SHI 3.6.24 – China Redux

SHI 2.28.24 – Money, Money, Money

February 29, 2024

SHI 3.13.24 – The Wind Beneath our Wings

March 13, 2024

China is the word’s second-largest economy.

As a result, China’s current and future economic vitality impacts economic conditions far beyond their borders.

China’s government recently “set” an economic growth target of 5% for 2024. That’s an ambitious goal for an economy experiencing consumer price deflation, an historic residential real estate slump, and export troubles here in the US. The US trade deficit with China fell significantly in 2023. China imports in the US declined 20% last year.

“

Can China achieve 5% growth in 2024?“

“Can China achieve 5% growth in 2024?“

I think its very unlikely. More likely, I believe China’s economy will shrink in 2024.

Arguing for the positive, ‘Personal Consumption Expenditures’ make up only 37% of China’s GDP. (Recall that number is about 70% here in the US.) So a decline in consumer spending has about 1/2 the impact in China vs. the US. But in the negative, ‘Gross Capital Formation’ is 43% of their GDP. And this China GDP segment is in free-fall at an accelerating rate.

Why is this important?

The expansion or contraction in China’s GDP in 2024 have far-reaching implications on the price of oil, global trade, the level of China’s exports, US trade tariffs, and the list goes on. Let’s explore a few.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding …. By the end 2023, in ‘current-dollar‘ terms, US annual economic output rose to an annualized rate of $27.94 trillion. After enduring the fastest FED rate hike in over 40 years, America’s current-dollar GDP still increased at an annualized rate of 4.8% during the fourth quarter of 2023. Even the ‘real’ GDP growth rate was strong … clocking in at the annual rate of 3.3% during Q4.

According to the IMF, the world’s annual GDP expanded to over $105 trillion in 2022. Further, IMF expects global GDP to reach almost $135 trillion by 2028 — an increase of more than 28% in just 5 years.

America’s GDP remains around 25% of all global GDP. Collectively, the US, the European Common Market, and China generate about 70% of the global economic output. These are the 3 big, global players. They bear close scrutiny.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

What is ‘Gross Capital Formation”? The World Bank defines gross capital formation as

“… outlays on additions to the fixed assets of the economy plus net changes in the level of inventories. Fixed assets include land improvements (fences, ditches, drains, and so on); plant, machinery, and equipment purchases; and the construction of roads, railways, and the like, including schools, offices, hospitals, private residential dwellings, and commercial and industrial buildings.”

Now, consider these comments posted in a December 7th, 2023 article in the EastAsiaForum:

“Forty years of continuous growth has transformed China into one of the world’s two largest economies. This is a remarkable achievement that has lifted hundreds of millions of people out of poverty and into the global middle class, consistently surpassing expectations and confounding those who predicted an economic bust.

That pace of growth is now slowing for several reasons. Like in many advanced economies, China’s population is getting older — a demographic transition that has been exacerbated by China’s one-child policy between 1980 and 2016. Globally, there is post-COVID-19 resurgence of economic nationalism. Trade growth, already suffering from market saturation, is slowing as manufacturers in Europe and North America reshore, diversify their sources of supply or their governments impose trade barriers.

But there is another brake on China’s growth. Its economy has for many years depended on outsized domestic investment in real estate and infrastructure and those investments are showing sharply diminishing returns. Local governments that rely on land sales for revenue need to service their debt and revenues are collapsing as the real estate boom falters.

Will China’s economy melt down as a result? Not necessarily — at least not in a financial crisis of the kind the West experienced in 2007–08. But it will not be easy to manage these problems, the remedies may be difficult, and the end result is likely to be much slower trend growth.

In joint research with International Monetary Fund economist Yuanchen Yang, we have estimated how much of China’s economy depends on real estate and associated infrastructure. In 2021, the direct and indirect impact of real estate in China’s economy was 22 per cent of GDP, or 25 per cent when factoring in imported content. If infrastructure such as roads, mass transit and water pipes that service residential and commercial real estate is included, the total rises to 31 per cent.

In the years immediately before the COVID-19 pandemic, the total was even higher. The only advanced economy in recent history with a similar share of real estate plus infrastructure investment in GDP was Spain during the run-up to the Global Financial Crisis, though that peaked below the 30 per cent level that China has now sustained for a decade.

The physical transformation of China’s cities over the past three decades has been remarkable. But looking at the cumulative building that has already taken place, it is clear that the construction growth engine cannot power China’s economy as it has in the past.

Real estate is durable. As the stock increases, the economic returns to construction decline. For example, floor area per capita of housing in China is now equal to or greater than France or the United Kingdom. While the United States’ housing stock remained stable at 65 square metres per capita from 2011 to 2021, China’s housing stock increased from 5 square metres per capita in 1992 to almost 49 square metres per capita in 2021.

80 per cent of that floor space is in smaller, poorer Tier 3 cities, which have not benefited nearly as much from agglomeration effects as the richer, more prosperous Tier 1 cities like Shenzhen, Beijing, Guangzhou and Shanghai, and mid-ranked Tier 2 cities. Tier 3 city populations are already in decline, prices are falling and vacancies in many regions are high.

Nationally, the ratio of real estate under construction to completed commercial real estate has been steadily increasing, suggesting a market in which developers cannot complete projects due to a lack of final buyers and funding. Infrastructure investment has similar challenges. Projected investment in high-speed rail vastly outpaces the growth in the number of people who are using it, and recent infrastructure investment has been concentrated in Tier 3 cities.

At the same time, local government debt has climbed relentlessly from around 5 per cent in 2006 to 30 per cent in 2018, even by conservative estimates, and regional private banks are also exposed. The central government can always decide to bail everyone out, but doing so while maintaining the credit growth needed to fuel the economy poses challenges.

Chinese household wealth is overwhelmingly concentrated in real estate. Even without a financial crisis, the central government will be forced to adapt to wean China’s economy off its dependence on this sector.

Beijing might use its sweeping powers to restructure and reallocate economic activity as it has done effectively in the past. There are also fiscal policies that would address this problem, such as increasing transfers to bail out local governments or allowing local officials to impose property taxes — though the latter appears off the table politically into the foreseeable future. The government can also attempt to redirect infrastructure investment into areas that are still underinvested in Tier 3 cities, including schools and hospitals.

China’s authorities have been effective at meeting economic challenges during its four decades of growth, but addressing this set of problems will be daunting even for them.”

Normally, I might discount such comments. However, these are Kenneth Rogoff’s words. Dr. Rogoff is an extremely well-known and accomplished economist, currently affiliated with Harvard University. His research and data is without equal.

To repeat, above Dr. Rogoff stated, “If infrastructure such as roads, mass transit and water pipes that service residential and commercial real estate is included, the total rises to 31%.” That is s staggeringly large percentage. Chinese residential real estate values are falling. Chinese citizens no longer believe buying another home or condominium is a smart place to store and grow wealth. The government has successfully crushed housing speculation across China. But, at the same time, they have crushed the widely held belief housing is a good investment. As home sales continue to plummet, China’s economy is poised to shrink further.

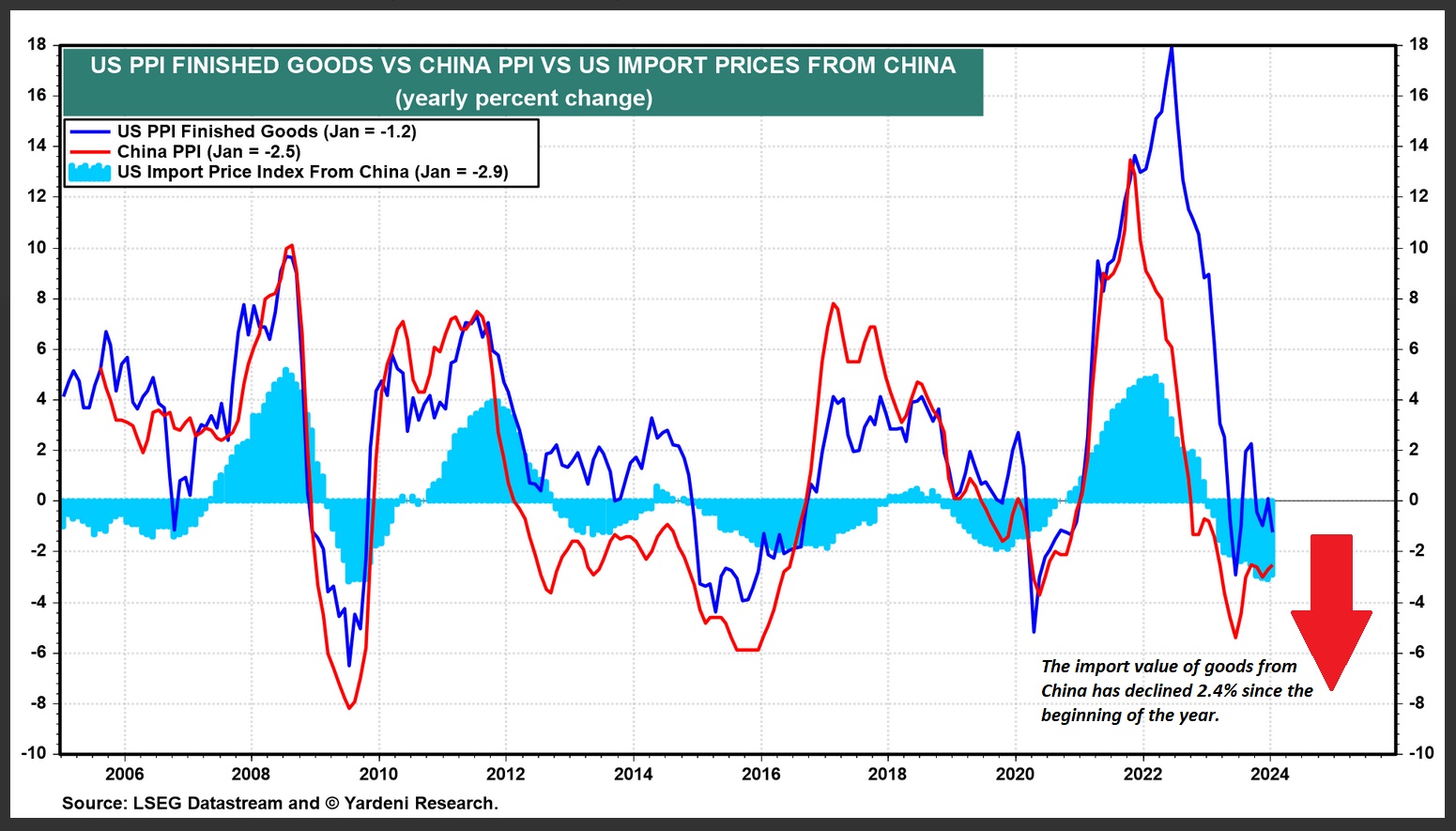

On March 4th, Ed Yardeni made these comments in an article he called “China: Pushing on a String?”:

“We started observing in 2023 that China is exporting deflation (chart). In recent weeks, that’s become widely recognized. This certainly is one reason why the Fed didn’t have to engineer a recession in the US to bring inflation down. China is having a property-led recession for us! The Chinese government might try to export their way out of it, which could exacerbate deflation around the world. Trump has already threatened to increase tariffs significantly on Chinese goods if he is reelected. Keep your seat belts on.”

“For us?” Funny. Here’s the chart he referenced above:

I added the RED arrow and text. The bottom line: Chinese goods are getting cheaper once again. The US is definitely “importing deflation” from China. But it’s worth noting US imports from China are steadily falling, year-over-year.

In 2022, US exports to China totaled $154 billion. In 2023, this figure fell slightly to $148 billion. However, US imports from China declined from $536 billion to about $427 billion in 2023 — a 20% collapse. The US is the largest consumer marketplace on the planet. For numerous reasons, China exports faces serious headwinds in the US at present. Without an export increase in the US, China’s manufacturing economy will continue to struggle. How does one increase sales in a difficult market? Lower prices. The aggregate price of Chinese goods, in the US, during 2024, is heading lower.

Evidence suggests the Chinese consumer is paring back their purchases of consumer goods. In the first 6-weeks of 2024, Apple reported iPhone purchases declined 24% in China. Yes, part of this drop-off is due to stiff competition from Chinese smart phone brands, like Huawei, but all smart-phone purchases, in the aggregate, declined 7% Y-O-Y, according to the Wall Street Journal.

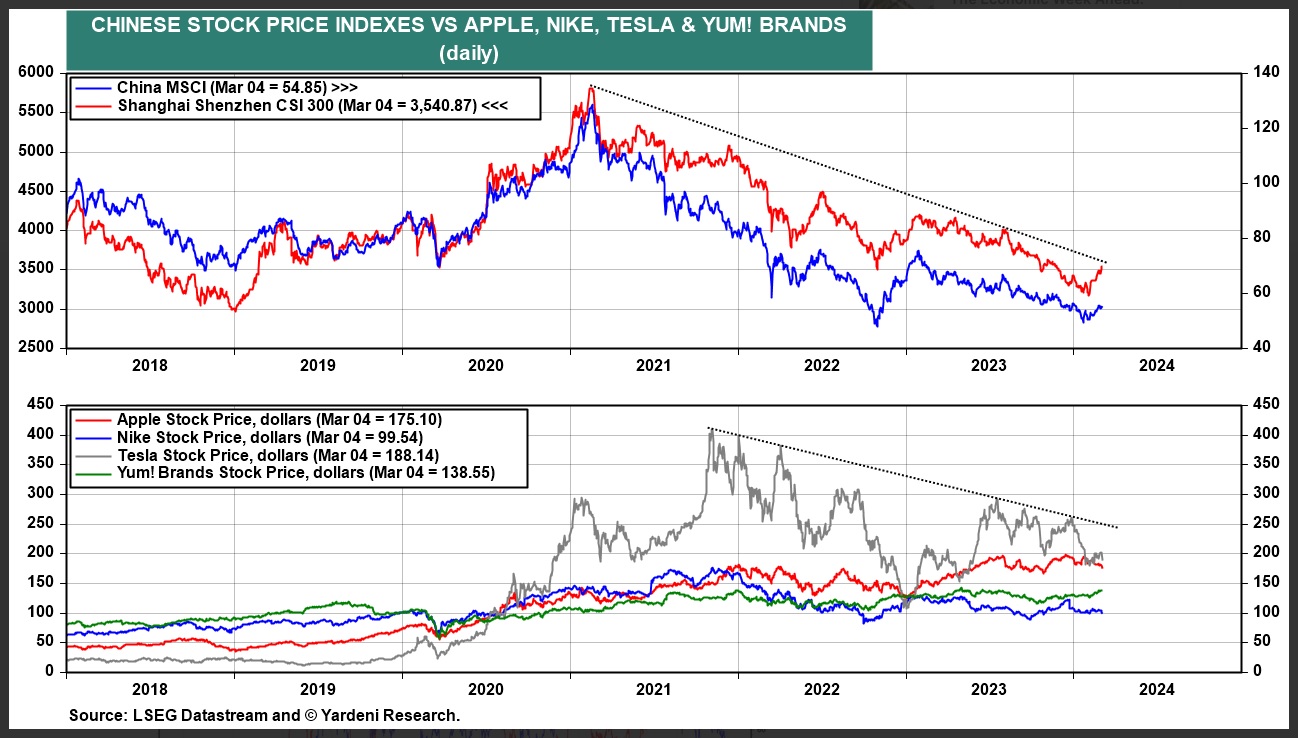

Once again, here’s a chart from Yardeni:

US companies with large exposure to the Chinese consumer are struggling in 2024. And so is the Chinese stock market, as a whole. As you can see above, the value of China’s two largest stock markets is down about 50% since their peak in early 2021.

Summarizing, it’s clear to me that Chinese export values will fall in 2024 in order for China to maintain, or increase, export levels in the US. This will be dis-inflationary for the US. In fact, allegations of “dumping” are likely to increase — and so are tariffs. Finally, as the demand / supply relationship for oil is global, and in very tight balance, Chinese stagnation, or worse, a recession, will likely reduce global petroleum demand in the coming year, resulting in stable, or even falling, oil prices for the foreseeable future. Again, this is dis-inflationary for the US. And both will happen during this exceptionally contentious election year. Interesting.

In my opinion, the probability for an economic contraction in China, during 2024, is far greater than an expansion, let alone achieving the 5% GDP growth target they announced recently. China’s economy and consumer prices will both deflate this year, in my opinion, no matter how deep China’s central government cuts interest rates or distributes financial stimulation. The die is cast.

To the steakhouses!

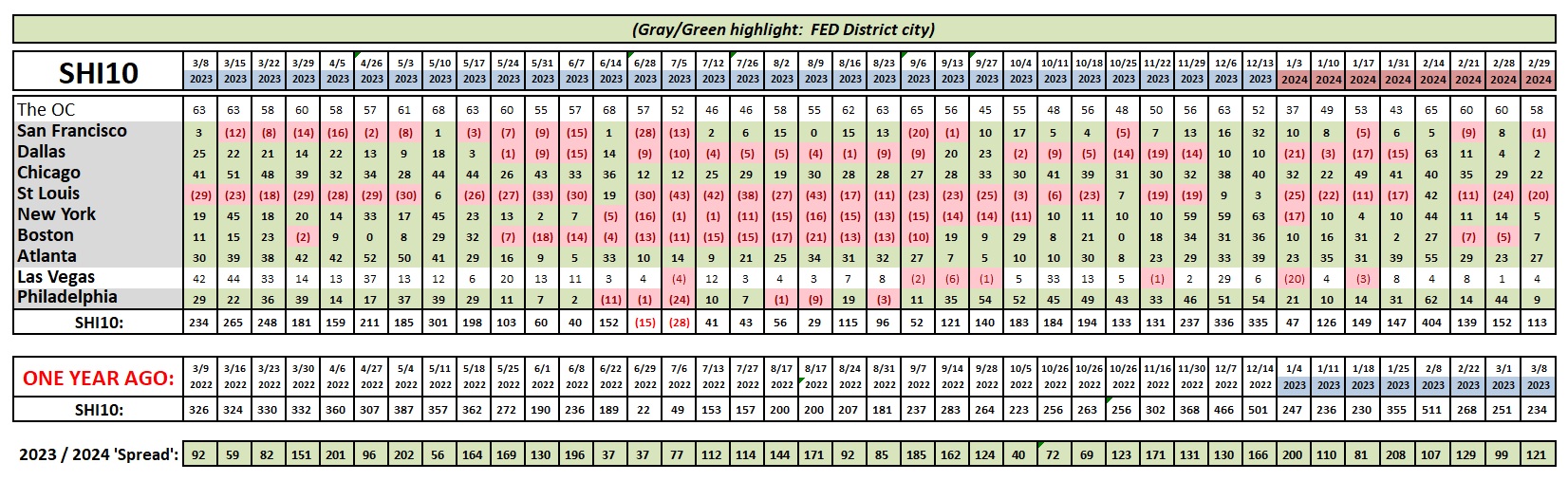

As we see above, expensive steakhouse demand across America is consistent once again. The “spread” for 2024 over 2023 remains quite similar to prior weeks. Our affluent American continues to spend extravagantly! Here’s the detailed report.

I hate be be such a spoil-sport, but I must repeat: Do NOT invest in an expensive steakhouse restaurant in St Louis. Clearly, the city is populated by Vegans, and has been so for years. And avoid New York, but for different reasons: Clearly there are too many wonderful steakhouses to pick from — their supply of opulent eateries must far exceed demand.

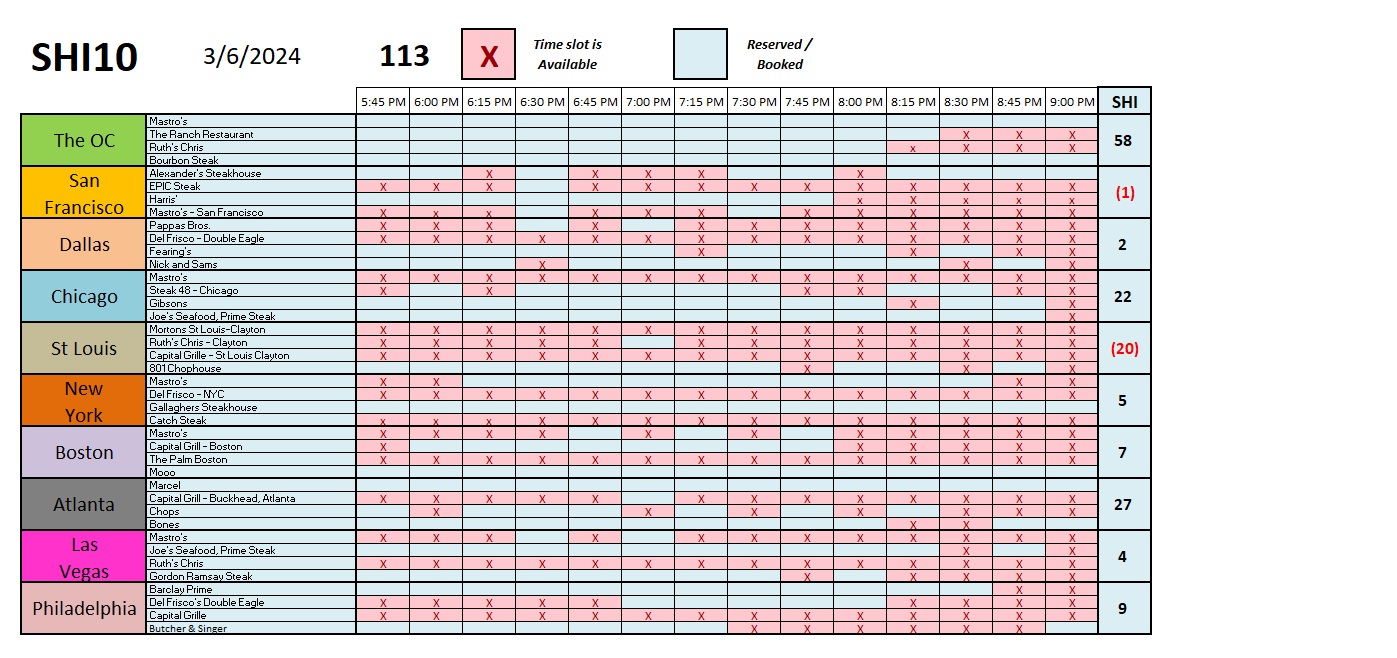

But here in the OC, pricey Filets are sizzling. Expensive eatery demand is strong, and reservations remain hard to get for Saturday next, a party of 4, and an $800 dinner check. Amazing.

<> Terry Liebman