SHI: 12/23/2020: Predictions for 2021

SHI 12.16.20: Piles and Piles of Cash

December 17, 2020

SHI 12.31.2020: The Death of Spontaneity

December 28, 2020

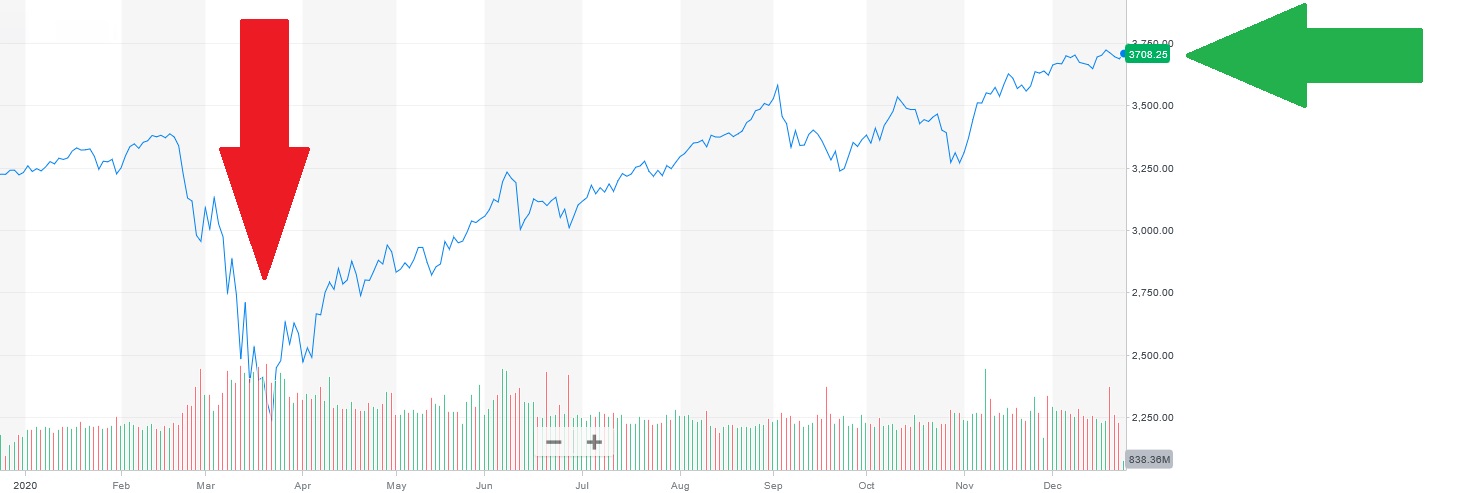

It’s a good thing I didn’t make 2020 predictions at the end of 2019. 🙂

I mean, who could have predicted these two moves in the S&P 500 index? Clearly no one.

No, there was nothing remotely predictable about 2020 one year ago. But 2021? Knowing what we know now, I have some thoughts.

“

Forecasting 2021 events? Sure. Why not.“

“

Forecasting 2021 events? Sure. Why not.“

So, in my final post in 2020, let me wade in.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Before COVID-19, the world’s annual GDP was collectively about $85 trillion. Then it shrank … then bounced back! We can thank global fiscal and monetary policy for the bounce. According the the Q3, 2020 ‘preliminary’ numbers, annual US GDP is back UP to about $21.1 trillion. And still, together, the U.S., the EU and China continue to generate about 70% of the global economic output.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

2021 GDP: Let’s start with the ‘big boy’ … GDP growth. We will finish 2021 with a ‘real’ GDP growth rate of greater than 6%.

CPI: The consumer price index will finish 2021 at less than 2.2% … and the FEDs more conservative PCE will finish the year at about 1.5%.

Asset Inflation: This is where I believe you’ll see the inflationary impact of the staggering money supply growth. After 15% gains in 2020, home values will increase another 12% in 2021. Commercial real estate is more of a mixed bag. For example, a recent Wall Street Journal article discussed the most transparent metric for commercial properties: Publicly traded REITS. Here is what they found: ‘Retail’ property REITs – market values are down 42% YTD. Hotel REITS: down 50%. Office building REITS: down 36%. But the market value of Data Center REITS is up 23% in 2020 and ‘industrial’ property REITS are up about 9%. So in 2021, feel free to dabble in commercial property cautiously, but I predict the value of all commercial properties will be higher by the end of 2021 — with the sole exception being office buildings. They are in for a long slog.

10-year Treasury yield: Ahhh … the trillion dollar question. My prediction: The 10-year Treasury will trade flat all year long. It will not move much — either up or down — from its current level of about 0.95%.

Grab Bag: Here is a hodgepodge of other forecasts: By December of 2021, air travel capacity levels will exceed those from December of 2019. Broadway will return by Q4 … and the venues will be packed full. Consumer spending will explode, driving GDP growth to levels not seen in decades. Spurred on by almost zero interest rates, infrastructure investment will begin in earnest across the globe … gaining traction and pace as the year ends. AI and the IoT will also gain traction … as the move toward an automated world gains speed, and labor as a percentage of manufacturing cost will continue to fall. The price of gold will finish 2021 at more than $2,500 per oz. In 2021 will will say goodbye to the LIBOR index … and hello to SOFR.– the ‘Secured Overnight Funding Rate.’ LIBOR will be replaced by the end of the year. China will launch a digital currency in 2021: The ‘e-yuan.’ It will be the first major digital currency … but not the last.

Finally, here’s one I feel very strongly about: The ‘steakhouse index’ will return in 2021! That’s right … our ‘alternative economic metric’ will once again be front and center in 2021. The anticipation is downright palpable! 🙂

Happy Holidays!

- Terry Liebman