SHI 3.3.21: Staying Positive in a Negative World

SHI 2.24.21: Our Rates are Rising!

February 24, 2021

SHI 3.10.21 – Spending $4.5 trillion

March 10, 2021

Insanity redux: Want a home loan? How does a -0-% interest rate sound?

That’s right. Zero. Zip. Nada. Zilch. Too outlandish to believe? Perhaps, but as we all know, these days truth tends to be stranger than fiction. 🙂

https://www.theceomagazine.com/business/finance/interest-rate-fixed-zero/

Nordea Bank Abp is already offering interest-free home loans. Two competitors have followed suit and the largest bank in Denmark — Danske — is seriously considering the same. Imagine that: In Denmark, money for home loans is free.

“

Free money in Denmark! “

“Free money in Denmark! “

If the interest rate is zero, then your borrowing cost is zero. So the money is free, right? How in the world can Nordea Bank stay in business lending money at zero percent? Great question. You may find the answer to be stranger than a zero percent home loan. 🙂

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Before COVID-19, the world’s annual GDP was collectively about $85 trillion. Then it shrank … then bounced back! We can thank global fiscal and monetary policy for the bounce. According the the Q3, 2020 ‘preliminary’ numbers, annual US GDP is back UP to about $21.1 trillion. And still, together, the U.S., the EU and China continue to generate about 70% of the global economic output.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

-0-% home loans. Crazy, right? Can Nordea stay in business lending money for free?

Yes, and here’s how they do it: For bank deposits exceeding about $41,000 — 250,000 danish krone — the bank charges the depositor a 0.75% annual rate on their money. That’s right: The depositor pays to put his or her money in the bank. Let me repeat: If you deposit $50,000 into Nordea, don’t expect Nordia to pay you any interest.

That’s not gonna happen.

No, not only does the bank pay you no interest, but you cannot deposit your money with the bank without cost. The bank charges you 3/4 of a percent to simply keep your money in the bank! By comparison, your mattress is looking pretty good! Consider this: one year later … that mythical $50K you deposited in the bank? Your account balance is now $49,625. What a great deal! Well, for the bank maybe. For you? Not so much.

For all of human history, banks and “lenders” have been profitable charging their borrowers interest. Not today. Not in Denmark. And since the bank charges no interest, they must charge their depositors a “fee” for “safely storing” their cash. And that’s what’s happening in Denmark today.

And in Germany, too. Germans are prolific savers. In fact, 30% of all savings in the eurozone are from German citizens — over $3 trillion in total.

Germany’s biggest lenders, Deutsche Bank and Commerzbank, have required new customers since 2020 to pay a 0.5% annual rate to keep large sums of money with them. The banks say they can no longer absorb the negative interest rates the European Central Bank charges them. According to price-comparison portal Verivox, 237 German banks now charge “negative interest rates” to private customers, up from 57 before the pandemic hit in March of last year. Charges range between 0.4% and 0.6% for deposits beginning anywhere from €25,000 to €100,000. The charge for bank deposits is higher in Switzerland. There, you will pay the same as in Denmark: 0.75% per year.

Insanity redux. The world of finance is upside down.

The ‘official’ interest rate in Denmark is 0.05%. In Switzerland? Negative <0.75%>. Denmark and Switzerland have lived with negative interest rates since January of 2015. The Swiss 10-year bond currently yields a negative <.269%>. Denmark’s is a negative <.17%>. And, at least for now, these ultra-low and negative rates are here to stay.

Bloomberg recently completed their quarterly review of global monetary policies, covering 90% of the world’s economies and central banks, and concluded that no major western central bank plans to hike interest rates in 2021. China, India, Russia and Mexico have indicated they plan to cut rates further, and of all central banks across the globe, only Argentina and Nigeria’s plan to raise rates this year:

Most seem to be following moves made by the FED and Chairman Powell:

“We are committed to using our full range of tools to support the U.S. economy to achieve our goals,” Powell said in December after the Fed strengthened its bond-buying guidance. “We will continue to use our tools to support the economy for as long as it takes until the job is well and truly done. No one should doubt that.”

Ditto for the euro-zone and Asian central banks.

Then why are US interest rates so much higher than our counterparts around the globe?

Why are US rates positive — and rising —

when the rest of the developed world sports negative rates?

First, it’s important to say that not all US Treasury rates are rising. Yes, the “long end” of the curve is rising: The 10-year Treasury yielded .93% on January 4th. Today is yields closer to 1.5%. In fact, yields have lifted for every Treasury instrument longer than 1-year … while yields have declined on the 1-mo, 2-mo, 3-mo, 6-mo, and 1-year treasuries. In other words, the “yield curve” is steepening.

And as I mentioned in last week’s blog, at present, the US Treasury has a “supply” problem. And it’s about to get worse … assuming the $1.9 trillion stimulus bill passes. From a Bloomberg article earlier this morning:

“Treasuries resumed declines on Wednesday, sending yields higher across the curve. That follows a disastrous sale of seven-year notes in the U.S. last week, which set the tone for tepid demand for subsequent sovereign bond offerings from Indonesia to Japan and Germany, and prompted other nations to scrap offerings. The push for higher rates comes as central bank policy makers attempt to ease investors’ discomfort at the pace of the recent jump in yields.”

“I am paying close attention to market developments. Some of those moves last week and the speed of the moves caught my eye. I would be concerned if I saw disorderly conditions or persistent tightening and financial conditions that could slow progress towards our goal.”

The FED, it would appear, is watching. Closely. A run-away rise in long-term yields would derail the FEDs monetary plan. As Ms. Brainard suggests above, they will step in — if needed — to prevent “disorderly conditions” or “persistent tightening.” Translating this into easy-to-grasp english, they must increase the amounts of bonds they are purchasing. FED assets on their balance sheet are about to grow substantially.

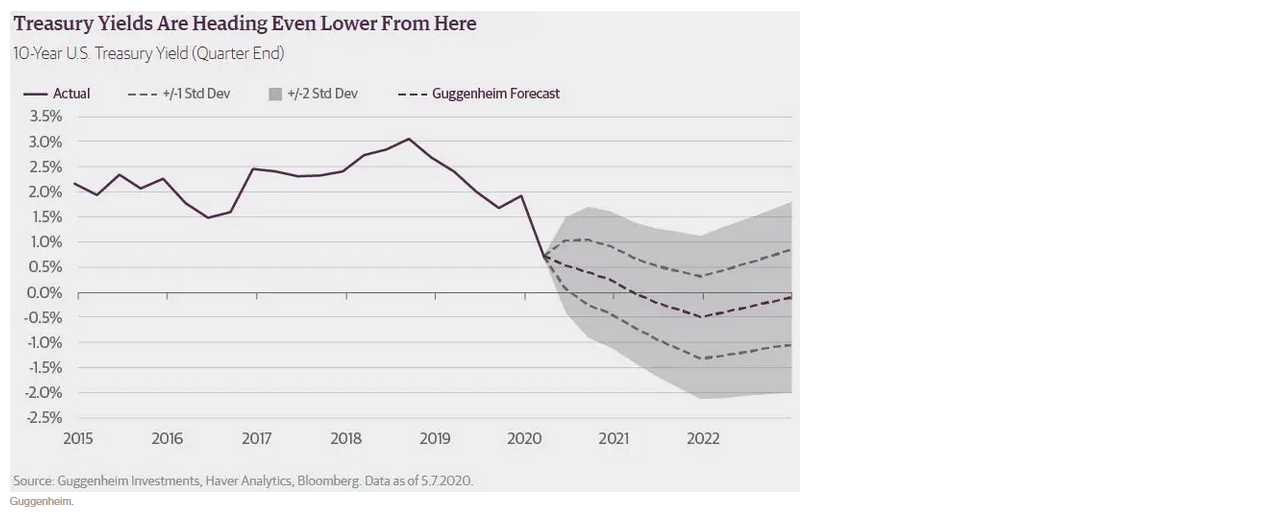

Scott Minerd is the CIO at Guggenheim, where he manages over $250 billion in assets. Minerd is in my camp: He believes the 10-year US Treasury rate will fall. But he’s even more “bearish” than I am: He expects the 10-year to tumble to 25 basis points … and then go negative in 2022.

“Over time, as stimulus payments and tax refunds are distributed and more money looks to be put to work, investors will extend maturities on their bond portfolios in a ‘reach for yield,'” Minerd has been reported to have said. Per Minerd, two-year Treasury note yields could go to 1 basis point or lower and 5-year Treasury notes could easily reach 10 basis points.

“These levels would put downward pressure on 10-year Treasury rates, likely rendering the current yield unsustainable,” said Minerd. Guggenheim models the 10-year yield at -0.5% in January 2022, but that number is bounded by a two-standard deviation range of a high of 1 percent and a low of -2.0 percent:

Perhaps I find Minerd’s comments comforting, satisfying my confirmation bias, because just about everyone else seems to disagree with us. And, no, I’m not of the opinion that the US 10-year Treasury is going negative, but comparative rates from other developed nations around the globe tell me long-term US Treasury rates must fall from current levels.

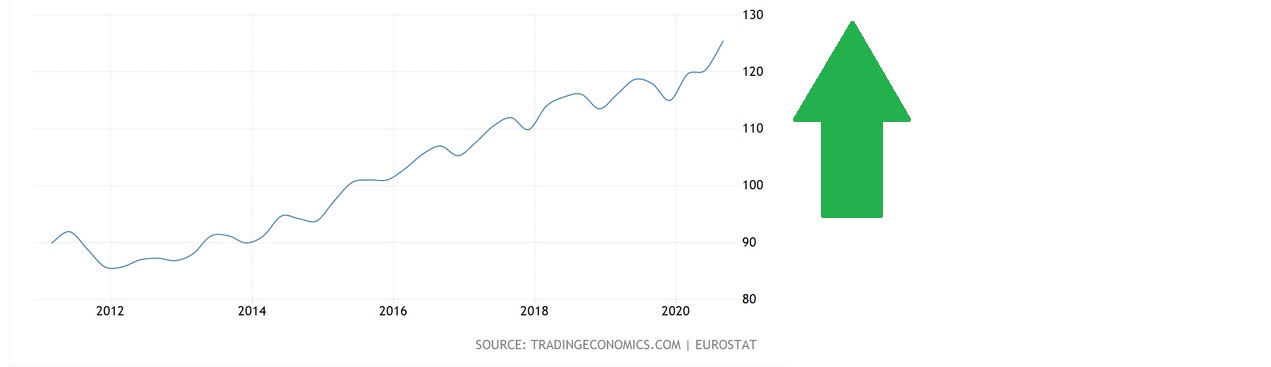

Lets go back to Danish housing for a moment. What impact, do you suppose, a zero percent rate for home loans might have on the housing market? Correct! Danish home prices have lifted in recent years, but since the beginning of 2020, the ‘Denmark House Price Index” has been skyrocketing!

“The housing market is doing well, and houses are now being sold for the highest prices ever. Prices are increasing in most of the country and plenty of sales are being completed,” said Nordea housing market economist Lise Nytoft Bergman.

Color me shocked. 🙂

Just kidding. Obviously. Recently, here in the US, we’ve seen the staggering home demand and price increases with interest rates in the mid-2s….I can only imagine the rocket-fueled price increases we’d see if rates fell further, settling in between 1% and 2%! And it could happen. If Minerd is right.

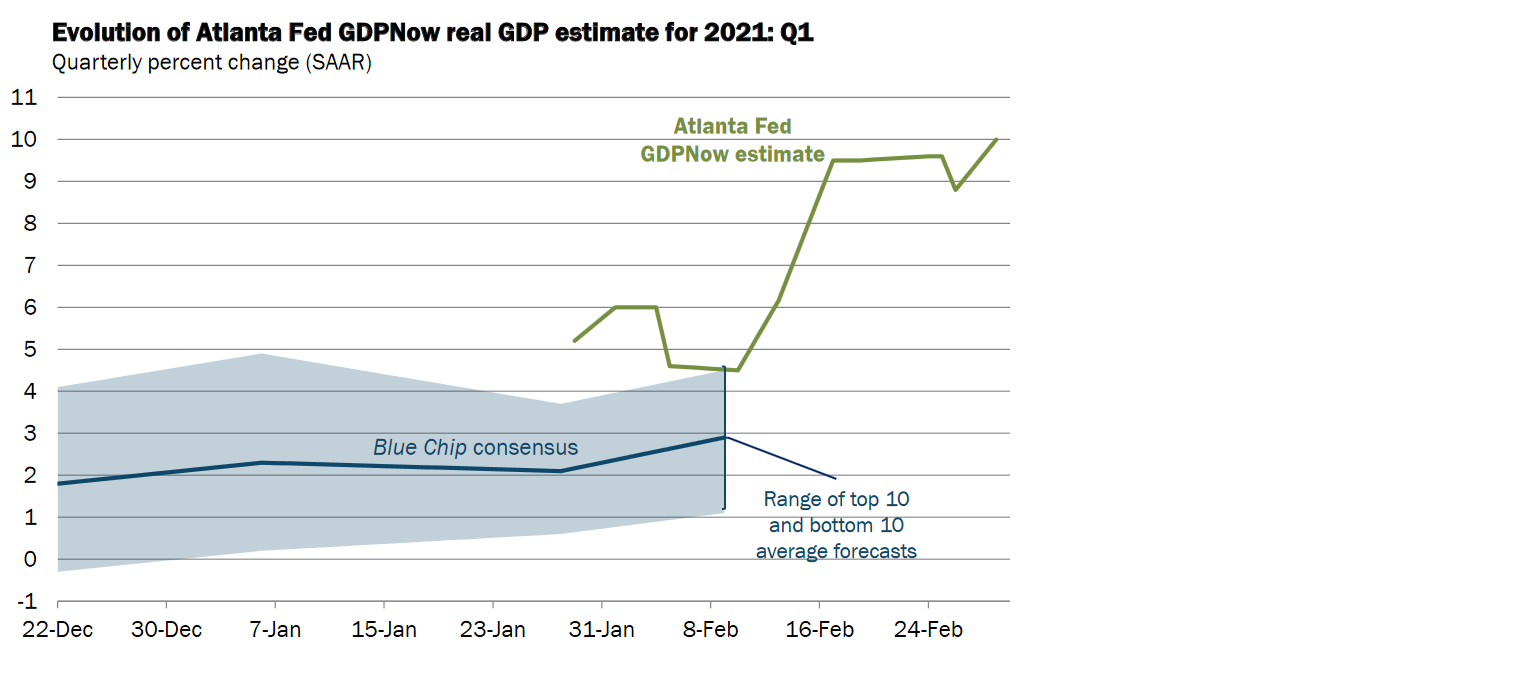

And all this is happening while the US GDP growth is going bonkers. Consider the latest reading from the Atlanta FED and their “GDPNOW” forecast:

Latest estimate: 10.0 percent — March 1, 2021

That is staggering. Here’s their chart:

In my experience, the Atlanta FED econometric model tends to overestimate GDP growth. But 10%? I’ve never seen a prediction this high. An outcome even close would be a staggering achievement for our economy. Absolutely staggering.

Finally, according to the CDC, as of 3/2/21 Covid-19 vaccine “total doses distributed” reached 102,353,940 … and total administered was 78,631,601. The vaccine roll-out is picking up steam … and this is before J&J makes a big push. Herd immunity can’t be too far off.

The stars are aligning. My opinion:

The US economy and GDP growth are about to explode — in a good way.

I hope you’re holding on tight. 2021 is about to get even more interesting. 🙂

- Terry Liebman