SHI 4.26.2023 — The Best Burger Ever?

SHI 4.5.23 — Big Macs and Knock-On Effects

April 5, 2023

SHI 5.3.23 — A City of Two Tales

May 3, 2023

Before I get to that, let me apologize. I failed to produce a blog two weeks in a row! Perhaps you noticed? ? Well, my skis don’t ski on their own. I had to go and keep them company! But I’m back.

Globalization is nothing new.

Consider these historic words from a well-known Brit:

“What an extraordinary episode in the economic progress of man …. for any man of capacity or character at all exceeding the average, life offered, at a low cost and with the least trouble, conveniences, comforts, and amenities beyond the compass of the richest and most powerful monarchs of other ages.

The inhabitant of London could order by telephone, sipping his morning tea in bed, the various products of the whole earth, in such quantity as he might see fit, and reasonably expect their early delivery upon his doorstep; he could at the same moment and by the same means adventure his wealth in the natural resources and new enterprises of any quarter of the world, and share, without exertion or even trouble, in their prospective fruits and advantages….

He could secure forthwith, if he wished it, cheap and comfortable means of transit to any country or climate without passport or other formality and could then proceed abroad to foreign quarters, without knowledge of their religion, language, or customs, bearing coined wealth upon his person, and would consider himself greatly aggrieved and much surprised at the least interference.”

That well-known ‘Londoner’ was John Maynard Keynes. He wrote those words about 100 years ago, just following WW1, as he lamented about economic losses beyond the horrible human tragedy.

No, globalization is not new. Since the earliest travels of Marco Polo – and before – peoples of the world have endeavored to conduct business far beyond their immediate neighborhood. Keynes’ lament was reflective of only the latest chapter at that time. Before WWI, he and many other Londoner’s believed their economic largess was permanent. But WWI destroyed global supply chains as easily as bridges. Both would need to be rebuilt.

Ironically, both need to be rebuilt today. Infrastructure is crumbling in cities across America and pre-Covid supply chains aren’t much better off. Perhaps even more ironically, the root cause behind the broken bonds of the 1920s was first a war then a pandemic; and today – about 100 years later – first a pandemic and then a war.

By now you’re probably asking yourself, “OK, and this has what to do with the best burger ever?”

“

Globalization and Burgers?”

“

Globalization and Burgers?”

Sure. What began as a strictly American phenomenon is now global. Today, McDonalds operates in over 100 countries across the globe — more than 1/2 of all — with over 38,000 restaurants. That’s about as global as it gets. But as global as the Big Mac might be today, “how” that burger is made is changing. A lot. Both here in America and across the globe. Post-Covid and the ‘Ukraine Invasion,’ supply chains and labor resources are changing dramatically. We can argue whether the catalyst was the ‘remote work’ movement, accelerated technical developments, or something else. But whatever the trigger, the impacts on the future of product development and global work are absolutely exhilarating and fascinating.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. Even as the FED rapidly raises rates! At the end of Q4, 2022, in ‘current-dollar’ terms, US annual economic output rose to an annualized rate of $26.14 trillion. During 2022, America’s current-dollar GDP increased at an annualized rate exceeding 9%. No wonder the FED is so concerned, right? The world’s annual GDP rose to over $100 trillion during 2022. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the 3 big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

Here’s an important newsflash From McDonalds:

McDonald’s is ready to debut what it’s calling its “best burgers ever.” The company announced today it is making a few changes to its burgers, including new, softer buns and more Big Mac sauce on its signature Big Macs. Some tweaks have also been made to the cooking process to yield a more consistent sear and meltier cheese, and the company is adding white onions at the grill for a caramelized flavor.

The changes were first introduced in a few international markets, including Australia, Canada, and Belgium. They have already started rolling out in some markets on the West Coast and are now available in Los Angeles, Seattle, Portland, San Francisco, Sacramento, Phoenix, Las Vegas, Salt Lake City, Denver, Boise, Tucson, and surrounding cities. They will be available nationwide by 2024.

Softer buns? Meltier cheese? More sauce? My GOD! We live in amazing times. 🙂

Yes, I jest. Who really cares, right? Well, I do just a little: I own stock in McDonalds so I want the company to do well. But beyond that relatively insignificant detail, this iconic American company first rolled-out these amazing improvements in <GASP!> other countries! How could they?

Easily, because there really are amazing times, irrespective of even more sauce on the Big Mac.

Consider the following excerpt, courtesy of a recent report from the National Burea of Economic Research (‘NBER’):

The integration of countries and industries into global supply chains depends on cheap and efficient transport.

We show the evolution of transport use and costs over the last 55 years, and establish their implications for international trade and global supply chains. To set the stage, consider a concrete example: the change in the manufacture of telephones from a century ago to the present day.

Built in 1905, the Western Electric Hawthorne Works factory in the Chicago suburb of Cicero, Illinois, manufactured 43,000 varieties of telephone apparatus for the parent Bell telephone monopoly. It employed 40,000 people who worked in over 100 buildings. Even with a transcontinental railroad system, transport costs were substantial and excessive back-and-forth transport links were not common. As such, while this factory did source a few raw materials like Bakelite, rubber, and metal from remote locations, it manufactured many intermediate components internally — such as vacuum tubes in the early days and transistors later — before distributing finished telephone equipment across the country. This manufacturing complex effectively made handsets in a single location for the entire United States.

The factory operated until 1986, and large portions of the grounds were dynamited in 1994 to build a suburban shopping complex. In the age of globalization and low transport costs, a vertically integrated factory in a high-cost location no longer made financial sense.

The supply chain for the modern smartphone is quite different. The research and design activities for Apple’s iPhone take place in the United States, with further engineering in the United States and Taiwan.

Production directly involves 43 countries in six continents in addition to any further upstream manufacturers; key components are manufactured in Japan, Korea, Taiwan, and China, with final assembly in China and India. Apple’s direct subcontractors do not manufacture many of the components used and only assemble the final product before shipment around the world. With the exact mix depending on the model, components such as memory, microprocessors, optics, batteries, and screens are manufactured in both nearby Asian countries like South Korea, Taiwan, Japan, Malaysia, Vietnam, or even in the United States, Mexico, or European Union.

The supply chain for Apple’s iPhone is not unusual. In Samsung’s smartphone production process, design takes place in South Korea, manufacture of key components takes place in South Korea, Japan, and the United States, while the final assembly takes place in Korea, Vietnam, China, India, Brazil, and Indonesia. These locations are connected by frequent and reliable shipping networks. The expansive use of global networks by companies like Apple and Samsung is a function of declining transportation costs.

In 1890 it cost nearly $200 per ton to ship goods from California to Europe. A century later, the cost would be less than $2 per ton using a standard bulk ship.

Fascinating! Well to me, anyway. 🙂

Regardless of where that ‘best burger ever’ is consumed, the component parts — just like the iPhone — will originate from other places. Sure, the iPhone is far more complex to source, but you get my point. Here’s something that may surprise you: Have you ever heard of the U.S. ‘Defense Logistics Agency’? Early in the pandemic, the DLA took over the sourcing of hospital gowns from FEMA. This not long after India ordered their pharmaceutical industry to cease exporting 26 drugs and ingredients — most antibiotics — without explicit approval from the Indian government. As India provided about 1/5 of the globes ‘generic’ drugs at that time, this was a serious, and eye-opening, problem back in 2020.

US supply chains are now being rebuilt with redundant and diverse sourcing and ‘friendlier’ relationships, all with the intention of creating a more resilient, if not reliable, chain for mission-critical components and products. However, as you might imagine, any such supply chain will include higher-cost domestic manufacturers. This will be the longer-term source for stickier inflation in mission-critical products — like those that might fall under the DLAs purview.

For years to come, new supply chains for mission-critical products will be more expensive to operate, setting the stage for higher prices for products critical to maintaining health, commerce, security and infrastructure.

Ready for some good news?

For years, I’ve been concerned the future for US economic growth was dismal. Post-1971 and the decoupling of the US dollar and gold, America’s labor force replaced capital as the limiting factor governing GDP growth. Over the decades, immigration and automation helped stem the adverse impacts of declining American fertility, but still, US GDP growth rates faced serious headwinds.

So serious, for years I have opined that a real GDP growth rate exceeding 2% could not be sustained over longer term. I have changed my mind.

The pandemic accelerated the ‘remote work’ trend that had been slowing growing. Fast forward to 2023 and all of a sudden, to my eye, the ‘remote work’ phenomenon is no longer constrained by geographic borders. Sure, this trend has been developing for years — but now it’s on steroids.

Just as general material sources have popped up all over the world wherever local cost advantages appeared, the same seems to be happening with labor. And because technology and connectivity are no longer limitations, previous barriers that might have prevented ‘hiring’ a non-US laborer are falling away. No, not all … but many.

Think of this development as large-scale labor force growth from immigration — but without immigration!

The pandemic accelerated this shift. According to a survey by Upwork, 36.2 million Americans will be working remotely by 2025 — an 87% increase from pre-pandemic levels. And that’s just Americans. The growth outside our borders may be larger still.

I am personally aware of a number of US-based businesses that have outsourced some of their tasks or functions to other countries where labor costs are lower and talent pools are larger. Again, this type of outsourcing is not new, but the digital age has made it easier. According to a report by Statista, the pre-pandemic global outsourcing market size reached $92.5 billion by the end of 2019.

US companies are taking advantage of:

<-> Cost Reduction: Foreign outsourcing can help businesses save money on salaries, taxes, benefits, overheads, and infrastructure. For example, a software developer in the US earns an average of $107,510 per year, while a software developer in India earns an average of $6,291 per year, according to Payscale. Said another way, a US based company – in theory – can employ a software developer in India at 5.8% of the cost of a US employee. Actually, perhaps less: At present, the US company incurs no US payroll tax expense for this non-US employee.

<-> Access to Talent: Foreign outsourcing can help businesses access a larger and more diverse pool of skilled workers who can offer specialized expertise, creativity, and innovation. But frankly, the most meaningful word here might simply be the word “larger.” Because, essentially, given the significantly better fertility rates and population trends in many parts of Asia, this opportunity could be precisely the labor source many US businesses need, but cannot find here domestically.

<-> Scalability: This type of outsourcing can help businesses scale up or down according to their needs and demand. The difficulties associated with adding permanent staff are minimized.

The list goes on. This is happening, folks. And here’s the even better news!

The ‘global remote work’ phenomenon has the potential to be quite disinflationary, as the increased availability and far-lower cost of outsourced labor could generate large cost savings to many small, medium and large US companies.

Of course, there are a few challenges like quality control, cultural differences, time zone challenges, and increased technology security needs. But compared with the far greater challenge of finding local employees in a 3.5% unemployment-rate-marketplace, this could be just the development the US economy needs to soar. Not today, mind you, as we’re in the mists of a FED rate tightening cycle. But long term.

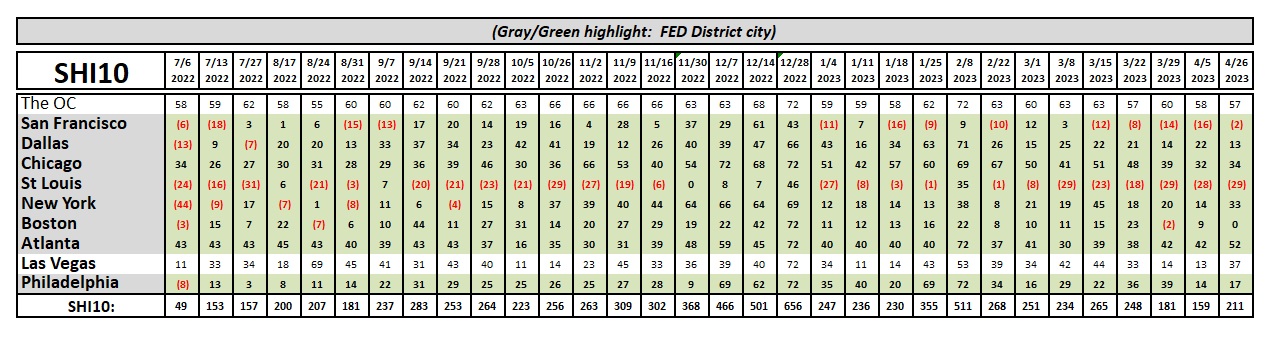

And while global labor force expansion may help McDonalds in their 100-plus countries, it doesn’t help our expensive eateries. No, enjoying a high-priced T-Bone at Mastros is a hyper-local phenomenon. Let’s see how the steakhouses are doing this week:

Better! All I have to do is go skiing for a couple of weeks and people head back to the steakhouses! 🙂

Well, a little anyway. This week’s SHI10 reading of 211 is a sizable improvement over the 4/5 reading. Good.

By the way, keep your eye on tomorrow’s ‘first’ GDP reading for Q1, 2023. The Atlanta Federal Reserve Bank’s GDPNow model forecast has fallen to only 1.1% — from about 3.5% earlier in the month. So this should be interesting … not only because of the trajectory, but the fact that a ‘positive’ reading of any size confirms the US economy continues to expand.

Also be sure to check out the ‘PCE Price Index’ to be released by the BEA on Friday the 28th. Recall this is the FEDs favorite and preferred inflation index. Both are sure to be market movers. As if we haven’t had enough of those lately. 🙂

<> Terry Liebman