SHI 3.29.23 — Reputation Lost

SHI 3.22.23 — How Safe is YOUR Bank?

March 22, 2023

SHI 4.5.23 — Big Macs and Knock-On Effects

April 5, 2023

A sterling reputation can be lost in the briefest of moments. Just ask Will Smith.

Sometimes the cause is clear and obvious. A vicious slap. A racist slur caught on film. An unprovoked military attack on a peaceful, neighboring nation.

But other times, I’m left scratching my head to find a reason for reputation loss. And since this is an economics and finance blog, and not a social commentary, today I’m talking about First Republic Bank and their very-public fall from grace.

“

What is a reputation worth?”

“

What is a reputation worth?”

Quite a bit. One year ago, First Republic Bank (“FRC“) common stock was trading at about $170 per share. Today it trades closer to $14 per share — a decline of more than 91%. Inasmuch as there are 182 million shares outstanding, simple math suggests the value of a reputation lost in this case is about $28 billion.

What unbelievably egregious offense did FRC commit to lose depositor and investor trust and trigger this staggering loss? What a great question.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. At the end of Q3, 2022, in ‘current-dollar’ terms, US annual economic output rose to $25.74 trillion. Thru Q3, America’s current-dollar GDP has increased at an annualized rate exceeding 7%. The world’s annual GDP rose to over $100 trillion during 2022. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the 3 big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

On February 7th, 2023, First Republic Bank (“FRB”) filed an “Form 8K” with the FDIC.

That filing disclosed the sale of additional shares of FRB common stock. The offering was underwritten by BofA Securities, J.P. Morgan Securities, Goldman Sachs and Morgan Stanley. The new FRB common stock sold at $138.24 per share, generating close to $400 million in proceeds to First Republic Bank.

https://ir.firstrepublic.com/static-files/8b9b53ef-08f6-432e-8313-5c7e56990430

Less than 2 months later, the common stock was trading at 1/10th that amount. That $400 million of stock became worth about $40 million. What happened?

That is precisely the question I asked the new ‘Microsoft Bing’ artificial intelligence search engine. Microsoft calls this engine “Your AI-powered copilot for the web.” As I had not used this tool before, I asked a friend for a bit of guidance. Finally finding my way to the ‘launch pad,’ I posed this request of the AI engine:

“compare first republic bank in February to its status today”

I asked the AI system to reply in a “professional” tone and to write a “blog post.” Here’s an exact replica of what I got in response:

First Republic Bank: A Tale of Two Quarters

First Republic Bank is a commercial bank and provider of wealth management services headquartered in San Francisco. It caters to high-net-worth individuals and operates 93 offices in 11 states primarily in New York, California, Massachusetts, and Florida. In this blog post, we will compare the bank’s performance in February 2023 to its current status in March 2023, and analyze the factors that led to its dramatic decline.

In February 2023, First Republic Bank was enjoying a strong financial position and a solid reputation among its clients and peers. The bank reported a net income of $1.2 billion for the fourth quarter of 2022, an increase of 15% from the same period in 2021. The bank also boasted a high-quality loan portfolio, a robust capital base, and a loyal customer base. The bank’s stock price was trading at $180 per share, reflecting its growth potential and stability.

However, things took a turn for the worse in March 2023, when the bank became the latest victim of the financial crisis that had already claimed two of the largest banks in the country. The bank faced a sudden and massive withdrawal of deposits from its large corporate and institutional clients, who feared that the bank would not be able to withstand the market turmoil. The bank’s liquidity position deteriorated rapidly, forcing it to seek emergency funding from the Federal Reserve Bank and JPMorgan Chase & Co. The bank’s stock price plunged to $23 per share, a drop of 87% in two weeks.

The main reason for the bank’s downfall was its over-reliance on uninsured deposits from America’s largest banks. These deposits accounted for $30 billion of the bank’s total deposits of $212 billion at the end of 2022. These deposits were not covered by the Federal Deposit Insurance Corporation (FDIC), which guarantees up to $250,000 per depositor per insured bank. When the financial crisis hit, these large depositors panicked and withdrew their funds en masse, leaving the bank with a liquidity crunch.

The bank’s management tried to reassure its customers and investors that it had sufficient liquidity and capital to meet its obligations. The bank also announced that it had secured additional funding from the Federal Reserve Bank and JPMorgan Chase & Co., as well as access to other sources of liquidity such as asset sales and secured borrowings. However, these measures were not enough to restore confidence in the bank’s solvency and viability.

The future of First Republic Bank is uncertain at this point. The bank may be able to survive the crisis if it can retain its core customers, stabilize its liquidity position, and restore its profitability. Alternatively, the bank may be forced to merge with another financial institution or be taken over by regulators if it fails to meet its obligations or comply with regulatory requirements. In any case, the bank’s shareholders are likely to suffer significant losses.

First Republic Bank’s story is a cautionary tale for other banks that rely heavily on uninsured deposits from large institutions. These deposits may seem attractive because they offer higher interest rates and lower costs than insured deposits. However, they also expose banks to higher risks of liquidity shocks and runs. Banks should diversify their funding sources and maintain adequate liquidity buffers to cope with unexpected events. Banks should also communicate clearly and transparently with their stakeholders to maintain trust and confidence.

Fascinating. You have to love the title of the AI blog! The darn machine writes better than I do! 🙂

“The main reason for the bank’s downfall…” according to the AI-engine at Microsoft Bing was the bank’s “over-reliance on uninsured deposits….”

Can computers have opinions? I guess … because that’s precisely what this is. A computer’s opinion.

I’m not sure I agree. I think the cause is more complex than that, as I’ve discussed in prior blogs. But I have heard and read that suggestion numerous times, so I suspect that’s where ‘Mr. Bing’ found the ‘data’ to form his opinion in the blog.

I do find it interesting the AI-engine used words like “panicked” … “trust” … and “confidence.” And I feel some of the computer’s statements are inaccurate, such as “These deposits may seem attractive because they offer higher interest rates and lower costs than insured deposits.” I’m not sure what that means. Large deposits are attractive to banks because they are large, allowing the bank to grow and scale quicker.

The AI-engine suggestion that First Republic was “… the latest victim of the financial crisis” is accurate. But why has FRC been more severely injured by this crisis than many other banks, in very similar circumstances? I’m mystified.

The FED rate hikes have similarly affected all bank HTM mortgages, MBS, and Treasuries. All have lost “paper” value. It appears to me that all banks across America engaged in the similar practices, taking similar risks, with the only obvious difference being the size of their investment in illiquid, long-duration assets. So why has FRC become the poster-child for this bank run? Why have they lost the trust of their depositors? Why have investors lost confidence in the bank when about 45 days ago they paid 10X more per share for the same bank stock? What is fundamentally different today than it was on February 7th?

I struggle to offer a meaningful answer. To my eyes, other than customer and market perception, nothing has fundamentally changed.

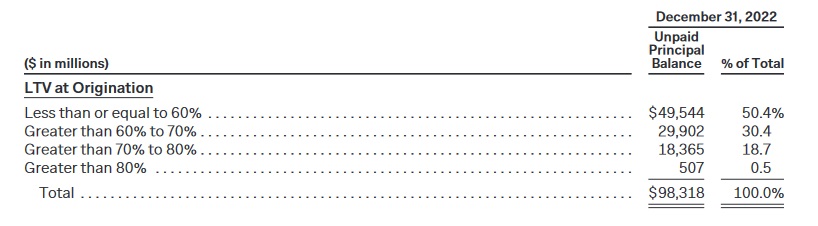

FRC invested quite a bit of their deposits into ultra-safe home mortgages. As of the end of 2022, they held almost $99 billion of ‘Single family’ mortgage loans. Were these “risky” home loans? You decide. Here is a chart of the ‘loan-to-value’ for all the loans at the time of origination:

More than 1/2 were made at 60% LTV or lower.

On February 7th, 2023, some of the biggest banks in the US felt First Republic’s investments were safe and sound, and were happy to participate in the stock sale and capital raise. So what changed?

Nothing. Nothing, of course, except the lost confidence trumpeted almost daily in the media and obvious in the bank’s common stock price. This is a bank run, folks. Fueled by emotion, innuendo, fear and anxiety, mob mentality takes over and logic and objectivity are nowhere to be found. And for reasons lost on me, the bank’s hard-earned reputation has thus been lost. Will they regain it?

Perhaps. But that clearly isn’t easy. I have no doubt Mr. Smith would agree. Once a reputation is fractured, it does not mend quickly. Regardless of the cause.

Our entire entire banking system remains under a cloud of fear and distrust today. Again, nothing has fundamentally changed. But the systemic challenges go far beyond the pain at First Republic. Confidence has taken a hit … and reputations are damaged. I have no doubt the folks over at the FDIC are kicking around ideas for a long term fix. Perhaps they should hire IntraFi to do the job?

What is Intrafi? While they have been around for 20 years, I was unaware of their existence until last week. My thanks to the SHI reader who brought this to my attention:

https://www.intrafinetworkdeposits.com/about/intrafi-network-overview/

Thru that network, an individual or company can theoretically protect up to $100 million deposited into a single bank. The model looks very intelligent. Take a look.

Some media outlets now suggest the next big shoe-to-drop will be commercial real estate mortgages. Are they right? Well, when we combine the Covid-pandemic disruptions with a 5% FED rate hike, there’s no telling where the systemic cracks will appear. Like Elvis, ‘normalcy’ has ‘left the building.’ And there can be no doubt, bone-jarring hits like these are not good for the American economy. The economic effects will reveal themselves in time … but rest assured we will see significantly less commercial real estate and business lending in the immediate future — much as we have seen significantly less new capital in the technology space. These ingredients do not make for a robust economic soup. On the other hand, there’s still a lot of stimulus left over from the pandemic largess to counter the current credit and capital contractions.

Does this mean recession odds are higher? Yes. But it’s worth remembering our economy has really defied the naysayers so far this year. In fact, about one week ago, the Atlanta FEDs ‘GDPNow‘ model estimated real GDP growth in the first quarter of 2023 at 3.2%. That is a staggeringly high number given the headwinds. Time will tell. Let’s head to the steakhouses.

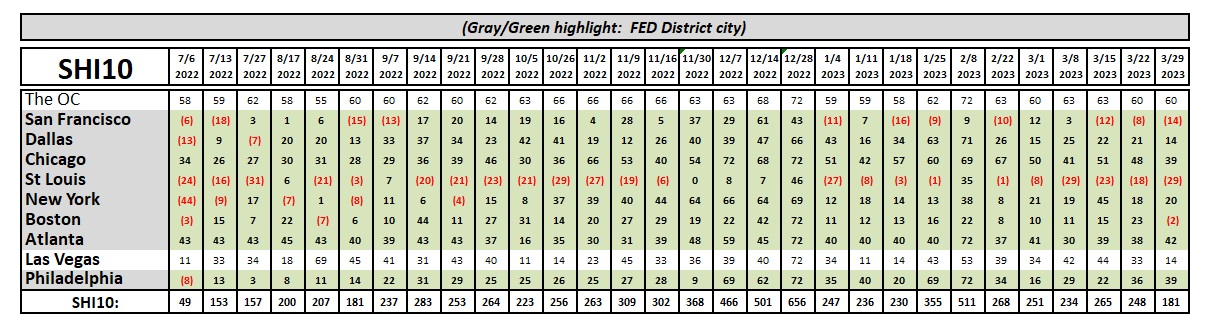

Well, this chart shows the lowest SHI10 score we’ve seen since August of 2022. Reservation demand was weaker in 6 of our 10 SHI markets this week. One week does not make a trend … but in light of all the economic noise out there, I’m a little concerned. Slightly. Let’s see what next week brings.

<:>-<:> Terry Liebman