SHI 3.15.23 — Bank Panic!

SHI 3.8.23 — Snail Tracks

March 8, 2023

SHI 3.22.23 — How Safe is YOUR Bank?

March 22, 2023

Bank Panic: Rates, Runs, Failures and Other Unintended Consequences

I think that’s a better name for today’s blog. 🙂

Bank panics are nothing new. In the words of the FED:

“The Panic of 1907 took place over one hundred years ago, before the establishment of the Federal Reserve System, the Federal Deposit Insurance Corporation, or the Securities and Exchange Commission — institutions designed to bring stability to banking and financial markets.”

Stability? Really? Today? Well, this is certainly debatable … but thru my eyes, the 2022 rate hikes from that very same Federal Reserve brought anything but stability to our financial markets. In fact, I would argue, they broke it. Perhaps not the entire banking system; but, they certainly “broke the bank” and not in a good way.

(Here’s a link to a bit of history … if you’re interested https://www.federalreservehistory.org/essays/panic-of-1907 )

“

Globally, economic cracks are showing.”

“

Globally, economic cracks are showing.”

The word “bank” and the word “run” are both perfectly harmless as long as they are not paired together. But put them side-by-side and you get “bank run.” The scariest phrase ever heard by a bank CEO. Have you seen the movie “It’s a wonderful Life”? Great film from about 70 years ago, starring Jimmy Stewart as “the banker.” This is what a bank run looked like decades ago (right click, open in new tab):

https://www.youtube.com/watch?v=2GDlioFhoAk

Silicon Valley Bank failed exceptionally quickly, by historic standards. Usually, it takes a fair amount of time for a bank to die and vanish. Usually, the slide is measured in years, or at the minimum, months. But Silicon Valley Bank failed in 1 week.

I can easily argue that a week before their failure, they were a thriving, successful, 40-year old, $200+ billion institution. Like most opinions, this one is only partially true in fact, but there’s a lot of truth in that statement. By many measures, this was a very successful bank. Until it broke. And it broke fast. Did the FED break it? Or is there plenty of blame to go around?

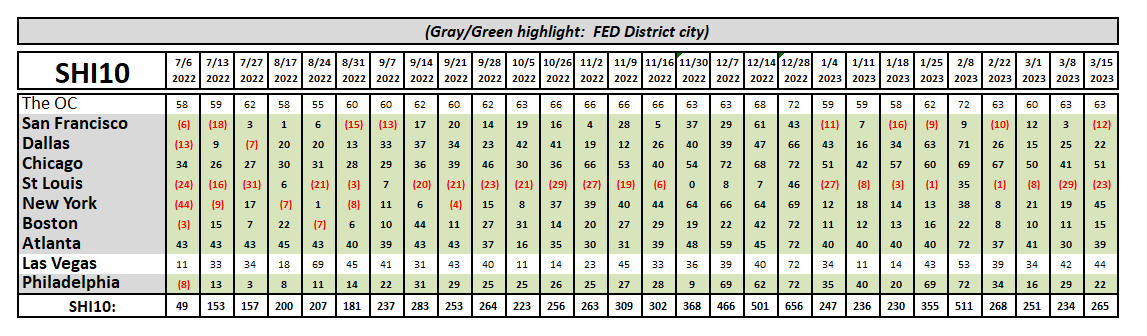

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. At the end of Q3, 2022, in ‘current-dollar’ terms, US annual economic output rose to $25.74 trillion. Thru Q3, America’s current-dollar GDP has increased at an annualized rate exceeding 7%. The world’s annual GDP rose to over $100 trillion during 2022. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the 3 big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

There is plenty of blame to spread around on this one. Super–speedy FED rate-hikes were the catalyst, but in my opinion SVB’s management and investment decisions leading up to the bank failure were poor at best. And finally something broke. Sure, the “snap” itself was a few years in the making, but without the exceptionally fast 2022 rate hikes from the FED, it’s quite likely SVB would not have failed, further triggering the systemic bank panic we’re seeing today.

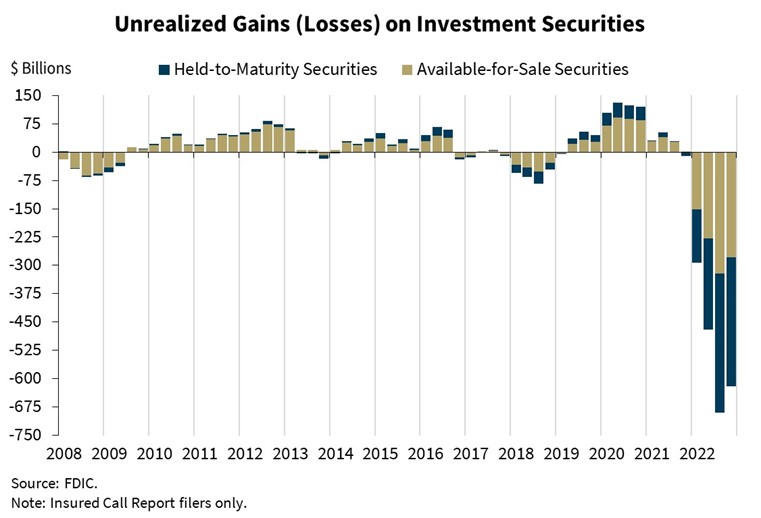

The story, my friends, like many stories, starts with a bit of history. For years, banks carried relatively small gains or losses from “Investment Securities” on their books. Investment securities are most commonly US Treasuries and, to a smaller degree, ‘mortgage backed securities’ — both rather conservative investments. But when the FED began their fastest rate hike in recent history, things changed. All banks, in the aggregate, began to realize large “mark to market” losses on their balance sheets. I talked about this extensively in my first 2023 blog:

https://steakhouseindex.com/shi-1-5-23-jobs-jobs-jobs-and-money/

The data in that January blog highlighted Q3 of 2022. I can now show that same graphic from Q4 of 2022:

In Q4, as interest rates moderated, bank losses declined, to the benefit of all banks.

“Unrealized losses on securities totaled $620.4 billion in the fourth quarter, down 10.1% from the prior quarter.”

Because that’s what happens when rates fall: The value of fixed-rate ‘Investment Securities’ increases. As the chart above shows.

(If you are interested in reading the latest FDIC report, here’s the link: https://www.fdic.gov/analysis/quarterly-banking-profile/qbp/2022dec/)

Silicon Valley Bank

Back to SVB. Fast forward to early March of this year. Moody’s — the credit rating agency — had notified SVB’s board a credit rating reduction was imminent. Worried this would be very bad for business, SBV quickly decided they needed to sell Treasury securities ASAP at a sizable loss and then raise additional ‘equity’ capital in order to attempt to preserve their credit rating.

This turned out to be an exceptionally bad choice, because it followed within days of the failure of the crypto-bank Silvergate Capital. Their choice and timing could not have been worse. A bank panic had begun.

In a ‘bank run,’ depositors withdraw their money and leave the bank like rats jumping off a burning ship. Late last week, prominent funds like ‘Union Square Ventures’ and ‘Coatue Management’ blasted out emails to their entire roster of startup companies: Yank your deposits from SVB as soon as possible. A bank run was triggered. And spread like wildfire. Within hours, as withdrawals accelerated, bank failure fear became a self-fulfilling prophesy.

Prisoner’s Dilemma

Had no one pulled their funds from SVB, the bank would be alive and kicking today. But frightened humans don’t work that way. Protect yourself was the call. Pull your money now was the command. So the bank failed. Had no one withdrawn money, the bank would have remained sound. Fear, panic and self-interest made that outcome impossible.

In this way, a bank failure is a bit of a paradox in decision analysis, much like a game-theory puzzle the “Prisoner’s Dilemma.”

Imagine you and a buddy are arrested and accused of committing a crime together. You did it, of course, and felt it was the “perfect crime”; and, you have no idea how the cops got onto you. Regardless, you’ve been nabbed.

Placed in separate rooms, and at the same time you both are told: Confess first – before the other guy – and you will be set free. The person remaining silent, however, will remain in jail, and if convicted of the crime, will spend up to 20 years in prison. But if you are too slow … and confess second, you will go to prison, having confessed to the crime. Finally, you know that if neither person confesses, it’s likely both of you will go free due to lack of evidence. In other words, if no one says anything, you’ll be set free.

What should you do? Do you confess and throw your buddy under the bus? If you do, how do you know – before you confess – that you confessed first? Because if you confess second, you go to prison. And if neither confess, you both go free. Should you stay silent … trusting your buddy will do the same?

A dilemma indeed.

If every depositor “trusted” the other depositors to do nothing, leave their funds in the bank, and relax, the bank would have survived. But that’s not what happened … and it probably never will. Human nature.

We all know that our bank is not sitting on the cash we deposited. Even though we are promised we can withdraw our cash at any time, we know they invested the money for a much longer duration. In “safe” things like home mortgages, US Treasuries, etc. But those investments fluctuate in value as interest rates change. And if rates go up really, really fast, assets purchased before the rate hikes are worth less, on a current-value basis, than before the hikes.

Which is why the FDIC permits member banks some latitude about how they manage this issue. A few decades ago, federal accounting standards were revised. Under this new standard, banks were required to report the “fair market value” of their assets in all public disclosures. But with a nuance. Banks have three (3) different possible labels for securities they hold on their books. And the bank can pick the label they want to use.

The “Hold To Maturity” — let’s abbreviate as ‘H-T-M’ — label means market value losses do not impact earnings or capital. Meaning, any “mark to market” losses can effectively be hidden from public scrutiny. If classified as “Trading” assets, those identical holdings would have been required to include the unrealized losses in their earnings and equity. A third category, “available for sale,” lets lenders exclude such losses from their earnings, but not equity.

At the end of 2022, SVB classified a large majority of their “Investment Securities” as H-T-M. When these securities finally matured, the bank would be repaid in full … at 100% … no losses whatsoever. So, as a result, the bank did not have to reduce the value of the securities on their books. They had about $97 billion classified as H-T-M. As the FED rate hikes grew in size, the current market value of these securities fell significantly. Even as the rate increases dented value, SVB could in theory “hold” those securities on their books thru maturity, without reflecting a value loss on their balance sheet.

Which worked fine until the decided to sell $21 billion of their H-T-M securities at a $1.8 billion loss. Bad call. Fatal call. They should never have sold H-T-M securities. They should have been held to maturity. They should have figured out some other way to increase or access liquidity. After this bonehead move, the dominos began to fall quickly. And by the end of the week, the FDIC owned the bank. SVB was dead and gone.

Unintended consequences?

In retrospect, it’s easy to see that something had to break. Across the globe, after a decade of near-zero and negative interest rates, central bankers rapidly lifted rates at a pace unseen in modern history. Ironically, what broke wasn’t the consumer’s willingness to spend money … although the most recent Commerce Department data shows consumer spending did fall slightly in February, after a 3.2% spurt in January. No what broke was the banks. Seemingly “safe” mid-duration investments like US Treasuries are worth less today than a year ago, and once the public’s awarness was awakened, fear flooded the banking system. Across the globe.

Now that pandora’s box is open, contagion effects are spreading. Do other banks have the same, or similar, problem? Sure. Will they fail too? That’s the fear brought by a bank panic and contagion.

First Republic Bank is in the news. One month ago, their share price was about $133. Today? about $33. Why? Is FRB also in trouble?

According to the WSJ, “First Republic showed a large gap between the fair-market value and balance-sheet value of its assets. Unlike SVB, where the biggest divergence is in its portfolio of debt securities, First Republic’s gap mostly is in its loan book.” Meaning they have made loans at interest rates far below current interest rates. Per that same WSJ article, in its annual report, First Republic said the fair-market value of its “real estate secured mortgages” was $117.5 billion as of Dec. 31, or $19.3 billion below their $136.8 billion balance-sheet value. The fair-value gap for that single asset category was larger than First Republic’s $17.4 billion of total equity.

Throwing the mortgages and securities (“financial assets”) into the same bucket, the fair value of First Republic’s financial assets was $26.9 billion less than their balance-sheet value. So, in theory, on paper, the bank’s equity has been wiped out. The combination of First Republic’s earlier “investment decisions” plus the FEDs rapid rate increases wiped out their entire equity base — on paper. It is an “unrealized loss”, not an actual loss.

Sure one could argue today they shouldn’t have made low interest rate loans, or bought longer-duration Treasuries, a couple of years ago when interest rates were close to zero. But at the time these investment were perceived as ultra-safe. Some day, perhaps sometime in the next couple of years, the FED will lower rates again, and these assets held by First Republic and other banks will magically regain their value … and all will be good in the world. Ahhhhhhh …….

On the liquidity issue, First Republic recently commented: “Sources beyond a well-diversified deposit base include over $70 billion of available, unused borrowing capacity.” So, unlike SVB, First Republic appears to have access to liquidity without selling off securities or mortgages. I wonder why SVB did not. Regardless, this fact aside, First Republic has been crushed in the past few days. Not only are their common- and preferred-stock prices down by spectacular amounts, their credit rating was “cut to junk” earlier today by S&P and Fitch, two credit rating agencies. Will First Republic survive this onslaught? Time will tell.

With all this turmoil, I expected to see a very weak SHI10 when I pulled the numbers a few hours ago. After all, the diners at our expensive eateries will probably spend close to $1,000 for ‘dinner for four’ at any of the 40 SHI restaurants. This same group both owns a lot of bank stocks and has large bank deposits. Are they worried? I thought yes, they are, and I expected reservation demand at $100-a-plate steak houses to be in low demand:

Nope. It turns out I was wrong. Demand is actually up this week. As my Irish wife and all my Irish friends know, Friday is St Patricks Day … so it’s possible Saturday reservation demand reflects this fact. Perhaps next week’s SHI will be more telling.

Was the bank break an unpredictable or unintended consequence of the FED rate tightening? I feel it was absolutely predictable … but I’m on the fence about whether or not it was intended. The FED has a tough job … bringing down sticky inflation is clearly a difficult task. That aside, I’ve previously commented I thought they went too far … too fast. It takes up to a full year for the economy to feel the impact of a FED move. Their overly eager rate hikes, I feel, broke the bank. And is now spreading contagion fears. My opinion.

Regardless, by actions and rhetoric, in short order they undoubtedly pushed the consumer and this economy to the breaking point. One large bank failure is now in the history books. Will there be more? Quite possibly. Human nature suggests the widespread fears will not quickly abate or be easily constrained. Keep your fingers crossed for a FED rate hike “pause” later this month.

Good luck out there … these are crazy times indeed.

… <|:.:|> … Terry Liebman