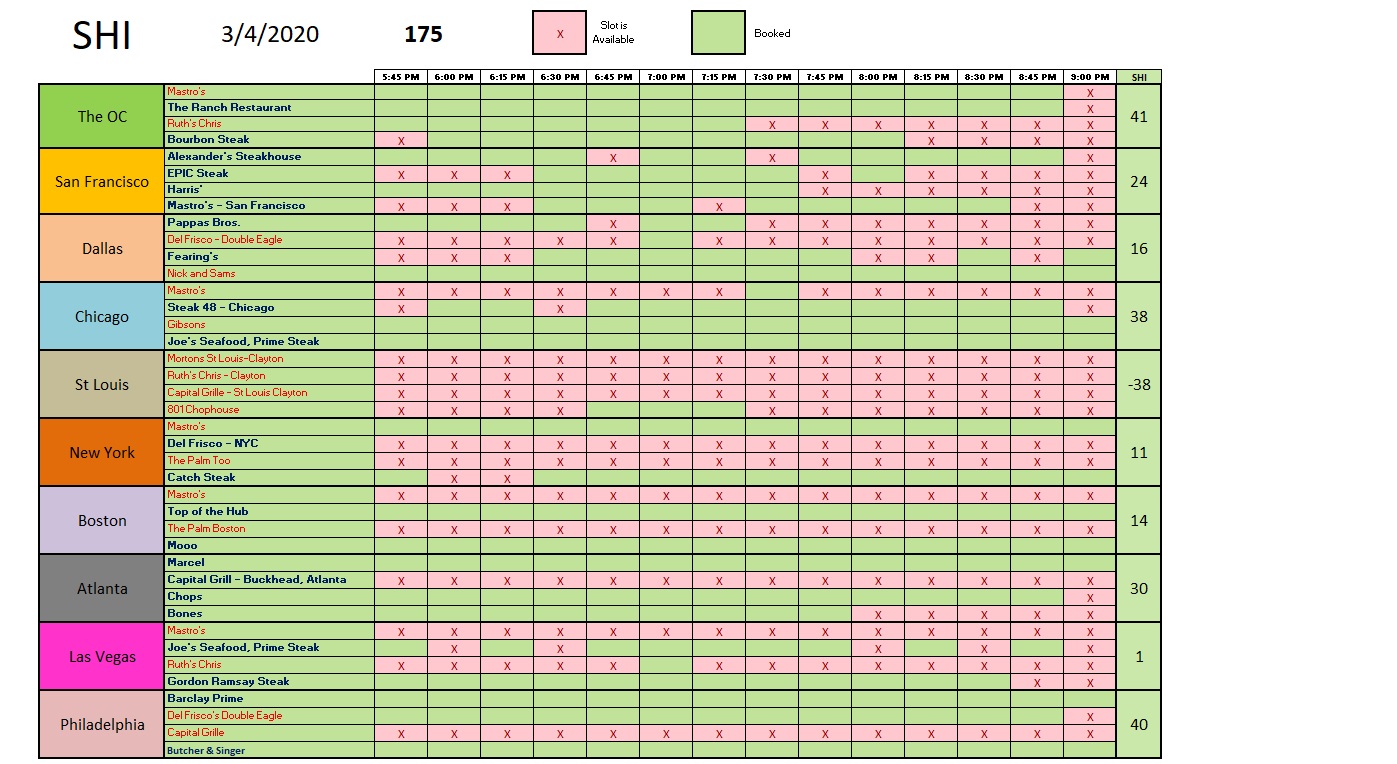

SHI 3.4.20 – Welcome to California, Comrade

SHI 2.26.20 – Reaching New Lows

February 26, 2020

SHI 3.11.20 – Out of an Abundance of Caution

March 11, 2020

“Bernie Sanders won the ‘Super Tuesday’ California primary.”

Sorry, but I personally find this outcome very disturbing. Not because I dislike Bernie … he seems like a nice guy. I’m sure we’d have a nice chat over a beer. No, because he holds deeply entrenched economic and financial beliefs that I find very disturbing. And he has been surprisingly successful in convincing millions of folks here in California — actually, more accurately, across the entire country — that his socialist economic agenda is the right approach. Millions of Californians now clearly believe their lives would improve under a socialist government led by Bernie. OK, to be fair to Bernie, he says is is a “Democratic Socialist” — NOT a socialist. But frankly, I have trouble finding the difference between the two.

Welcome to California, Comrade.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is about $85 trillion today. According to the most recent estimate, US ‘current dollar’ GDP now exceeds $21.7 trillion. In Q4 of 2019, first estimates suggest nominal GDP grew by 3.6%, following a 3.5% annualized growth rate in Q3. The US still produces about 25% of global GDP. Other than China — in a distant ‘second place’ at around $13 trillion — the GDP of no other country is close. In fact, the GDP output of the 28 countries of the ‘European Union’ has fallen behind, collectively now almost $2 trillion less that US GDP. Together, the U.S., the EU and China still generate about 70% of the global economic output.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

May you live in interesting times, the ancient Chinese curse suggests. Boy, I think we’ve left ‘interest times’ far behind … and moved right into “crazy” times:

- Italy just announced a closure of all schools in the country thru (at least) March 15th due to their growing Coronavirus challenge — a very real and legitimate problem, no doubt.

- Responding to growing Coronavirus concerns and its potential impact on both US and global supply chains and business activity as time passes, the FED made an “intra-meeting” cut interest rates by a full 1/2 of one percent, reducing the FED funds rate down to about 1.00%

- According to CNBC, approximately 440 “converences” in Asia, Europe and North America have now been cancelled because of Coronavirus fears.

- The Democratic party “Super Tuesday,” too, is in the rear-view mirror. Joe Biden and Bernie Sanders are the de facto winners.

- Responding to the FED rate cut, the 10-year Treasury plunged to new lows, settling in around 1% — a rate so low, by historic standards, it defies logic.

Crazy times indeed. I understand the choices above. Whether or not I’d make them, I do understand them. I do. All expect for the Bernie choice. This one, frankly, baffles me. But perhaps I shouldn’t be so surprised, after reading the comments today from 36-year old pre-school teacher Anya McGrath of Los Angeles who spoke with the Wall Street Journal:

“Bernie Sanders speaks for underserved people. I’m kind of all about getting money out of the hands of billionaires and getting it back to the people.”

Bingo. Well, there you have it. Just like all the historic socialist leaders, Bernie will separate those nasty billionaires from their fortunes, redistributing their money to all the needy, well-deserving pre-school teachers in America! He’s clearly a modern-day Robin Hood!

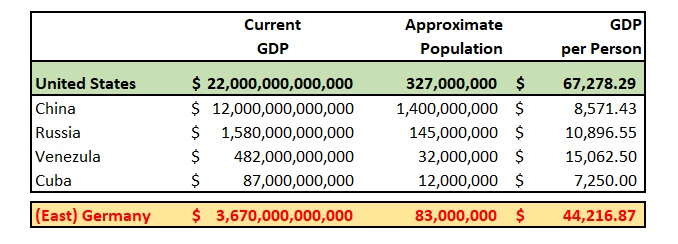

Or is he? Does the “socialist” agenda actually work for people like Anya? Let’s see how successful Bernie’s socialist and communist predecessors have been in redistributing wealth. Let’s examine the facts. Take a look at this chart:

The numbers on the chart are factual. In some cases, they may be a bit dated — for example, the Cuba numbers are about 5 years old — but the conclusions are irrefutable. The “per capita” income in socialist (or communist) countries is far lower than the per-person average income in the United States … or Germany.

What country possesses the largest oil reserves in the world? You might guess Saudi Arabia … and while you’d be close, you’d also be wrong. Saudi Arabia is #2. The largest oil reserves on the planet are in Venezuela. Surprised? Yeah, it’s a bit of a conundrum. With all their oil wealth, you’d expect the citizens to be rich. And you’d be wrong. Venezuela, the home of rampant food-shortages, hyper-inflation, and wide-spread abject poverty owns the largest oil reserves in the world. And the “average” Venezuelan citizen “earns” about $15,000 per year.

Look how well the folks in Cuba are doing. Ouch. 60 years after their people’s revolution, almost everyone is driving a 50-year old chevy. And living on beans.

And when looked at thru the lens of ‘purchasing power parity‘ or adjusted for currency and value compared to other countries — known as PPP, the Venezuelan number is even lower, closer to $11,000 per person, according to the IMF. Even worse, it has declined from more than $18,000 annual PPP back in 2013. People in Venezuela become poorer with each passing year.

By comparison, the PPP in Saudi Arabia (a ‘monarchy’ of sorts) — #2 on the oil reserves list — is currently close to $50,000 per citizen, per year. It’s interesting to note the difference between the Russian per-person GDP and the same metric in Germany. Remember, East Germany re-joined Germany with the fall of the Berlin Wall in 1989. Today, about 30 years after the reunification, the average German per-capital income is more than 4X that of Russia. Russia remains socialist. Germany, today, is a ‘democratic, federal parliamentary republic.’ And in 30 years has become a manufacturing powerhouse.

Sorry, Anya, but I don’t think a Bernie presidency would fulfill your hopes for wealth distribution. If history is any guide, perhaps the billionaires in a ‘Bernie America’ will become poorer, but so will you. OK … this is clearly my 2 cents. My opinion only. I’ll now step off my Bernie soapbox.

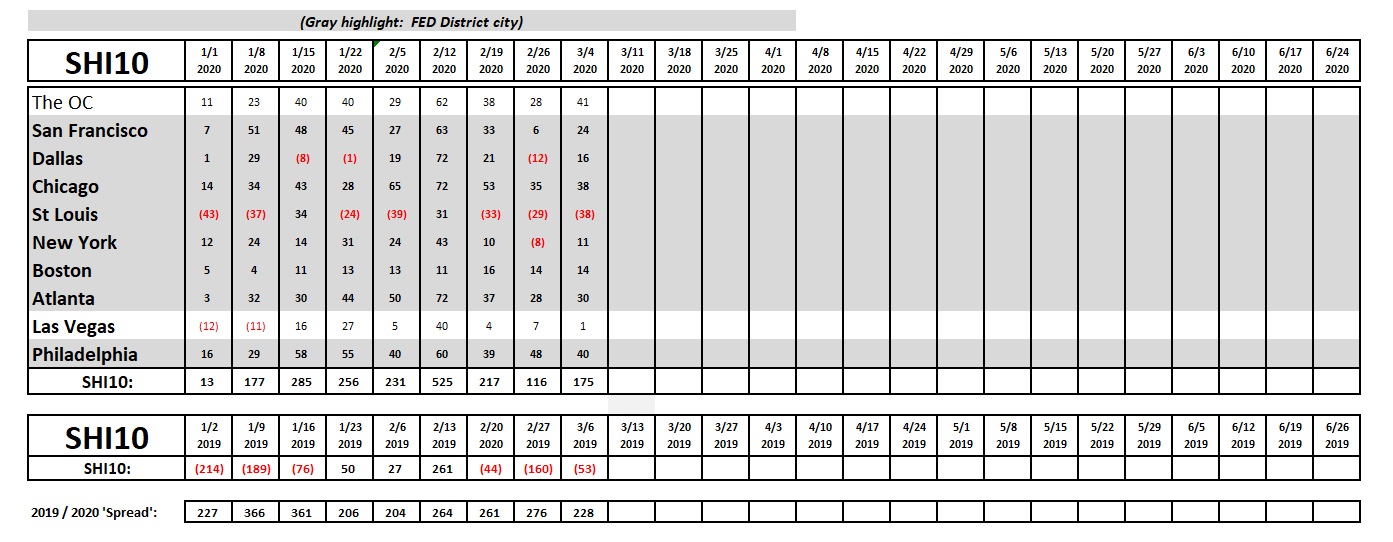

Has the Coronavirus scare impacted restaurant reservation demand for this Saturday around the US? Let’s take a look:

Nope. Not a dent, that I can see. In fact, most of our SHI10 markets show stronger reservation demand than last week. The biggest negative change is in St Louis, but this city has been trending poorly for weeks now. I don’t think virus fears have any impact on these results. Expensive steaks are in very high demand in the OC, San Francisco, Dallas, Chicago, Atlanta and Philly. Well-heeled diners, at tables of 4, seem more concerned with finding the perfectly grilled steak than catching the virus. Interesting. Here are the trend numbers:

Just one week ago, the title of my blog was ‘Reaching New Lows,’ talking about the unprecedented super-low rate on the US 10-year Treasury. Today it is even lower. In fact, as I write this blog, it is hovering right around 1.00%. Wow. Here’s a link to last week’s blog:

https://www.steakhouseindex.com/shi-2-26-20-reaching-new-lows/

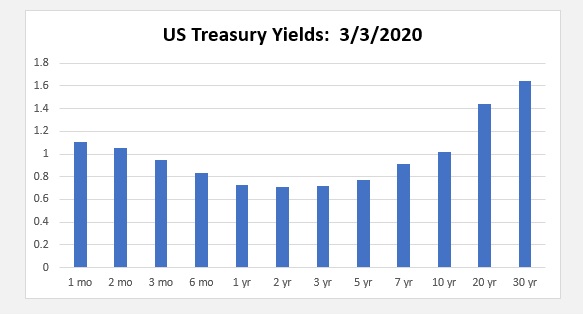

So, rates are low. The lowest they’ve even been. Further, the yield curve is severely inverted. Take a look:

The 2-year Treasury was paying about 0.71% yesterday, compared to 1.11% for the 1-month and 1.64% for the 30-year. The 3-month and 10-year are almost identical. So, I’m sure you’re asking, what does this mean?

Today, nothing. Not yet. The markets are frightened. Let’s see how it settles in. On the other hand, diners do not seem to be frightened at all. I asked a friend who flies frequently how the airports “look” today vs. a couple of weeks ago. His report, just earlier today, was: “Airports are 1/3 of what they were 2 weeks ago.” Wow. People are OK going to a crowded restaurant … but not an airport.

We’re way past “interesting times.” Crazy times indeed.

- Terry Liebman