SHI 5.3.23 — A City of Two Tales

SHI 4.26.2023 — The Best Burger Ever?

April 26, 2023

SHI 5.10.23 — Everyone Loves Mom!

May 10, 2023

I know, this lead-in and title are a bit confusing. What am I talking about? Tails? Tales? Cities or kitties? Stay with me while I clarify and move on from my journalistic hyperbole. A Dickens classic will help:

“It was the best of times, it was the worst of times, it was the age of wisdom, it was the age of foolishness, it was the epoch of belief, it was the epoch of incredulity, it was the season of light, it was the season of darkness, it was the spring of hope, it was the winter of despair.”

So begins the famous novel by Charles Dickens, A Tale of Two Cities, and the turbulence of the French Revolution.

Turbulence. There is no shortage of turbulence in America today. The melting of the Sierra’s epic snow pack is certain to ensure California’s waterways are extremely turbulent as spring becomes summer; our esteemed elected officials in Washington have assured us plenty of turbulence as they negotiate increasing the current US debt ceiling; and, every economist on the planet has a personal, and often divergent, opinion about FED, inflation, interest rates and the looming US recession.

“

Tales and tails … two very different things.”

“Tales and tails … two very different things.”

Divergent is another excellent word. As I write this blog, the FED readies their latest interest rate move. Will they raise again? Will all voting members agree on the move … or will there be divergent opinions? We’ll know shortly.

And the answer is important. Because a rate hike will have further economic repercussions. ‘Unrealized’ bank losses will immediately increase. Car and home loans will immediately become more expensive. The odds of another bank failure increase. And so does the probability of a US recession.

Are these the best of times … the worst of times … or something in between?

Many economists and analysts have been sounding the alarm for months, warning the US economy is heading for a crash landing that could rival the Great Recession of 2008-2009. Their evidence: Further FED tightening, slowing GDP growth, the US debt ceiling crisis, our inverted yield curve, the trade-war with China, the Russian invasion in Ukraine, the bank crisis, commercial real estate crash, weakening consumer confidence, and rising consumer and corporate debt. They argue that these factors are creating a perfect storm that will eventually trigger a contraction in output and employment, leading to lower incomes, higher unemployment, and a rapidly contracting US economy.

Other experts are far more optimistic. They dismiss these gloomy forecasts and contend that the US economy remains resilient and robust. Their arguments are supported by strong underlying fundamentals such as falling inflation, solid consumer spending, a healthy American consumer balance sheet, and a resilient labor market. They claim that these factors will outweigh the negative effects of the external shocks and uncertainties, and that the US economy will continue to expand at a moderate pace. They assert that the fears of a recession are overblown and exaggerated by the “experts,” the media and political hyperbole.

I still think it’s something in between.

Turbulence is always frightening and unsettling for all of us. It’s only human to fear the unknown. Personally, I am very concerned about the California runoff and the debt-ceiling Kabuki theater playing out in Washington. Bumpy roads, both.

But today we’ll talk about the potentially looming US recession … and the financial impact of today’s FED decision.

It’s what I do. 🙂

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. Even as the FED rapidly raises rates! At the end of Q4, 2022, in ‘current-dollar’ terms, US annual economic output rose to an annualized rate of $26.14 trillion. During 2022, America’s current-dollar GDP increased at an annualized rate exceeding 9%. No wonder the FED is so concerned, right? The world’s annual GDP rose to over $100 trillion during 2022. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the 3 big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

The ‘Cal State Fullerton University 2023 Spring Economic Forecast has been released. Here’s the hyperlink if you want to take a look (right click, open in new tab):

Make no mistake: They do a GREAT job here. This 43 pager is chock-full of excellent data and analysis. I enjoyed it thoroughly.

But I have a few problems with it, as I’ll discuss below. But, first, let’s discuss the obvious: Who am I to cast stones? The experts over at Cal State Fullerton, ‘College of Business and Economics’ have every right — frankly, more — than I to make economic predictions. More, I would argue, because the authors of their most recent Spring Economic Forecast are both PhDs and, in comparison, I an economic simpleton, with only an Economics BS to my name. And, truth be told, that was only a ‘dual minor’ as my actual college degree was granted in ‘Finance.’

So who’s forecast should you believe when making your business and investment decisions in the months to come? You decide when you’re done reading today. 🙂

Part of the issue I have with their forecast, frankly, is presentation style. And part is content.

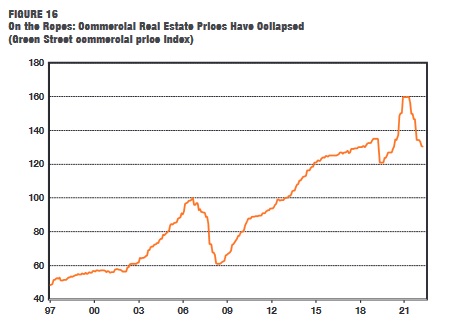

Let me talk about style first. Facts are facts — unless you are Donald Trump and you are able to make up your own — but the way facts are presented can often skew the reader’s impression. Consider this image clipped from page 20 of the CSUF forecast:

That drop-off on the right is precipitous. The words used by CSUF to describe it are above, directly under “FIGURE 16” and say:

“Commercial real estate prices have collapsed.”

Wow. That’s an aggressive conclusion. Have they actually collapsed?

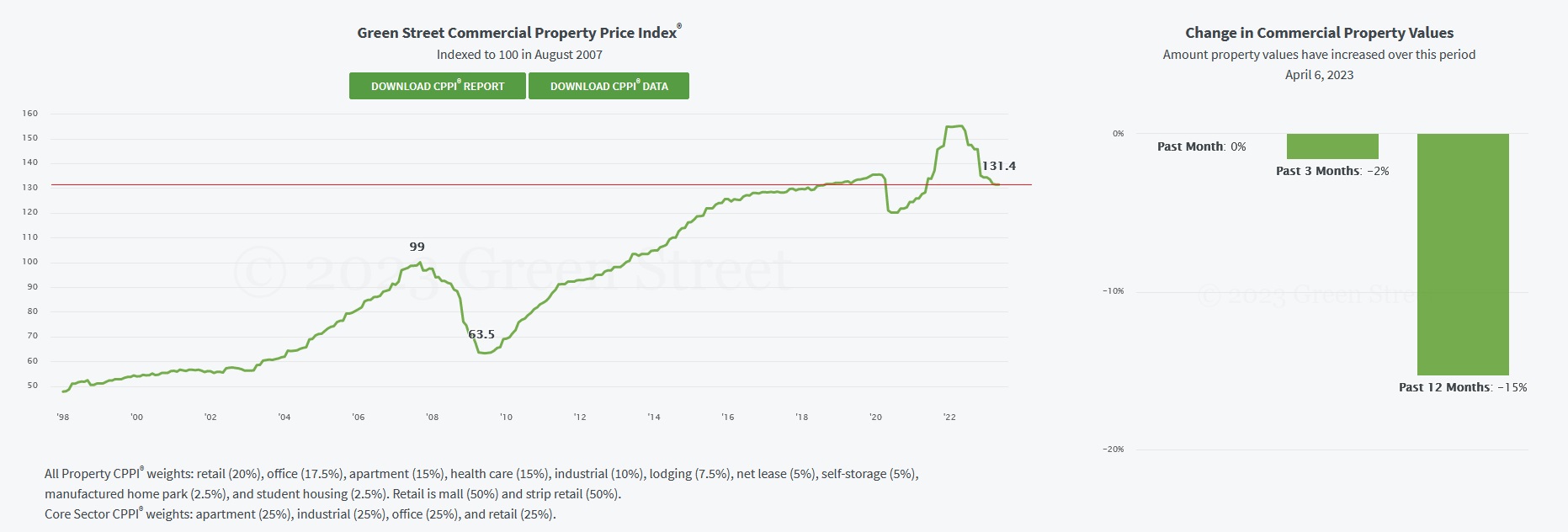

No. First, the source of the CSUF image is Green Street. Below is the actual graph provided by Green Street. The referenced “collapse” is most assuredly a value decline. No doubt, the index has definitely declined. Significantly.

But has the index collapsed? Again, no. I added the red line for context … and note that an index-value of 100 took place in August of 2007. To my eyes, the post-pandemic period is extremely turbulent — first falling … then rising rapidly … and now falling again. Turbulent.

Note also the index is a ‘blend’ using retail, office, multi-family, health care, industrial, hotels, NNN leases, self-storage, mobile home parks, and student housing projects. Have all commercial property segments lost value? Once again, no. Values are all over the map — some are UP and some are down — depending on property type.

Let’s move from style to content and focus on a few CSUF discussion points. Let me start here. The CSUF forecast opines:

“All this points to a scenario where a recession is unavoidable. We expect it to hit between Q3 and Q4 of this year and last about 10 months.”

Their concerns:

- GDP growth is slowing. 2023 Q1 growth was only 1.1%.

- The consumer’s ‘excess savings’ is dwindling.

- The inverted yield curve doesn’t lie.

- The bank balance sheets hide $2.2 trillion of ‘mark-to-market’ losses — MTM losses which exceed the total market capitalization of the 4,400 US banks of $2.1 trillion. The commercial real estate ‘bust’ is very concerning.

And the list goes on. Are they right? Is there reason to worry?

Sure. Plenty.

And moments ago the FED raised short term rates again — now at a top-of-range at 5.25% — adding fuel to the fire. This was a bone-head move, in my opinion, and it will not play out well in the banking system. Alas……

OK, back to the CSUF concerns. Yes, I’m concerned too. But I am not yet in the “recession is imminent” camp. I still believe our US economy, in the macro, is very resilient and will continue to grow. For the moment, anyway.

Here are my thoughts, addressing each of the CSUF worries above:

- Yes, GDP is indeed slowing. Slowing was inevitable. However, while the annualized Q1 ‘real’ growth rate was 1.1%, the nominal or current-dollar growth rate during Q1 was a sizzling 5.1%. It was adjusted down to 1.1% by an inflation factor. Current dollar annualized GDP is running $26.47 trillion! This is huge!

- Sure, consumers are spending their cash. And they’re using credit cards too — credit card balances are up. However, it’s important to note that at the end of 2022, American households had a ‘net worth’ of almost $148 trillion. Including amost $5 trillion in “checkable deposits and currency.” That same line-item was about $3.2 trillion in 2020. Excess savings may be dwindling, but American households remain flush with cash.

- The inverted rate curve is indeed inverted. It is often the proverbial ‘canary in the coal mine’ and might be here. We’ll know for sure in a year or two. 🙂

- The bank mess is definitely a mess. And it was made even messier by the “deal” the FDIC gave the Chase to acquire the assets of First Republic Bank. In my opinion, that was a HUGE mistake. JPM Chase should have been forced to buy the common stock and preferred stock in addition to the assets. Even if they only paid $3 bucks for the common and full price for the $1.35 billion of preferred, that would have only increased their cost by a billion or two. But by wiping out ALL the shareholders, the FDIC told the shareholders of other smaller, regional banks, “you may lose your entire equity investment” if the share price falls too low and we’re forced to step in and take over. By wiping out all the First Republic shareholders, the FDIC dumped gasoline on the bonfire. This could get ugly.

I expressed my opinion on “recession odds” in my 3.8.23 blog. I opined that unless and until the FED funds rate eclipses 6.25%, I felt the US economy was resilient enough to muddle thru. Even as the FED moved to 5.25% today, I still believe we can avoid an economic contraction because of all that cash sloshing around out there. My comment from that post:

Here’s today’s take away: The current rate hike-cycle began with the federal funds rate near zero. Now we’re close to 5%. And the FED assures us they aren’t yet done raising rates. Assuming they finish this cycle at or below 6.25%, I will opine that recession odds are about 50/50. Above that rate, recession odds increase dramatically. And if they go above 7% … look out below. The US economy will contract.

And here’s the blog post itself:

https://steakhouseindex.com/shi-3-8-23-snail-tracks/

If the bank “thing” becomes a conflagration, that might change my mind. We’ll see what the FDIC and FED do now. As I put the finishing touches on this blog, I’m watching another perfectly healthy, 67 branch strong, $41 billion bank get hammered in the “after hours” stock markets. Already depressed, their stock price is down 55% in after-hours trading. Staggering. Pacific Western Bank is on the ropes. Why?

Fear. Irrational, run-away stock investor fear. Investors are worried the stock price may plummet to zero … so they are selling before it does … causing it to plummet to zero. A self-fulfilling prophesy. This is ‘First Republic Bank, Act 2.’ This is ugly.

To the steakhouses! I need a drink.

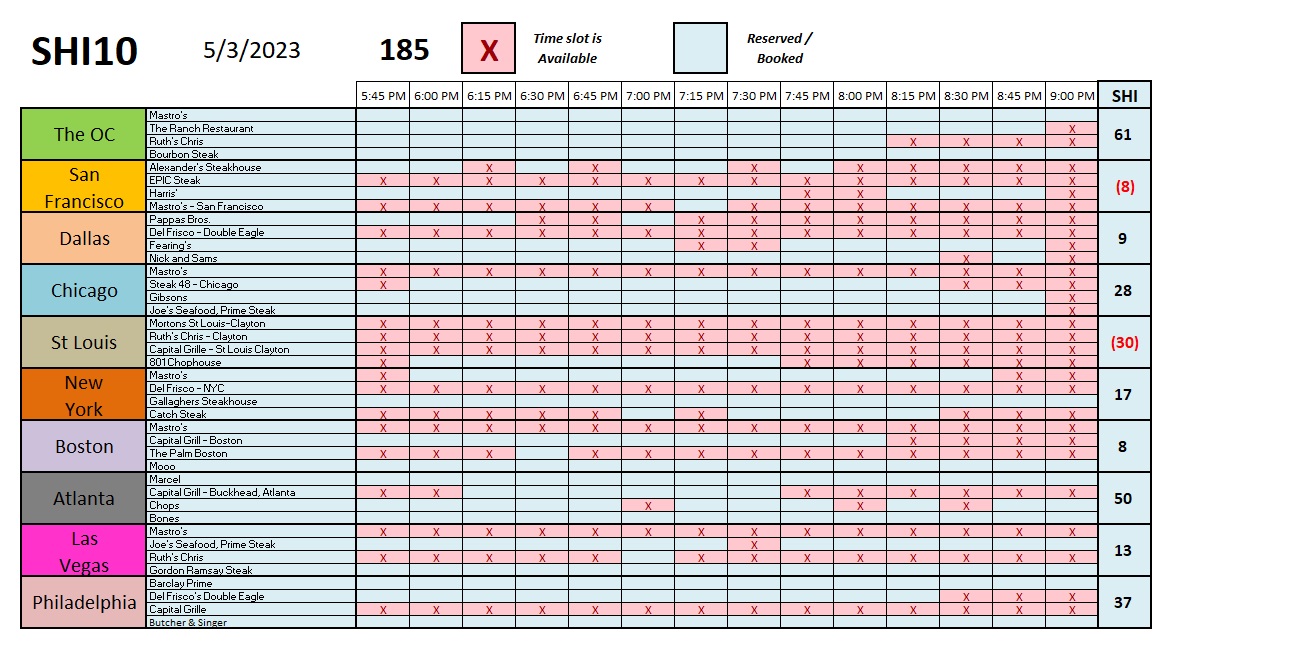

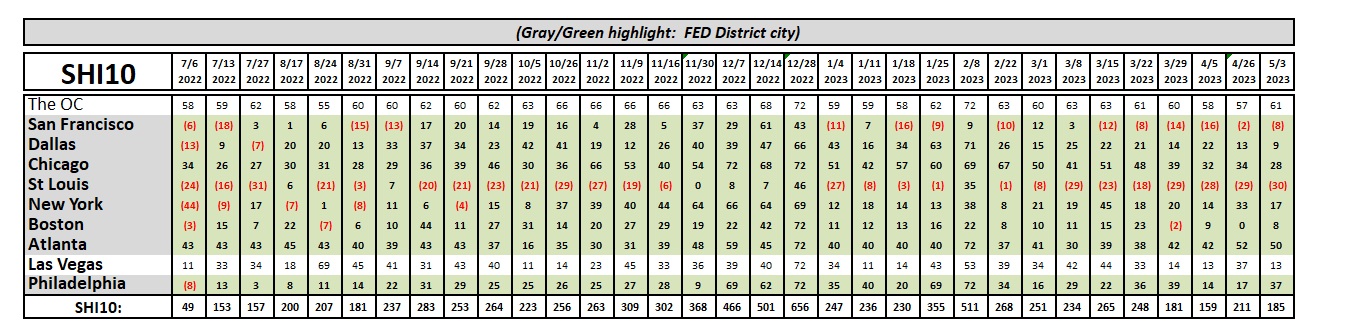

There’s not much to report, other than the steak houses are looking pretty quiet in ‘Vegas this week. This is new:

A SHI10 reading of 185 is consistent with prior weeks … so no concern there … but that sizable slow-down in ‘Vegas might be a worrisome change that we’ll have to keep our eyes on. Up to now, ‘Vegas has been been generally booked:

Earlier today, the FED raised rates again. But you already knew that. Life just became a little more expensive for the typical American consumer. Prime rate went up again — now 8% — from its low-point 18 months ago of just 3.25%; the average credit card rate is now about 20%; and, don’t even ask about mortgage rates.

But every coin has two sides. What’s bad for the consumer is great for the banks. Defaults aside, the banks are making bank! 🙂

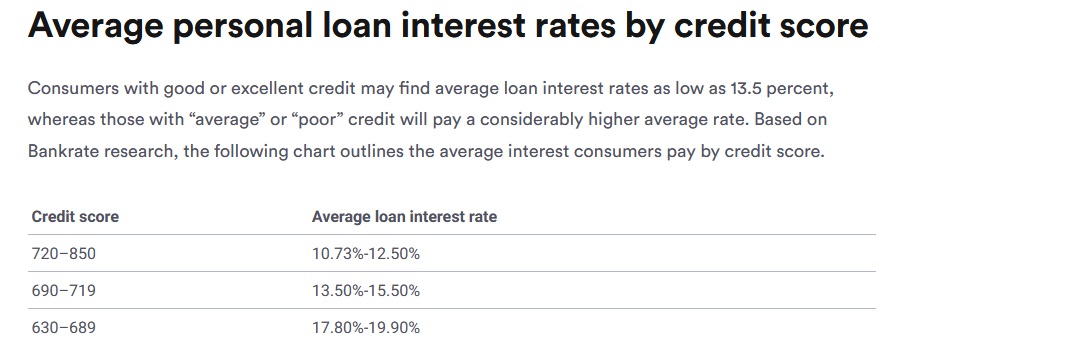

The days of low, low interest rates are far behind us for now. Looking for a ‘personal loan’? You’ll be paying loan-shark level rates, according to Bankrate.com:

The days of negative sovereign-debt rates and low, low home loans are but a distant memory. It’s so ironic that the banks, in general, are under the gun at the same time their net-interest revenues are growing like a weed.

Ahhh…the good old days. Gone for now. Well, as the FED raises rates yet again, it feels like a hammer-blow on the knee of the American economy and consumer. We’ll see what else breaks. Interesting enough: I rarely agree with Senator Elizabeth Warren on much of anything. But she and I agree that the FED has raised rates too fast and too far. Maybe we’ll become best-buds?

<> Terry Liebman