SHI 2.24.21: Our Rates are Rising!

SHI 2.17.21: Baskets Full of Data

February 17, 2021

SHI 3.3.21: Staying Positive in a Negative World

March 3, 2021

Is it time to panic?

No. Relax. Sure the US 10-year Treasury rate is higher than just weeks ago. Much higher. What’s this mean? Is rampant inflation is right around the corner?

No. Relax. The rate rise has a few causes — one of which is definitely a fear of inflation — but the rate rise is probably more closely aligned with the burgeoning supply of Treasury debt caused by the multi-trillion stimulus bills and the rising expectation for a rapidly growing US GDP as the vaccine gains traction across the country.

“

Remain calm. We’re good.“

“Remain calm. We’re good.“

“Reflation” is definitely happening. The prior stimulus injections have done their job. And we will likely see another $1.9 trillion (or thereabouts) of new money. Cumulatively, when finished, the US Covid-19 stimulus programs may exceed $5 trillion. Wow. $5 trillion. And that’s just here in the US. Across the globe, the total stimulus injection may eclipse $15 or 16 trillion — which is an amount equal to about 20% of the globe’s $85 trillion annual GDP. Staggering.

But while rates are up significantly here in the US, they are not in Europe or Asia. The 10-year German ‘bund’ remains at a negative 0.30%. How about Italy — arguably one of the weakest euro-zone economies? Their 10-year yield is only 0.69%. And in Japan? The most indebted “developed nation” on the planet? Their 10-year debt is close to zero, yielding only 0.123% — almost unchanged over the past 3 years.

So why are 10-year rates rising significantly here in the US?

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Before COVID-19, the world’s annual GDP was collectively about $85 trillion. Then it shrank … then bounced back! We can thank global fiscal and monetary policy for the bounce. According the the Q3, 2020 ‘preliminary’ numbers, annual US GDP is back UP to about $21.1 trillion. And still, together, the U.S., the EU and China continue to generate about 70% of the global economic output.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

So why are 10-year Treasury rates rising significantly here in the US?

The short answer, I believe, is the growing “supply” of new US Treasury debt. The supply is simply outstripping demand. It appears that there is more debt for sale than buyers willing to buy … at the present. Makes sense.

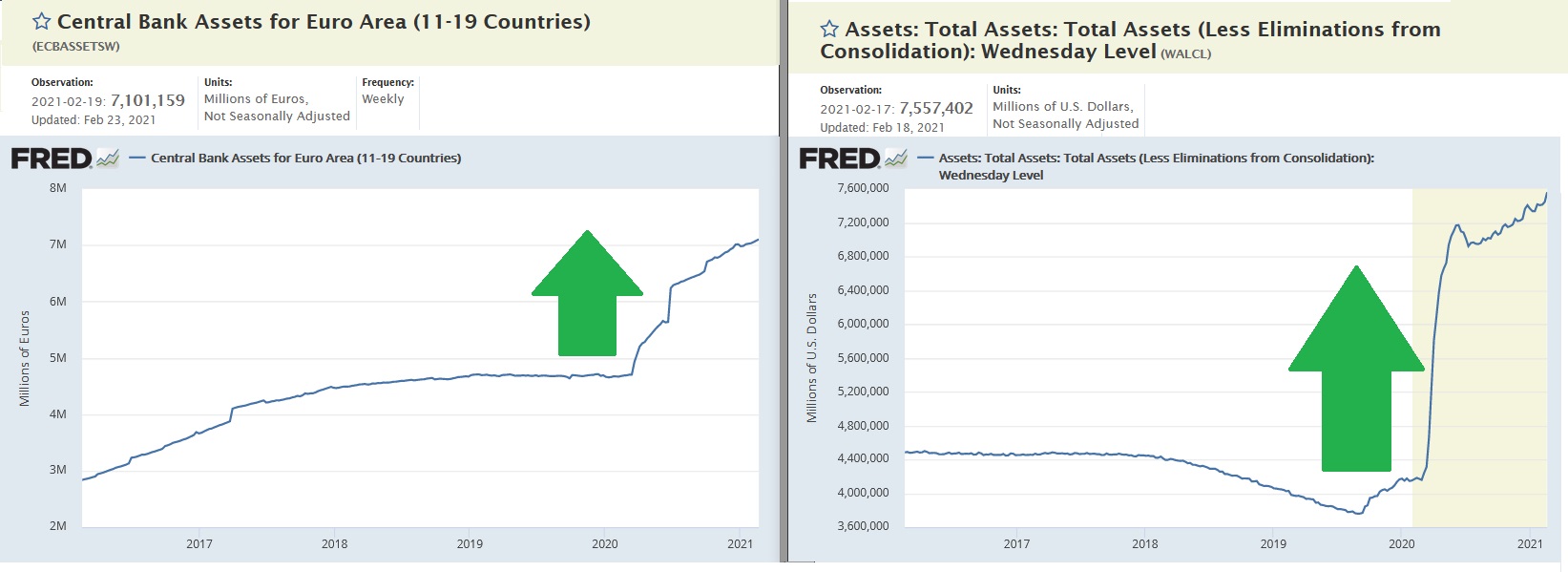

For example, consider what’s happening in Europe. Like here in the US, most European countries have unleashed massive Covid-19 stimulus programs. And like here in the US, they’ve floated massive amounts of debt to fund it. And just like the FED here in the US, the ECB has purchased much of the sovereign debt sold:

Both the ECB and the FED have “purchased” trillions in debt. In mid-March, 2020, the ECB had about 4.7 trillion euro on their balance sheet. Today, as we see above, the number has climbed to over 7.1 trillion euro. Convert that to US dollars, and we see the ECB owns about $8.5 trillion of European debt. The FED, on the other hand, only owns about $7.5 trillion. Only. 🙂

But unlike here in the US, ECB leaders have pledged to keep “financing conditions favorable” until the pandemic crisis is far in the rear view mirror. They have already begun jawboning to keep rates at or near zero in the Eurozone:

“Sovereign yields are particularly important. Accordingly, the ECB is closely monitoring the evolution of longer-term nominal bond yields.”

— Christine Lagarde, ECB President

European economists have said things like, “If euro-zone sovereign yields continue to move higher in coming weeks, it’ll leave the ECB no choice but to step up their purchases with the pandemic emergency purchase program to counter this undesirable tightening of monetary conditions.”

Here in the US, the FED has made no such commitments. Yet. Sure, Powell has been testifying over the past couple of days assuring us that Covid-inspired stimulus — due to it’s “one and done” nature — is not inherently inflationary. But he has made no similar comments about capping US treasury yields. Yet.

If yields continue to rise, I expect the FED will either (1) Increase their $120 billion monthly purchase — almost $1.5 trillion per year — of Treasury and MBS assets to a much higher level; or, (2) Create some form of structural “cap” on long-term rates.

It’s worth noting that Gita Gopinath, the Director of Research of the International Monetary Fund agrees with the FEDs inflation assessment. The IMF is not overly concerned:

“Several structural factors underlie this diminished relation between inflation and economic activity in many countries. One: Globalization that has limited inflation in traded goods and even some services. Second: Automation which, along with relative declines in the price of capital goods, has largely kept higher wages from being passed through to prices. Three: Expectations of inflation have remained broadly stable around the targets set by central banks, thanks to central banks’ independence and the credibility of their policies.”

— Gita Gopinath

I believe she is correct. Over the past few years, in this blog I’ve talked about the facts that the US economy is no longer constrained by our borders for goods, services and labor. Ours is now a global economy. And I’ve talked extensively about growing automation. My opinion remains that as the world “reflates” we will definitely continue these rigorous inflation debates, but we shouldn’t be overly concerned at the moment.

But the 50 basis point lift in the 10-year treasury yields is mildly concerning. But fear not. I suspect the FED will soon step in with counter measures. Yesterday and today, Powell testified to the House Financial Services Committee. There, he said:

“The economy is a long way from our employment and inflation goals.”

He assured the committee that the FED plans to continue to support the US economy with near-zero interest rates and large-scale asset purchases until “substantial further progress has been made,” a standard that Mr. Powell said “is likely to take some time” to achieve.

The FEDs dour comments notwithstanding, many US economists are expecting big things for our economy in 2021. Goldman Sachs has boosted their 2021 GDP growth forecast to 6.8%. Of course, their predictions, like others, are highly correlated with the speed of vaccine roll-out. So watch those rising vaccine numbers — they are very predictive for the reopening.

“We expect a surge in economic activity and hiring by the second half of 2021 following mass vaccinations, with the recovery particularly strong in the services sector,” said Leo Feler, a senior economist at the UCLA Anderson School of Management.

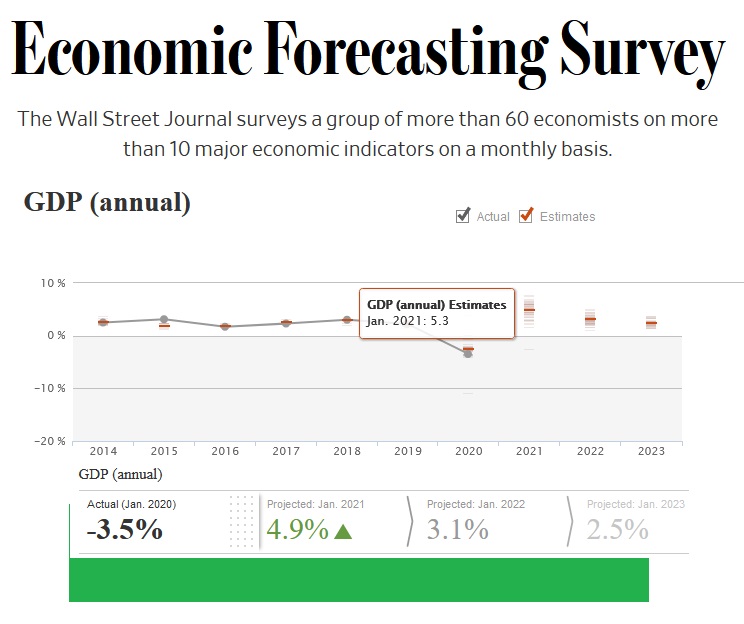

The Wall Street Journal recently asked more than 60 reputable economists for GDP predictions in the next few years. On the average, this group expects to see an average of 5.3% growth in 2021 and more than 3% growth in 2022.

I think they are low. I believe Goldman is closer. 🙂

A growing economy does put upward pressure on interest rates — but a vigilant FED will prevent excessive upward movement. Rates have been rising there’s no cause for alarm. They will peak and reverse soon enough. Once again, the FED has our back.

- Terry Liebman