SHI 3.8.23 — Snail Tracks

SHI 3.1.23 — Home Values and Inflation

March 1, 2023

SHI 3.15.23 — Bank Panic!

March 15, 2023

On a foggy morning, it’s easy to see where your garden snails have been and where they are going. They leave tracks.

And while the image above resembles movement of a large snail herd over time, it will come as no surprise to my long-time readers that this economic blog rarely discusses gardening issues. Rest assured, those are not snail tracks. No, forecasting the path of a garden snail would be easier.

“

‘Federal Funds’ futures are unpredictable.”

“

‘Federal Funds’ futures are unpredictable.”

The experts making these predictions are often wrong. Why is this so difficult forecast? It’s a great question … and it ‘tees up’ today’s blog.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. At the end of Q3, 2022, in ‘current-dollar’ terms, US annual economic output rose to $25.74 trillion. Thru Q3, America’s current-dollar GDP has increased at an annualized rate exceeding 7%. The world’s annual GDP rose to over $100 trillion during 2022. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the 3 big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

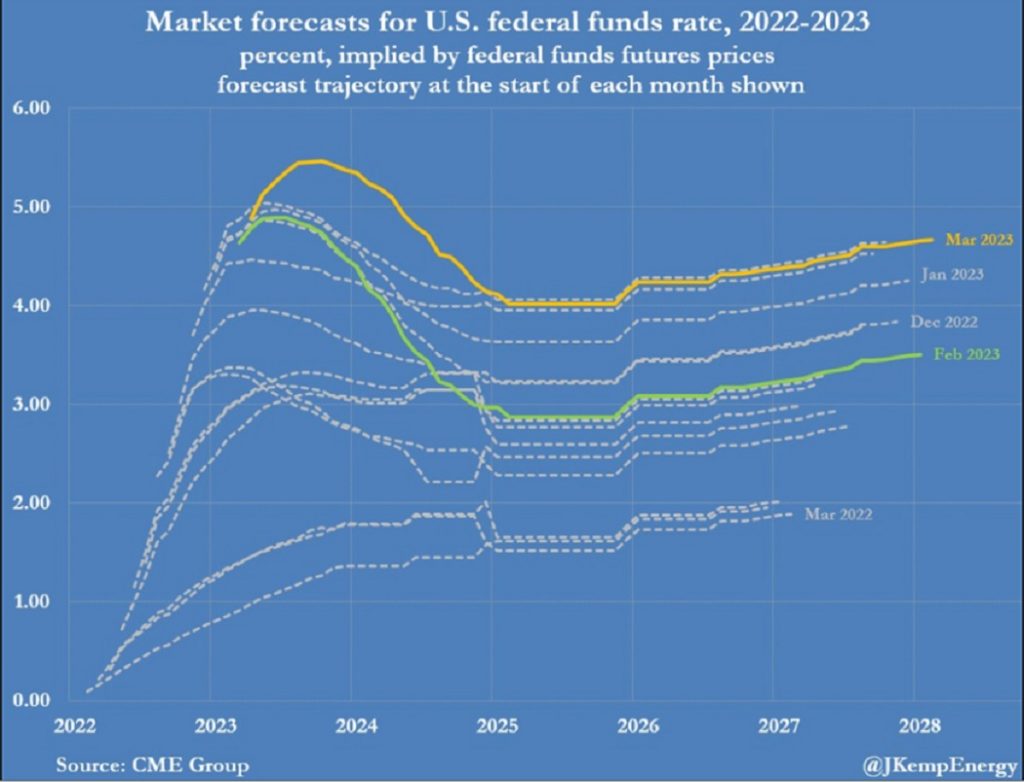

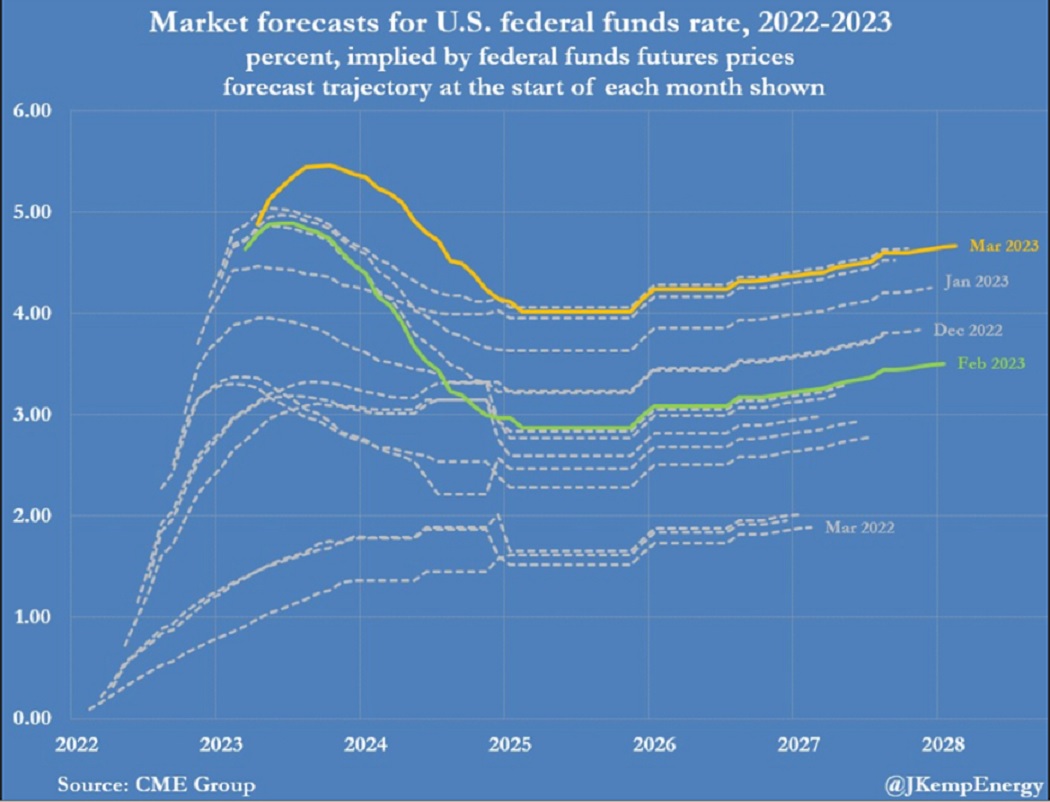

Here is a more complete image of the snails crawling thru our economic garden:

The ‘header’ of the graphic is self-explanatory. Each snail track above represents the expected future interest rate “level” of FED funds at the beginning of the month shown.

Low at the bottom of the image, we see the expected path for the FED funds rate, as of March of 2022, forecasted six years into the future. Remember that it wasn’t until May 5th of last year — about 1 year ago — that the FED increased the federal funds rate by 0.5%, the first rate pump in the current tightening cycle. Next, look at the four (4) dates on the right side of the image. December, January, February and March. Note how the “futures” predicted a far lower FED funds rate when February began? Now, as March of 2023 begins, the futures markets at the Chicago Mercantile Exchange (CME) now expect the funds rate to stay quite high for quite a long time.

Over the past couple of days, Chairman Powell confirmed that “higher and longer” is the FEDs expectation. But for the next 6 years? No. The only comment I can make with a high degree of confidence is that the futures markets are wrong. In my opinion, there is no way the FED funds rate will remain above 4% for the next 6 years.

Of course, I could be wrong, too. If inflation proves to be far stickier than transitory, then, sure, short term rates could remain high for years. I simply don’t expect that to happen. I remain firmly in the “transitory” camp — however, unlike the FED and the media, I define transitory as maybe a year or two. But once again I have to throw out a caveat: If the federal government continues to run deficits, print and spend money like the proverbial drunken sailor, all bets are off. I may not be a monetarist disciple, true-believer in all of Milton Friedman’s theories, but I do believe America’s recent experiences with fiscal over-stimulus, M2 growth, and inflation have undeniably proven that MMT is absolutely flawed and inherently inflationary. When M2 expands at a rate far beyond the nominal GDP growth rate, as it did in the past 2 years, we have learned once again that inflation will spike uncontrollably. This lesson is clear.

But does the current bout of FED rate increases guarantee a recession is around the corner? Is a recession as inevitable as the experts suggest?

Back in July, according to CNBC, 63% of the economic experts surveyed believed the US would be “in a recession” within a year. And most believed US GDP would begin to contract by December. Well, that didn’t happen.

And this survey took place in July of 2022 when the experts felt the FED funds rate would top off around 3.8% by March of 2023. Right about now, in fact. Well, that didn’t happen either.

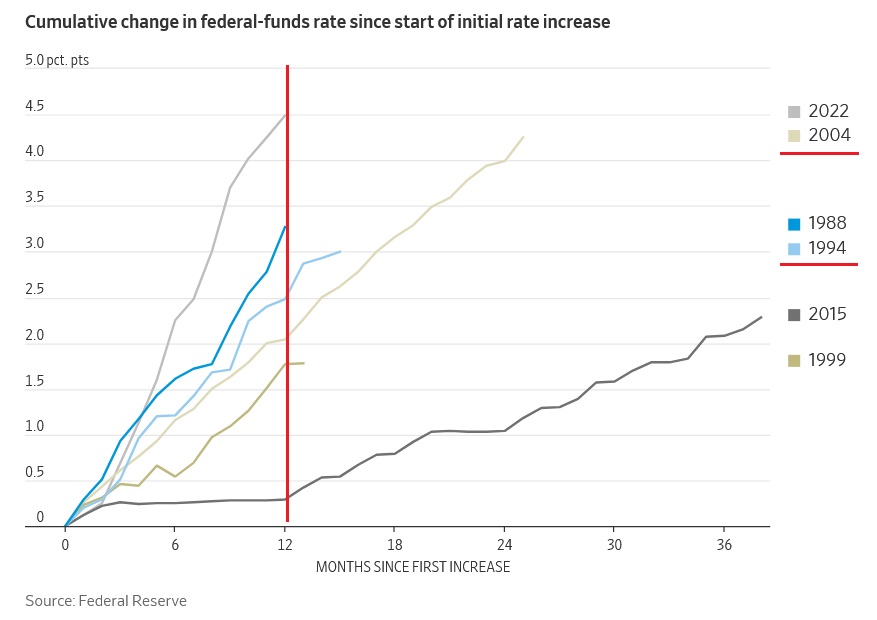

No, the FED blew right thru 3.8% and as I write this blog, the FED funds rate is at 4.75% — almost a full percentage point higher. And Powell assures us more rate increases are coming soon. The current rate-hike cycle, in fact, is one of the fastest in history:

I added the red lines. Notice the “MONTHS SINCE FIRST INCREASE” on the bottom axis.

The speed of the 2022 hikes is the fastest in recent history. The FED matched this speed in March of 1998, but that terminal increase was a little lower. In 2004, the FED raised more than 4% from the start, but the increases came over about 2 years.

Did each of these rate increase cycles trigger a recession, as the economic experts would have us believe?

No. The increase cycle in 1994 did not trigger a recession. A recession did follow the 1999 hike-cycle, but I would argue the rate hikes did not trigger it. No, it was triggered by the “dot-com” crash. Now, I would argue the FED rate hikes probably caused the crash, so one could argue the FED rate-hikes tangentially caused the 2001 recession. That seems right. I would also argue the 2004 increase-cycle did not, in itself, trigger a recession; however, the “Great 2008 Recession” did follow shortly thereafter. But I don’t believe the two events have a causal relationship. The 2015 hike-cycle did not trigger a recession. Fortunately.

So, clearly FED rate hikes cause financial stress. Which might lead to a recession. But the relationship is tenuous at best.

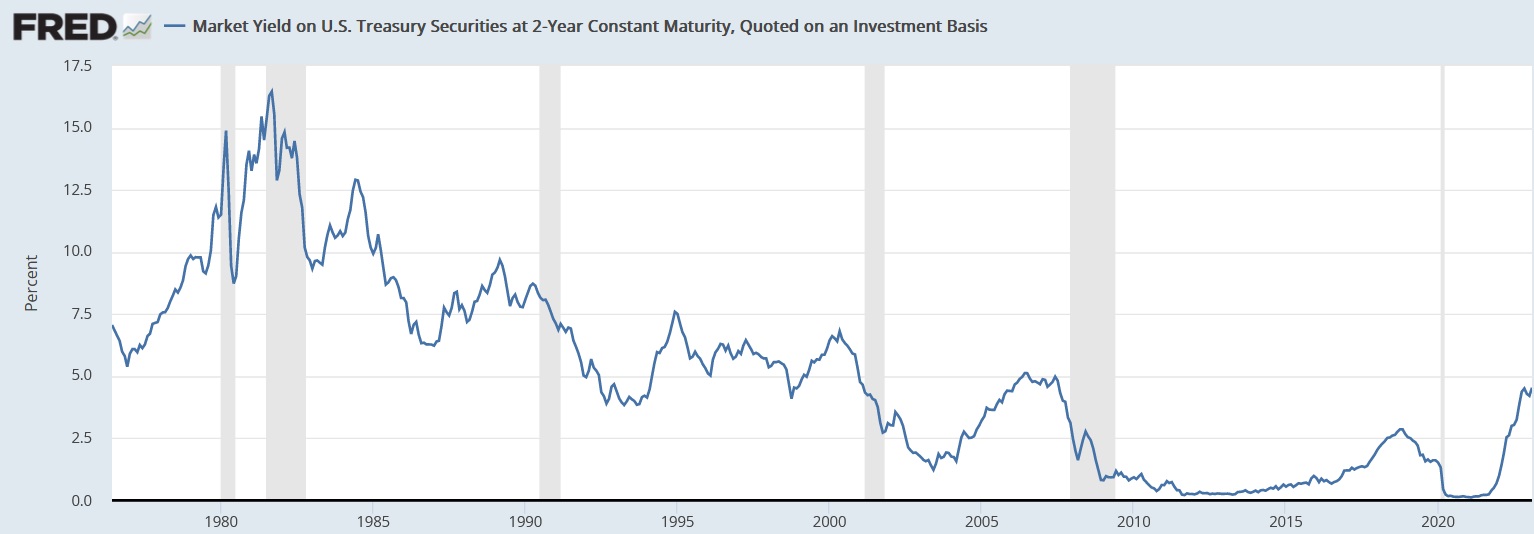

Recessions are notoriously hard to predict. But if the FED raises rates high enough, the US will enter a recession. How high is “high enough?” Many are suggesting our massively-inverted yield curve almost guarantees a near term recession. As I write this blog, the 2-year Treasury has passed thru and above 5% for the first time in decades. Is that high enough?

Probably not. Because as we see below, for many years in the past, the 2-year Treasury was far above 5%.

So while a 5% rate on the 2-year Treasury is an awesome place to park your “intermediate term” cash, it is far below the highest 2-year we’ve ever experienced.

Also, it’s important to consider the level of the FED funds rate at the moment the increase cycle began. For example, the 1988 super-fast increase-cycle began when the funds rate was around 6.5%. Lifting that rate to almost 10% in less than a year definitely triggered a recession. In January of 1994, when that FED hike-cycle began, the federal funds rate was already around 3% … and it peaked around 6%. No recession followed.

Here’s today’s take away: The current rate hike-cycle began with the federal funds rate near zero. Now we’re close to 5%. And the FED assures us they aren’t yet done raising rates. Assuming they finish this cycle at or below 6.25%, I will opine that recession odds are about 50/50. Above that rate, recession odds increase dramatically. And if they go above 7% … look out below. The economy will contract.

But gravity isn’t only a rule in physics. It’s a rule in finance, too. The higher the FED lifts rates, the stronger the “financial” gravitational pull to drag them back down.

To repeat, it’s entirely likely that a recession is already inevitable. Many experts suggest FED rate increases to date have already assured us of that future. Perhaps, but I disagree. However, rest assured there is a level of interest rates that would guarantee a long and deep recession. For example, imagine if the FED were to raise rates to 20% at their next FOMC meeting. That would certainly guarantee a recession. And a stock market collapse. And all kinds of other bad things.

But they won’t. They cannot. The FED is bound by very real behavioral constraints. Think of bumpers on a bowling alley that prevent a ball from falling into the gutter. They will likely raise rates again, but their increases will be measured and thoughtful. But even under such a regime, there is a rate level above which the economy is likely to tip into a recession. Time will tell.

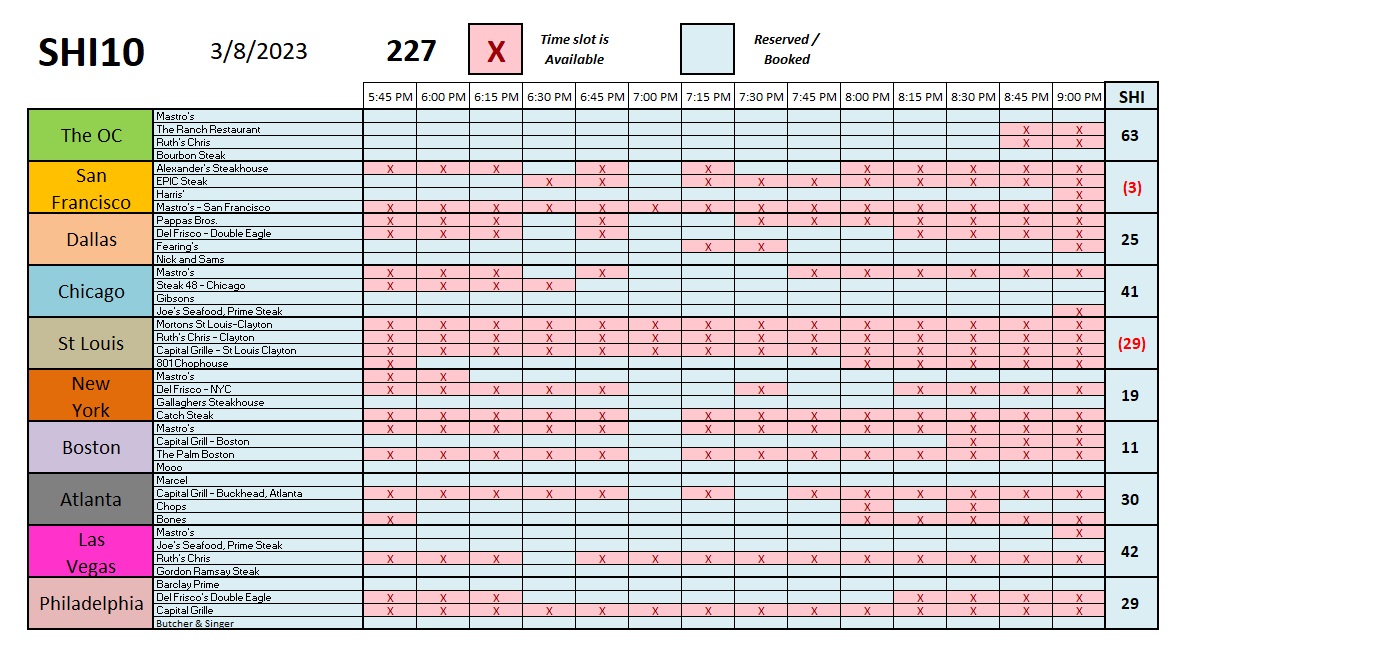

Let’s head over to the steakhouses.

Not much has changed this week … perhaps we see a slight dip in reservation demand. But very slight.

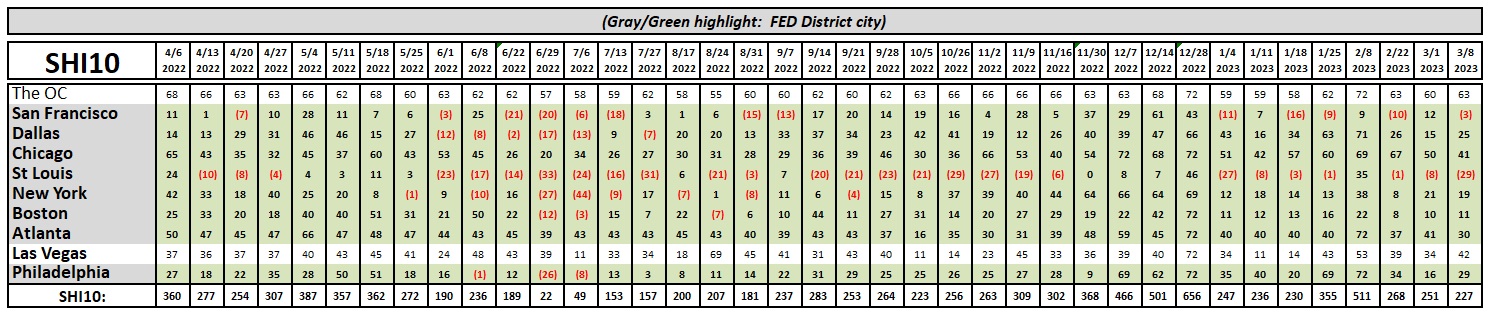

Week over week, and month over month, demand for these expensive eateries is holding up quite well. Better, frankly, that I expected. Media jawboning has been so overwhelmingly gloom and doom economically speaking, I’m actually a bit surprised we haven’t seen more of a pull back. Apparently, the upper crust still has plenty of money to spend on expensive steaks. Here’s the week-over-week trend report:

Thanks for tuning in.

<:> Terry Liebman