SHI 5.10.23 — Everyone Loves Mom!

SHI 5.3.23 — A City of Two Tales

May 3, 2023

SHI 5.17.23 — Elon For Prez!

May 17, 2023

Sunday is Mother’s Day.

Guys, get to work. Yeah, I’m talking to you. It’s time. Buy a card. Maybe a gift? And if you’re considering taking “mom” to your local expensive eatery for a great steak, make your reservations soon … because as you’ll see below, they’re going fast.

“

Happy Mother’s Day!”

“Happy Mother’s Day!”

And what about about money supply?

Right. That was a pretty sloppy transition. But I had to get there somehow. Because money supply growth since 2020 has been fascinating … especially when viewed in a discussion with GDP growth and CPI inflation. M2 growth skyrocketed in the 18 months following the pandemic. And I mean skyrocketed. So in addition to the impact of Mom’s Day on opulent eatery reservation demand, today we’ll take a closer look at the inner workings of M2, GDP and the CPI.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. Even as the FED rapidly raises rates! At the end of Q4, 2022, in ‘current-dollar’ terms, US annual economic output rose to an annualized rate of $26.14 trillion. During 2022, America’s current-dollar GDP increased at an annualized rate exceeding 9%. No wonder the FED is so concerned, right? The world’s annual GDP rose to over $100 trillion during 2022. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the 3 big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

In this blog, I’ve talked extensively about the difference between “real” and “nominal” as these terms relate to economic and financial statistics. I do this because main-stream media and economists offer little, if any, color on these metrics – but I consider the distinction to be very significant and very important in developing an understanding of the financial world.

For example, earlier today the most recent CPI report was released by the US Labor Department. According to that report, the cost of “all items” for all urban consumers – a metric known as the “CPI-U” – increased during April by 0.4%, and by 4.9% over the preceding 12 months. High level, this is within the range of what experts had expected. Food and ‘shelter’ prices moderated a bit during April, but energy and used car prices increased at a fairly fast clip.

So here’s a question for you. Is this price increase “real” or “nominal”? Sorry, trick question! 🙂

It’s really neither…but if we had to put a tag on it, I’d say nominal. That’s because inflation measures changes in the price of the things we consume. By definition, those changes are nominal, or current-dollar. That is essentially what the CPI, the PCE and other inflation metrics measure. An ‘inflation adjustment’ is the tool used to convert a nominal statistic into a real number. And inflation is always measured in current-dollars.

Gross Domestic Product (“GDP”) is always first measured and reported in real terms. Current-dollar GDP is always mentioned in the GDP release, but much in the way Prince Harry is mentioned in the line of succession in the British monarchy. That’s right: Prince William gets all the press and accolades – Harry, just a passing mention at best. As far as the experts are concerned, real GDP is the crown prince, and nominal GDP is only mentioned along with the “GDP deflator,” the inflation metric used to reduce the current-collar GDP figure down to the real number.

The logic of this approach is unassailable. Yes, to measure the true performance of the US economy, we do need to strip out gains attributable just to inflation. Only then do we have a precise measure and understanding of how the American economy is changing quarter over quarter. That is what the real GDP number tells us. But once calculated, why is this number considered far more important than the nominal, or current-dollar growth figure? Why does the nominal GDP number get the Prince Harry treatment here? Trust me, I’m not kidding here. You have to go to the sixth paragraph of the BEA report to find the current-dollar GDP information. Which is absurd, because the data is impressive!

Current‑dollar GDP increased 5.1% at an annual rate, or $327.9 billion, in the first quarter, to a level of $26.47 trillion.

Recall the real GDP growth number was a paltry 1.1% for the quarter. This is a meaningful measure. But the nominal GDP growth rate is important, too. Especially, when one considers the amount of press around recession forecasts. The word ‘recession’ must be the most oft discussed economic word in today’s financial press. Every news cycle is dominated with fear of a recession. But when was the last time you heard someone mentioned the fact that the US economy is still expanding at a robust clip? Right, almost never if at all.

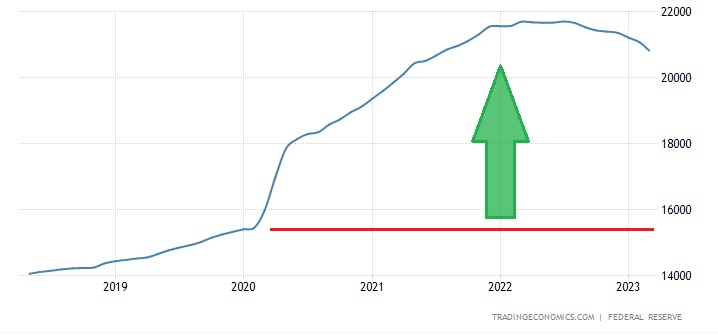

M2 is a measure of the US money supply. It includes cash, checking deposits, and other types of deposits that are readily convertible to cash such as CDs and is considered a broader definition of money than M1, which only includes cash and checking deposits.

Is M2 growth reported in real terms?

No, M2 is always nominal. M2 is never adjusted for inflation. I’m not suggesting it should be, I’m only making the point.

M2 was $4.7 trillion when the year 2000. 20 years later, as 2020, began, it clocked in at $15.4 trillion. In 2000, nominal GDP was $10 trillion. As 2020 began, just before the pandemic hit, it had reached $21.7 trillion.

M2 exploded between 2020 and July of 2022, when it reached a peaked at $21.7 trillion. In just 18 months, M2 expanded by almost 41%. During this same 18 months, nominal GDP reached at $25.2 trillion, an increase of 16%.

The numbers on the vertical right are in billions of dollars.

Fast forward to Q1 of 2023. M2 has now fallen – down to $20.8 trillion. Our nominal GDP, on the other hand, has continue to climb, reaching at $26.5 trillion, during Q1. M2 is now up 35% since 2020 … and nominal GDP increased by 22%.

My point is this: By now, it has to be obvious to every economics expert that Milton Friedman was generally right. Friedman, a Nobel laureate economist, is known as the father of the ‘monetarism’ economic movement, famously opining that “inflation is always and everywhere a monetary phenomenon.” His theories suggested inflation is always caused by excessive growth of money supply relative to GDP. If asked, Friedman would most assuredly say that a 41% M2 increase at the same time GDP grew by only 16% is hugely inflationary. And he would be right. It was inflationary. As the FED and its staff of 400 economics PhDs now realize. 🙂

And now that money supply is shrinking, concurrent with a still growing GDP, it makes sense that inflation is moderating.

It’s also worth mentioning much has changed in the 50-or-so-years since the monetarism became popular. I’m sure the FEDs 400 PhDs would echo this sentiment, suggesting the relationship between money supply growth and inflation has weakened in recent decades due to changes in supply and scale of financial innovation, globalization, and monetary policy frameworks. And they would probably add targeting money supply may not be feasible in a world with almost endless sources of money creation.

Regardless of their protestations, Friedman was generally right. Sorry guys. Congrats on your PhD … but you might want to go back to school and study up on monetarism.

Is the shrinking M2 a concern? No. M2 increased by more than $6.3 trillion in 18 months. It has now shrunk by less than $1 trillion in the past year. Our financial system still has a whole lot of excess cash sloshing around. At current levels, I’m not concerned that a shrinking M2 is inherently deflationary or recessionary. But I’m keeping an eye on it.

To the steakhouses?

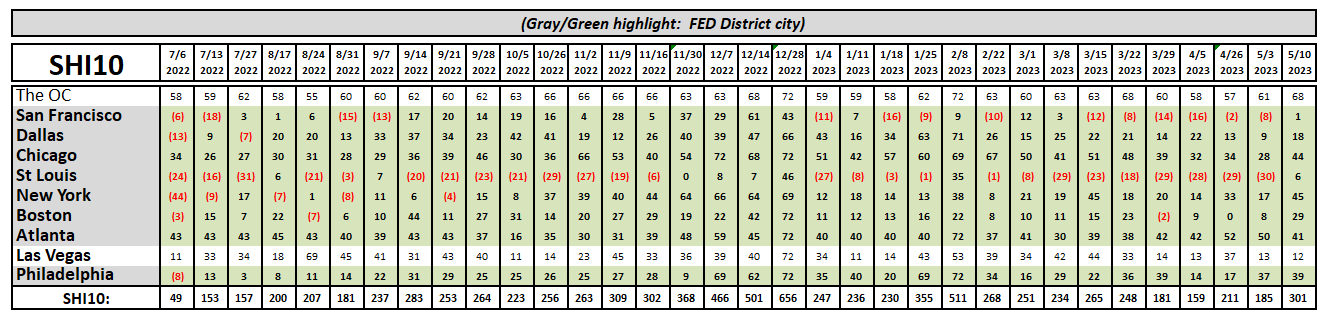

Yes, mom is popular this week! I attribute the SHI10 “bump” to mom. Here in the OC only two time slots are available on Saturday evening — but not until just before mom’s bedtime! The other three high-priced steak houses are fully booked.

Even St Louis has a fully booked restaurant this week! Miraculous! Here’s the trend report:

As we see above, the SHI10 jumped from 185 to 301 this week. That’s a significant bounce. But I suspect it can be fully attributed to Mother’s Day. I expect next week’s SHI figures to revert to the longer term trend we’ve been seeing in the past weeks.

Summarizing, I remain firmly in the economic expansion camp. I know this is a very unpopular position these days. Just about public opinion I hear or read suggests a widespread recession is just around the corner. And if one is in the mortgage or existing home sales business, I agree: You are deeply in a recession. And you’re likely to remain there for a while. Because as I’ve said before, FED-fueled interest rate hikes come on fast … but dissipate very slowly. It’s quite likely the FED will leave short-term rates at these lofty levels for a quite a while. But eventually, rates will moderate and the segments of the US economy that are heavily reliant on debt will thaw. And recover. And then thrive once again.

Am I worried the debt ceiling “thing” could become a serious problem? No. Don’t get me wrong: America does have a serious debt problem. We have to deal with it sooner or later. But current hyperbole and political brinkmanship aside, the ceiling will be lifted in time. Democrats and Republicans alike must realize their failure to do so would be political suicide.

<> Terry Liebman