SHI 4.5.23 — Big Macs and Knock-On Effects

SHI 3.29.23 — Reputation Lost

March 29, 2023

SHI 4.26.2023 — The Best Burger Ever?

April 26, 2023

Knock-on effects are those secondary or cumulative, down-stream effects triggered by current events.

For example, consider the SVB failure. That bank didn’t fail simply because management over-concentrated its deposit base with tech-savvy depositors, or the fact that a large portion of the deposits were ‘uninsured’ … or the fact that the bank carried a large ‘unrealized loss’ on their ultra-safe HTM securities portfolio. No, the bank failure really began a couple years before, even before the FED rapidly increased interest rates from zero to almost 5% in about 1 year — one of the most rapid rate increases in history. The SVB failure was a knock-on effect from the FED rate hikes.

“

The FED is breaking stuff.”

“

The FED is breaking stuff.”

And every time they do, we see additional knock-on effects, for example in housing, the stock markets, the CMBS market, investment real estate, and the list goes on. When the FED is trying hard to break things, we should all ask ourselves what other shoe might drop, so to speak.

Over the past few weeks, avid SHI readers have asked a couple of interesting questions. Remember, I have 6 avid readers! 🙂

The first concept is a little complex and wordy, so bear with me: “Can I ‘buy back’ my home-loan ‘note’ at a ‘discount’ from the bank that gave me the loan on my house … since interest rate increases have now reduced the value of that loan? Since the bank already has a ‘loss’ on their books, will the bank sell it to me for less than I owe on the loan?”

What an interesting question, right? The question is definitely factual. Assuming the home loan was made a couple years ago, say back when fixed rate loans were in the 2s, and assuming the bank kept the loan “on their books” and still holds it today, the question has merit. Unfortunately, the short answer is “no.”

The second is a bit easier: “After the FED tackles and tames inflation, will prices go down?”

Once again, the answer is a resounding ‘no.’

I explain both answers in more detail below, and you’ll be pleased to hear the Big Mac will be offering us a helping hand! Well, maybe not a hand … but you know what I mean. 🙂

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. Even as the FED rapidly raises rates! At the end of Q4, 2022, in ‘current-dollar’ terms, US annual economic output rose to an annualized rate of $26.14 trillion. During 2022, America’s current-dollar GDP increased at an annualized rate exceeding 9%. No wonder the FED is so concerned, right? The world’s annual GDP rose to over $100 trillion during 2022. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the 3 big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

The simple fact is that no human is required to buy or consume a Big Mac.

Or eat out at any restaurant, for that matter. But humans do both. Often, as it turns out.

Is the Big Mac cheaper … have prices declined … thereby inspiring price-sensitive consumers to consume even more Big Macs? And are restaurant prices falling, thereby triggering the knock-on effect of increased demand and patronage?

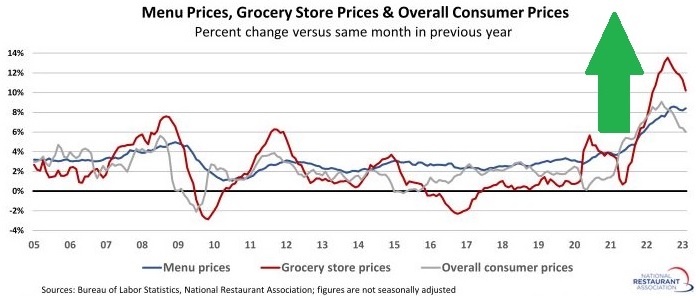

Nope. Quite the opposite. ‘Menu prices’ are way up, according to the National Restaurant Association:

Menu and grocery store prices haven’t increased at this rate in decades. And yet, restaurant ‘traffic’ continues to rise. In the aggregate, restaurants are busier than ever.

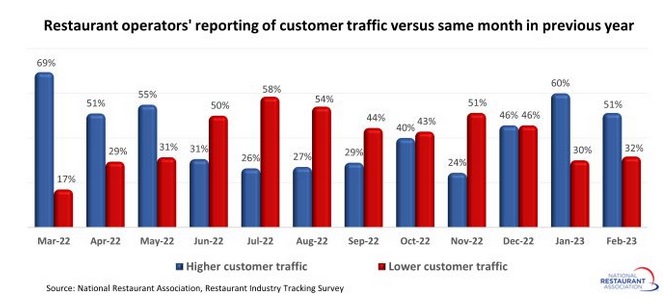

According the the NRA (not that one … the other NRA), restaurant operators reported a net increase in same-store sales for the seventh consecutive month. 73% of operators said their ‘same-store sales’ rose between February 2022 and February 2023, according to the National Restaurant Association’s monthly tracking survey. Only 12% of operators said their sales were lower in February, down from 23% who reported a sales decline in January:

So, to summarize: In general, all prices are significantly higher. And yet, demand is higher, too. Hmmm …

Economically speaking, this is very odd.

Economists have studied the relationship between price and demand for centuries. Historically, when the price of ‘a thing’ rises, demand tended to fall off. Why? It’s pretty simple, really. As a price rises, we all generally react in the same way: Often we will seek a better-priced substitute — similar in quality and “utility” — but cheaper. If the price or cost of “product A” increases dramatically, consumers tend to find “product B” that has similar features but costs less. Makes sense right? Then why isn’t this happening here? Why are restaurants still packed even as menu prices rise thru the roof?

Because the price of those alternatives is also thru the roof. “Substitution” is difficult right now. And there are numerous other variables at work here today: Consumers are still “flush” with cash … unemployment rates are still at all time lows … and, as we all know, grocery stores are not much better. Finally, notwithstanding the fact that the FED is working very hard to “break” the consumer’s spirit with their rate hikes, so far they’ve only managed to break the residential mortgage and home business, and to put a serious tweak into bank balance sheets. Other knock-on effects, I’m sure, are also developing right now. Will they become overly problematic? It’s hard to tell and even harder to predict. But I digress.

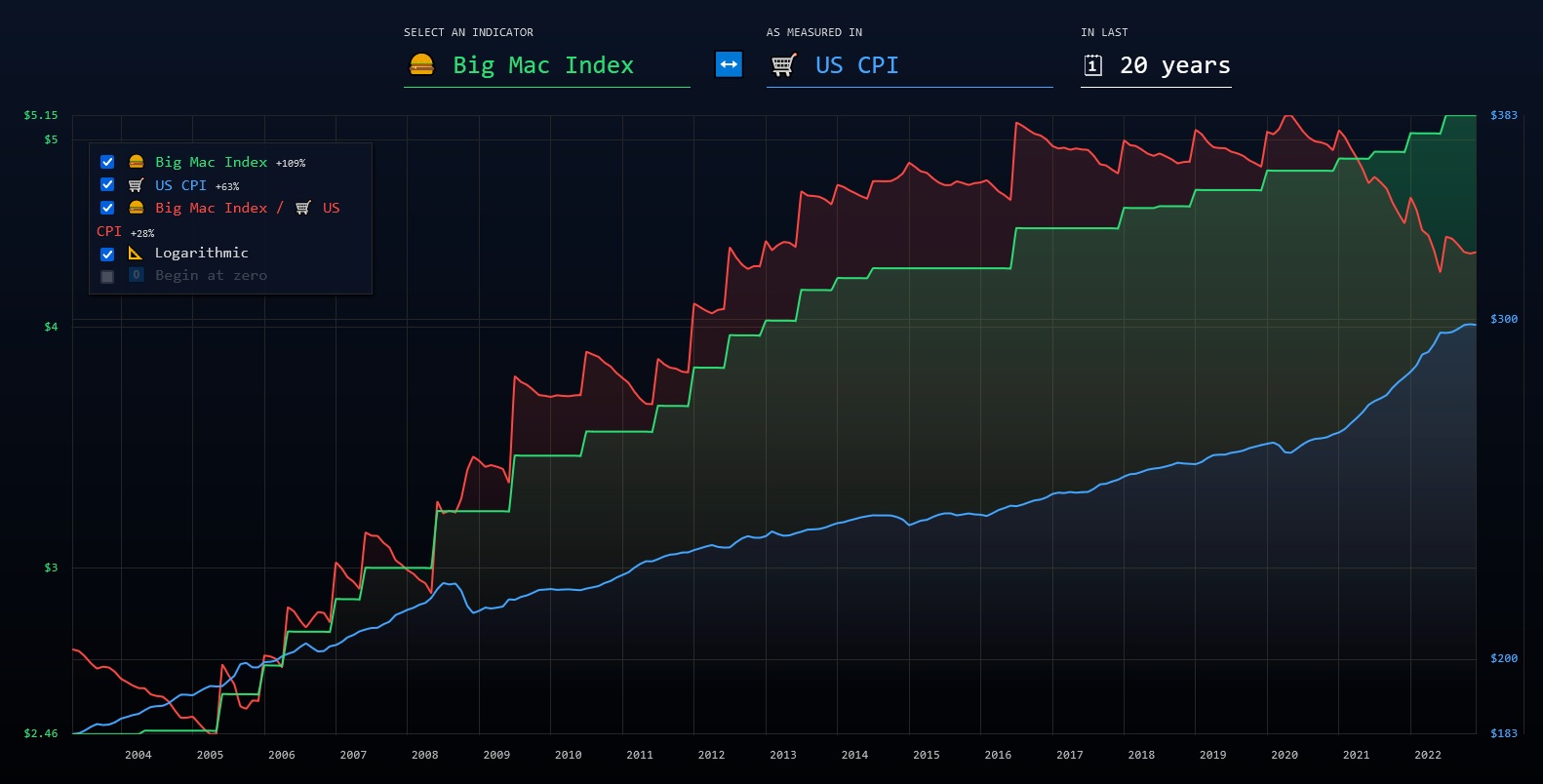

No, unfortunately for all of us living in this post-pandemic, post-Ukrainian invasion, post-massive fiscal stimulus world, prices of most things are up. And if history is a accurate barometer, they are not likely to go down any time soon. Consider the data from this historic, 20-year chart:

The green line tracks the 20-year movement in the price of the Big Mac index. This price is reflected on the “left-hand-side” of the chart. The blue line tracks the 20-year history of the US CPI. This movement is reflected on the “right-hand-side” of the chart. Let’s call the “Big Mac Index” the BMI for short. And this acronym is rather fitting: If you eat too many Big Macs, your personal BMI will skyrocket! 🙂

During the past 20-years, the chart suggests the CPI has increased by 63%. Concurrently, the BMI increased by 109%. The red line measures the relative relationship between the two. Beginning in 2021, for the first time in 20-years, the CPI increased at a percentage rate faster than the price of a Big Mac. Don’t worry: Knowing McDonalds as I do, I suspect this will change in the not too distant future. Big Mac prices are heading up.

So, to repeat, the red line fell beginning in 2021 is because the CPI increased at a faster rate than the Big Mac Index beginning at that time.

And herein lies the point: During the 18 prior years, both the CPI and the Big Mac increased year after year after year. Inflation is now a modern phenomenon — even when interest rates are super low and the FED expresses concern that inflation, too, is too low.

Inflation is now a structural component of the global economy.

It is a consistent, ever-present condition that will not moderate or go away.

And this is the simple reason why you can’t hold on to cash in your bank account over the long term. Even if your bank remains perfectly healthy, and your deposits are “safe,” your cash in the bank is losing value. When compared to the cost of things, that is. The CPI tells us that 20 years ago, “stuff” cost 63% less. If you kept a dollar in a bank for the past 20 years, today that dollar can only buy about 40 cents worth of stuff. That’s a huge value loss.

Of course, the Economist magazine’s original Big Mac Index is more of a FX (foreign exchange) tool, using the Big Mac as a metric to evaluate currency value relationships. For example, a Big Mac costs £3.79 in Britain and US$5.36 in the United States. The implied exchange rate is 0.71. The difference between this and the actual exchange rate, 0.81, suggests the British pound is 12.9% undervalued. But whether the pound is undervalued or not, the one thing I can guarantee is that a British Big Mac costs a whole lot more today than it did 20 years ago.

So, back to the original question: “After the FED tackles and tames inflation, will prices go down?”

No. They won’t. The cost of all things will continue to rise over time. Decade after decade, costs will increase. My opinion, of course, but a high-conviction opinion.

Let’s move to question 2: Can you buy back your home loan from your lender? Again, as I said above, no. Why not you ask? Well, there are two likely answers. First, your bank probably doesn’t own your loan. They probably sold it to Fannie Mae, Freddie Mac, or some other, similar private company that securitizes home mortgages. But even if they did keep the loan on their books, it is doubtful they have a desire to take an actual loss on your loan. Sure that loan is “worth less” that the loan amount today because interest rates are higher, but the bank is holding it as a “hold to maturity” asset and that’s what they intend to do. Sorry.

Shall we head to the steakhouses?

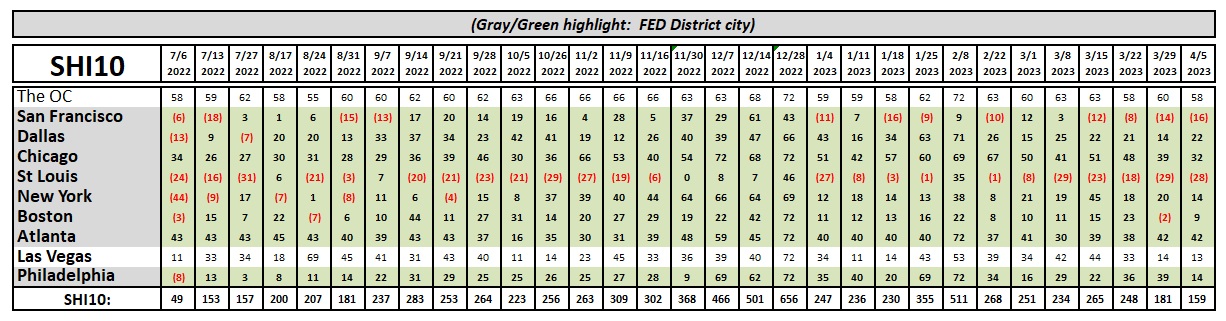

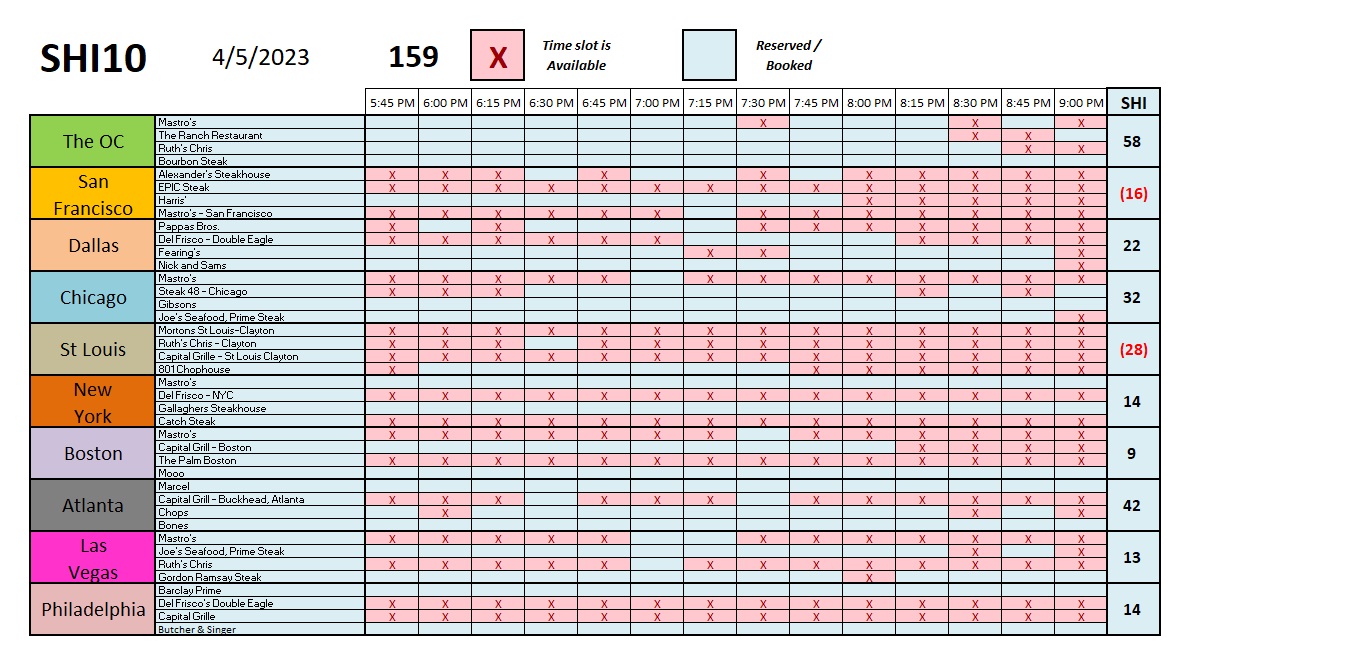

This week the SHI10 has fallen again. We’re now at levels unseen since July of 2022.

To my eye, the SHI10 definitely shows signs of decelerating. Below is the individual restaurant chart. Take a look because you’ll see something you have not seen in quite a while: A 7:30 pm ‘open table for 4’ at Mastros Ocean Club in Corona del Mar! And an 8:00 pm opening at Gordon Ramsey’s place in ‘Vegas! Wow … this is unusual!

But some amount of demand deceleration might not be a bad thing, frankly. Let me highlight something that may have been lost in all the noise from the “experts” that continue to predict a US recession.

In the aggregate, America’s 2022 ‘nominal’ GDP finished the year at just under $25.5 trillion. That number clocked in at $23.3 trillion for 2021. Doing the math, our current-dollar GDP increased by over 9% in 2022. Staggering. Let me repeat that:

In 2022, nominal GDP increased by over 9%.

This is why a some deceleration might be a good thing, and perhaps this is why the FED is working so hard to break things. The recent SHI10 suggests they might finally be chipping away at the consumer’s resolve to SPEND, SPEND, SPEND! We’ll continue to watch closely.

But not too closely … there will be no blog next Wednesday. Instead, I’ll be closely examining the ski slopes of Park City. Someone has to. May as well be me. 🙂

–> Terry Liebman