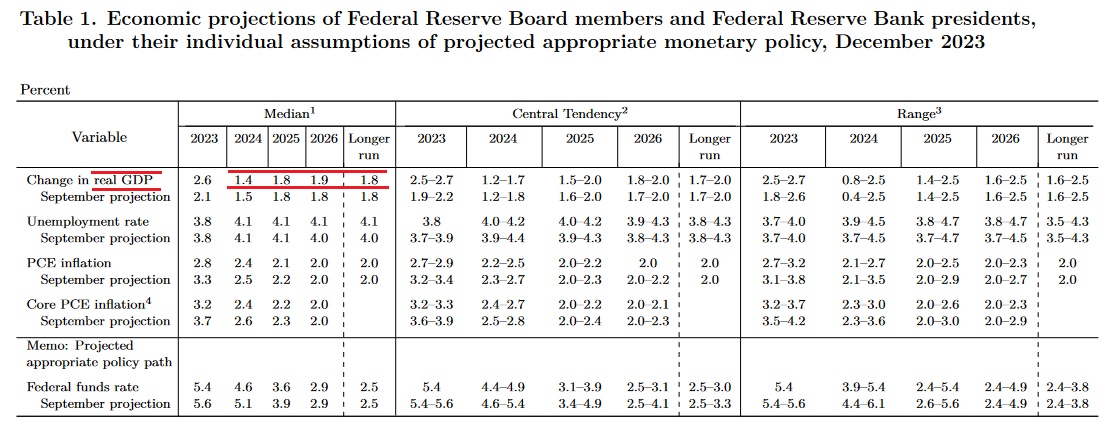

What you might want to fear, however, is the FEDs forecast in chart below, around future GDP growth. See my red lines? The FED does not expect real GDP growth to reach their 2% longer-run target until … well … never. Their “Longer Run” forecast — essentially, beginning in 2027 — is a 1.80% annual real GDP growth rate. Which is really bad news for all those folks whose job may have been, or may well be, displaced by the implementation of AI. Remember, if AI “takes away” existing jobs, but creates new ones, thereby permitting the labor force to continue to absorb labor force growth, we need an above-trend GDP growth rate. Nope, said the FED early Wednesday. Not gonna happen.

I both hope, and believe, they are wrong. I expect 2024 GDP growth in excess of the FED forecast.

Next, check out the FED forecast for the trajectory for the “Federal funds rate,” currently around 5.5%. By the end of 2024, the ‘median’ forecast is for a 4.6% rate … by the end of 2025, down to 3.6% … and the end of 2026 — 2.9%. Wow. Those are some serious declines. What happened to rates will be “higher for longer?” POOF! Gone. In the FED‘s opinion.

Not mine. My take is those forecasts are aggressive. The only reason the FED will pull rates down that far, that fast, would be because both (1) inflation is at, or below, its 2% long-range target, and (2) the US economy is weak or shrinking. While I expect (1) might happen, I do not expect (2) to happen anytime soon. It is likely the FED will lower the FED funds rate by 100 basis points during 2024 — to the 4.5% range — but I believe short term rate is likely to remain there for an extended period of time. How extended you ask? It’s hard to forecast today, with any certainty. Because the financial markets must now rediscover what is known as the “neutral interest rate.” Yes, the neutral interest rate. What, pray tell, is that?

Essentially, it is precisely what it sounds like. Economists would define it as “the short term rate prevalent when the labor force is at full-employment and inflation stable.” But a better way to think about this neutral rate is this: What is the rate of interest that neither stimulates nor restricts economic growth? That is the neutral rate or interest. The concept may seem simple, when stated that way, but in practice the neutral rate is difficult to find. Probably because it moves higher and lower based on an extensive list of variables. However, extrapolating from nonsensical endpoints we can get close; and if not precise, at least within a range.

For example, let’s ask this question: Does a zero percent interest rate stimulate the economy? No brainer, right? Of course it does. OK, well then, how about a 12% interest rate? No. That rate is restrictive and will cause GDP growth to decline. Thus, we know the neutral rates is somewhere between 0% and 12%. From here, move up from 0% and down from 12% … when you get to a rate that you feel, at this moment, is neither stimulative or restrictive, that’s today’s neutral rate.

Interestingly, the 5.2% real GDP growth rate in Q3 — in spite of a ‘5%+’ Federal Funds and 10-year treasury rate — suggests the US economy can handle high rates right now. This fact suggests that a 5% 10-year treasury is not restrictive. And that a 5.5% FED funds rate is not restrictive. However, logic suggests that interpretation is wrong. Logic suggests that those rates, over time, will be corrosive. Note: This is my opinion … not fact. But I feel I’m right.

The American economy will not continue to clock 5%+ GDP growth rates in future quarters. GDP growth in 2023 rode the wave of the massive post-Covid stimulus packages. I’m hoping the $5 trillion monetary and fiscal “boost” was a one-time thing. Sure, the 2024 economy will surely be bolstered by the Chips and Infrastructure acts, but the effect will be muted when compared to the 2023 GDP performance.

So, therefore, I feel a 5% rate — both short- and long-term — are too high to be neutral. Does 4% work? I don’t think so. How about 3%? Closer. I suspect the low-end of the FEDs 2025 forecast of 3.1% is probably very close. But rates are likely locked at a higher level because of the labor markets. Data suggests we remain in a world where there is more demand for labor than available laborers. Thus, during 2024, don’t expect more than 100 basis point reduction in the FED funds rate. My prediction: We will end 2024 with a FED funds rate at or near 4.25%.

Will the yield curve remain inverted during 2024? Yes, I expect it to remain slightly inverted as the economy continues to find its footing in the post-pandemic world. I believe the 10-year Treasury will end 2024 closer to 4.25%. Why so high you ask? Because for now, the economy has proven it can tolerate such a high rate … and the Federal government still has a lot of money to spend from the ‘Chips’ and ‘Infrastructure’ bills. But we will watch quarterly GDP reports carefully … and time will tell.

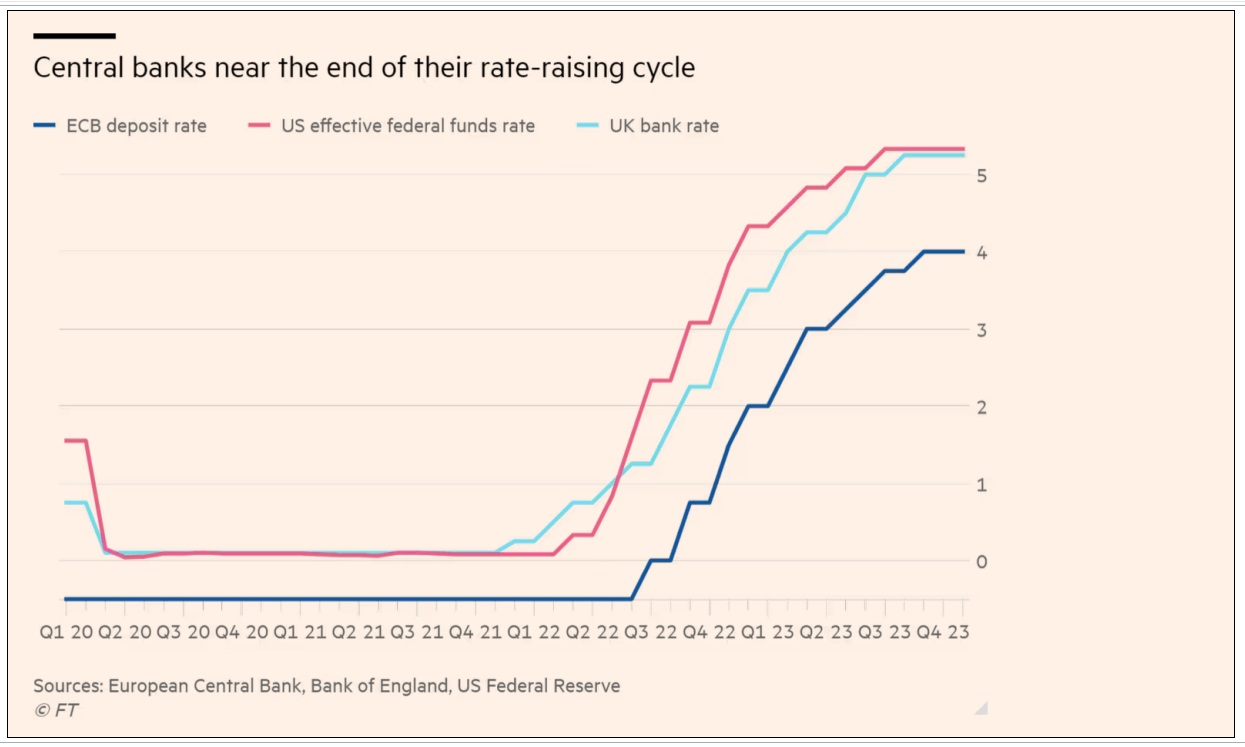

One final note on the interest rate topic. Earlier today, Thursday the 14th, the central banks in Europe announced they, too, just like the FED, will hold rates steady now. I expected this outcome from both the BOE and the ECB. Clearly the leaders of the major central banks are passing notes in the halls at the Bank for International Settlements over in Basil, Switzerland. The movement correlation between these three is clear and obvious:

Today, I declare that the rate hike cycle that began in March of 2022 is over. Worldwide. The next direction for rates? Down.

US Labor Market:

This market has baffled experts for years now. But most experts felt unemployment would not be tamed without significant pain in the labor markets.

On July 7th of 2022 — shortly after the FED began their rate hikes — the esteemed Larry Summers commented when speaking at the London School of Economics:

“We need five years of unemployment above 5 percent to contain inflation—in other words, we need two years of 7.5 percent unemployment or five years of 6 percent unemployment or one year of 10 percent unemployment.”

I felt the comment was absurd when made. Two years of 7.5% unemployment? That was 4% higher than the then current rate of 3.5%. The math tells us Dr. Summers believed more than 6 million people must lost their jobs in order to get the inflation rate under control. Fortunately, he was dead wrong. The unemployment rate today is only marginally higher, at 3.7% today, and inflation is definitely under control. In fact, the US how has more than 168 million working. That’s up more than 5 million from the last pre-pandemic measure. And the inflation rate continues to fall steadily.

Where will the labor markets go from here?

I suspect they will remain fairly robust. Why? Notwithstanding the fact that ‘labor cost’ as a percentage of GDP continues to slowly decline (as we saw in the graphic above), labor remains an important component of economic production and growth. Good news, right? 🙂

Ultimately, in a capitalist economy like ours, the demand for labor will always be highly correlated with corporate profitability. Corporate profits, after tax, drive that company’s stock price. The higher the profits, the higher the price. And publicly traded companies want to have a high, and rising, stock price. In the long run, the direction of the S&P 500 and the DJIA follow the direction of corporate profitability:

In Q3 of 2023, the annualized rate for ‘corporate profits’ was over $3 trillion. On the eve of the pandemic, that number was about $2.1 trillion. Yes, corporate profits for publicly traded companies are up over 30% from the same measure pre-pandemic. Stock prices are up. CEOs are happy. And during this same period, more than 5 million new workers joined the labor force.

As long as corporate profits remain stable or grow, I expect the labor markets to follow. And I believe this will be the case in 2024. GDP will grow, corporate profits will grow, and the unemployment rate will remain low. I forecast the unemployment rate will remain at 3.9% or lower during 2024.

And remember: Employed Americans are Americans that buy more stuff! As our GDP is about 70% correlated with Americans buying stuff, this is a good thing.

GDP:

The GDP growth rate will decline in 2024. In fact, the GDP growth rate will begin that decline in Q4 of 2023.

This is not a bad thing. The US economy cannot sustain the 8.9% nominal growth rate achieved in Q3. It’s simply too fast. However, it did get us to a current-dollar GDP level of $27.6 trillion, on an annualized basis, and that’s quite good! Remember: GDP peaked, pre-pandemic, at $21.9 trillion at the end of 2019. In less than 4 years, the ‘run rate’ for America’s economy has increased 26%.

By any metric, that’s a good thing.

But the party has to end. Someone spiked the punch bowl at the office party, your boss was dancing on the dining room table without a shirt, but, unfortunately the crazy-loud music inspired your neighbors to call the cops. They are here, now, at the front door. And they are about to take away the punch bowl. The party’s over. Yes, the “spike” to the punch bowl in this analogy is the $5 trillion of stimulus; and the “cops” are those buzz-kill economists over at the FED and they have done all they can to shut it down.

So the growth rate will slow from the blistering 8.9% (nominal) rate to something more sedate … but how low will it go? And is a recession in the cards?

No. No recession in 2024. I know plenty of experts are forecasting a recession in the 2nd half of the year, but I don’t see it. We are at full employment, the aggregate wealth of Americans has never been higher, and corporate profits are near all time highs. And all this was achieved during a massive FED tightening cycle.

Rates are now stable or falling. This will provide a tailwind for the economy and consumer spending. However, the lag effect of the prior rate hikes has not yet fully embraced the entire economy. That will happen during 2024. And it will dampen the GDP growth rate as a result.

I predict we will end 2024 with nominal GDP growth of 4.8% and real GDP growth of 2.2%. 🙂

US Inflation:

If during 2024 the real GDP growth rate is 2.2%, and nominal is 4.8%. that means I’m forecasting an inflation rate of 2.6% during 2024. This forecast will be assisted greatly by what’s called the CPI “base effect,” as the very high January and February (2022) readings ‘roll out’ of the annual calculation. And I expect the very large “housing” component in the CPI to decline meaningfully in the near future, possibly pushing the overall inflation even lower than I expect. The only wild card is the impact of ‘re-shoring’ and ‘close-shoring’ as globalization and supply chains shift post-pandemic. Globalization is inherently deflationary. The opposite, which we’re now experiencing, is inflationary.

We’ll see. But by Q2 of 2024, I expect to see the CPI somewhere in the mid-2s.

Real Estate:

What a mixed bag. Falling interest rates will add a tailwind to home price gains. Home values will generally rise in 2024.

I’m often asked about commercial real estate. What will happen in this segment? It depends. Industrial/logistic space should continue to claim top prize for value and stability in 2024; hospitality (hotels) should continue to do quite well, depending on location; multi-family performance will vary from exceptionally good to exceptionally bad, again, depending on location. Location will also impact the retail space, but I expect retail to generally do well in 2024. And I expect 2024 to be an “improving” year for office buildings — but that’s not saying much as things in the office building space couldn’t get much worse.

Recent inflation spikes in building materials and construction labor shortages have pushed replacement cost thru the roof. This is a reasonable tailwind for the sector. However, lower construction rates only help over the longer term and won’t offer much solace to any segment during 2024.

Lower interest rates may help some commercial property owners refinance debts coming due. But lower valuations will hinder that process at the same time. By the end of the year, there will be some distressed debt-force sales, but I do not anticipate a wave of defaults anywhere near as large as many experts are suggesting. There will be defaults, but they will be fewer than expected, and widely disbursed across the country.

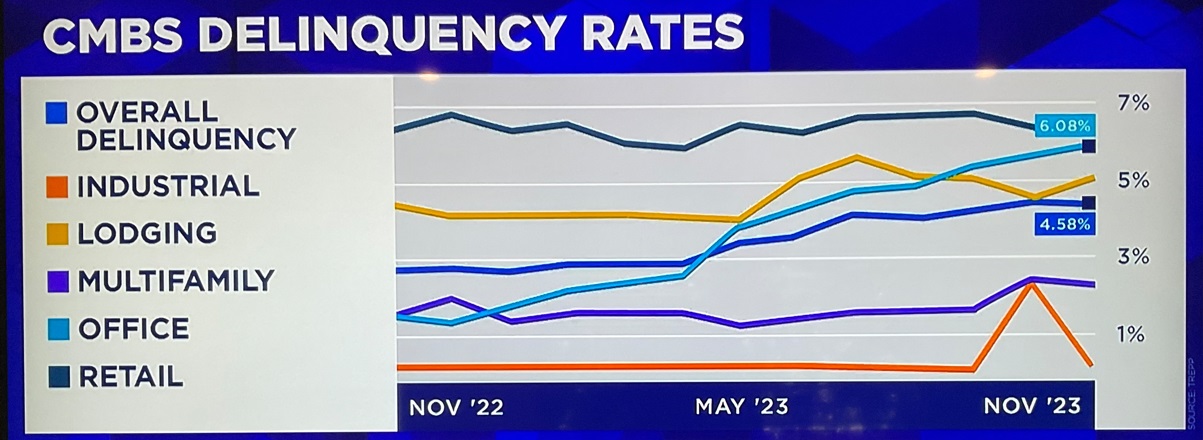

Ironically, as I was writing this section of the blog, the ‘talking heads’ on CNBC were talking about the commercial real estate sector. The put up this graph:

CMBS is an acronym for ‘Commercial Mortgage-Backed Security,’ a common source for much of the commercial lending across the US. We see that ‘delinquency’ or default rates on loans in the industrial segment are super low. But even a 6.08% delinquency rate on the office CMBS segment, is not indicative of a wave of defaults. Yes we will see defaults. But there is no massive wave ready to crash, nor will these defaults present any kind of systemic risk.

By now, you are probably as tired of reading my blather as I am of typing. 🙂

Let’s head to the steakhouses one final time in 2023.

Well, this week is almost identical to last week’s reading. No, Mr. Bing, I cannot explain that either. 🙂

Here’s the longer term trend.

What’s left to say but thank you for tuning in and, of course,

Happy Holidays all!

See you in 2024!

<:> Terry Liebman