SHI 4.4.18 Brevity is the Soul of Wit

SHI 3.28.18 History Repeats

March 28, 2018

SHI 4.11.18 Back to Basics

April 11, 2018

This week, brevity.

Unlike last week, this BLOG post will be brief. I have to give credit where credit is due: Shakespeare penned the title phrase, not me.

This week’s summary:

- Economic history is filled with turmoil and conflict. Countries seem to lurch from crisis to crisis. This is the normal condition.

- The current sabre-rattling notwithstanding between America and China, as long as the US Congress doesn’t invoke something as dumb as the ‘Smoot-Hawley’ Tariff act, this too shall pass.

- For now, I expect no meaningful mid- or long-term impact on our economy. Consumers continue to spend.

Below, you’ll find today’s SHI10 commentary.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will continue to be true for years to come.

Is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is almost $80 trillion today.

During the calendar year 2017, US nominal GDP increased by $833 billion … by an amount approximately equal to the market capitalization of Apple. At the end of 2017, US ‘current dollar’ GDP was almost $20 trillion — about 25% of the global total. Other than China — a distant second at around $11 trillion — no other country is close.

The objective of the SHI10 and this blog is simple: To predict US GDP movement ahead of official economic releases — an important objective since BEA (the ‘Bureau of Economic Analysis’) gross domestic product data is outdated the day it’s released.

Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric.

The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

Don’t get taken in by the fist-shaking and sabre-rattling. Fears of a legitimate trade war are overblown. As of January of 2018, China owned $1.168 trillion of US Treasury notes, bills and bonds. For better or worse, they are our business partner.

At least, this is my read of the tea leaves now. (See what I did here? Tea leaves? China? ) 🙂

The US economy is doing fine. S&P companies are generating record earnings. Consumers are spending their hard-earned — and borrowed — funds. Let’s see if they’re buying $80 steaks.

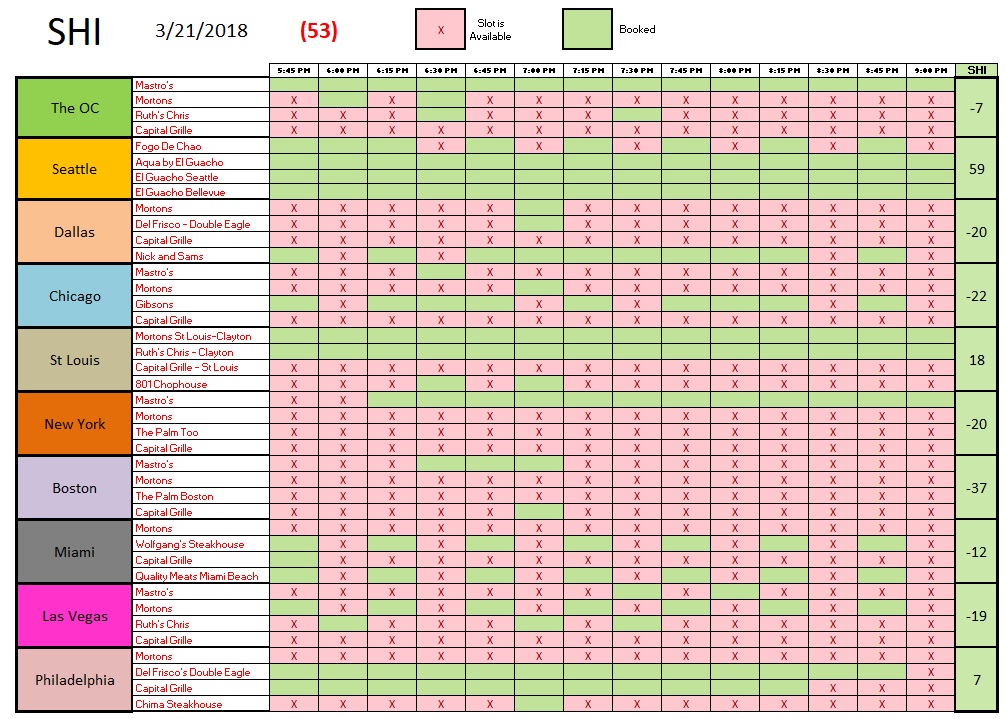

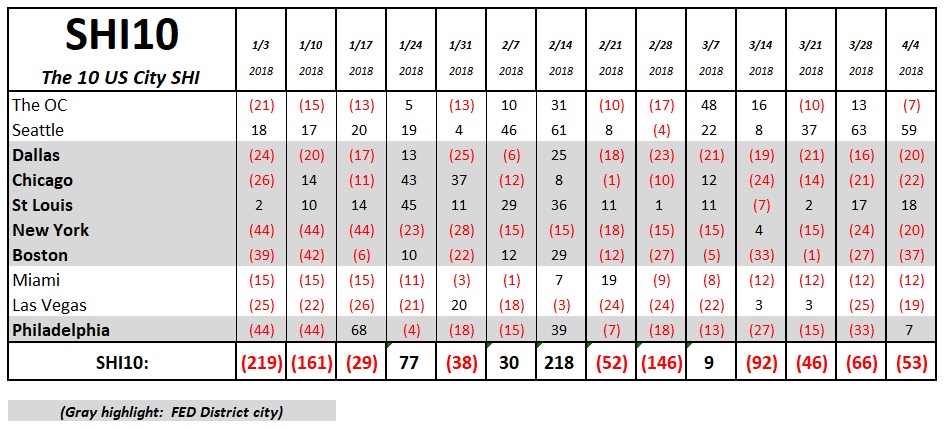

Yep, steaks are selling like hotcakes! Especially in — who would have guessed? — Seattle. Wow…two weeks in a row, Seattle is almost booked solid. Philadelphia recovered nicely from last week; St. Louis is pretty consistent. Here’s the long-term grid and comparison:

The SHI10 readings for the past 3 months are fairly consistent. I suspect our weekly results will improve with the weather.

The bottom line: The SHI10 is predicting solid economic performance for the foreseeable future. The administration’s budding trade-war with China notwithstanding, it’s steady as she goes.

- Terry Liebman