SHI 5.18.22 – Reading The Tea Leaves

SHI 5.11.22 – Cult Members Needed

May 11, 2022

SHI 5.25.22 – Economic Long COVID

May 25, 2022

In December, the FED changed their mind.

In an abrupt policy pivot, they decided the current bout of CPI inflation is not transitory. Month after month, CPI readings pushed higher. And month after month, the unemployment rate edged lower. Enter the pivot and new FED rhetoric and direction. Inflation is an existential problem, they told us, and it must be slowed.

Today, they continue to sing from the same hymnal. Inflation must be tamed, Powell tells us. And since the FED has no belief they can impact the very-much-broken ‘supply-side’ of the economic equation, they are forced to focus on reducing the ‘demand-side.’

“

Consumer demand continues to outstrip supply.”

“Consumer demand continues to outstrip supply.”

… according to the FED. Perhaps. This has certainly been the case in the past year or so … but is aggregate demand for both goods and services, here in America, still outstripping supply? Is this pattern continuing today? A great question to be sure.

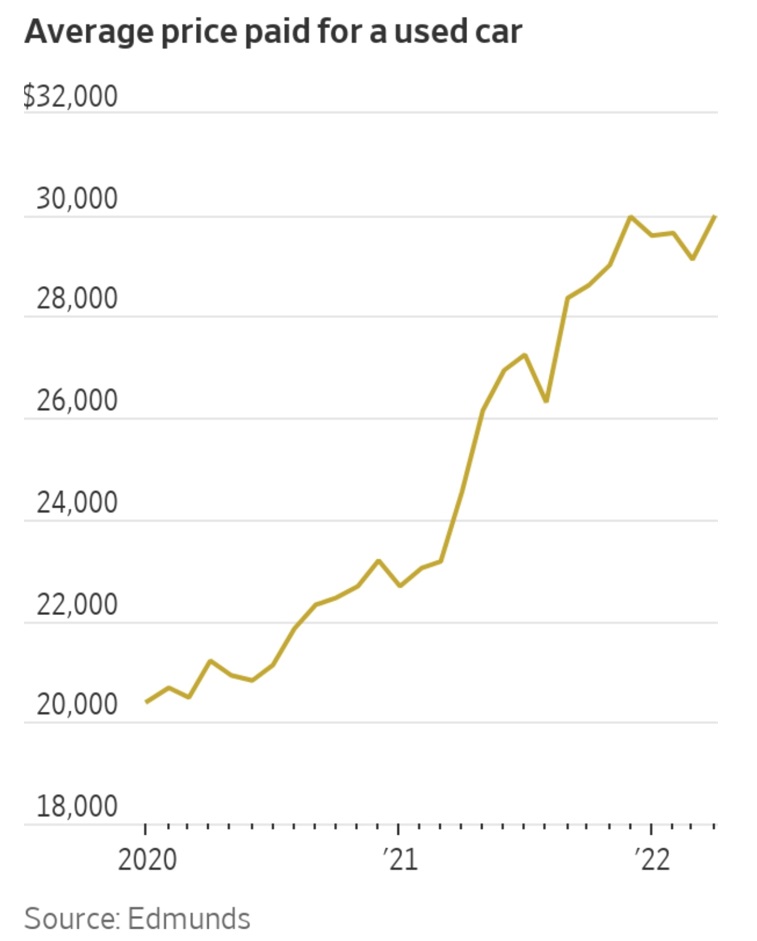

In conditions such as these, an ‘auction’ of sorts plays out in the purchase of goods and services. We all know what happens at an auction: Prices shoot to the heavens. Consider the market for used cars.

The chart at the right, courtesy of Edmunds, boldly demonstrates this fact. Over the past 2 years, the price paid for the average used car is up about 50%. In just two years!

Has the quality of used cars improved over the past two years? Of course not. And yet prices have skyrocketed. Why? Supply and demand. Disposable cash and supply-chain constraints. Post-pandemic, American bank accounts were flush with stimulus funds. New car deliveries were dreadfully inadequate in number and delivery timing and that used car began looking better and better. Prices responded in kind.

But is this inflation? On one hand, used car prices are clearly much, much higher. Again, this is a fact. Flush with cash, and tired of driving around their much older clunker, numerous Americans made the decision to buy a new car.

But it was unavailable. The reasons were numerous and unimportant for today’s discussion … but new cars were hard to come by. And thus consumers, armed with wheel barrels of cash, turned to used cars. An auction began and we saw the typical outcome: Given the relatively fixed supply of used cars, surging demand caused the impressive price spike we see in the chart.

But now prices are moderating. Used car prices have actually come down in recent months. Facing 50% price increases and shrinking bank accounts, many potential used car buyers made the decision to put of that purchase. And wait. Ostensibly for either used car prices to decline or new cars to be available.

A used car purchase is known as a “discretionary” purchase. Consumers can choose to put off the decision if they wish. Armed with cash, many did not. They bought. Now that bank account balances are much lower what will they choose to do? Will the used car auction continue … or will consumers pause? I contend the will pause. I believe used car prices have peaked and prices will decline in the coming months.

The challenge facing the FED, of course, is the fact that many items in the ‘CPI basket’ are not discretionary. Food, for example, is not overly discretionary. We all must eat. The “food” category counts for 13.3% of the CPI basket. Eggs are up 22% Y-O-Y. Bacon? 17.7%. Lettuce will cost you a lot more green: It’s up 12.7% Y-O-Y. In many respects, these items are not discretionary. Consumers can substitute … but food must be eaten. Will the prices of these items fall in future months, following the lead of used cars? I believe that is far less likely. The input costs to produce each of these items are also up significantly. I fear it is unlikely the prices for these items will moderate much at all in the coming months. Their cost may plateau, but I doubt prices will fall.

As I parse the list of CPI inputs, I feel there are clearly items on the list that manifest inflation. There is no doubt the cost of rental housing has increased significantly. This is also a trend I fear will not be easily moderated, FED action or not. But I believe the size of the increase in food, energy and transportation (oil) costs is a reflection of supply constraints, not excess demand. That “size factor” will moderate on its own in coming months. Help from the FED, I believe, is not warranted.

Regardless, since the FED feels they cannot “fix” the supply side of the equation, they plan to fix the demand side. So here’s today’s question for you to ponder: When the FED decides to “fix” the “excess demand problem” facing our economy today, what are they really saying?

The answer may surprise you.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. Significantly. By the end of Q1, 2022, in ‘current-dollar’ terms US annual economic output clocked in at $24.38 trillion. Yes, during Q1, the current-dollar GDP increased at the annualized rate of 6.5%. The world’s annual GDP rose to about $95 trillion at the end of 2021. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

I began writing this blog post over the weekend. The title — “Reading the Tea Leaves” was a bit more mysterious on Sunday when writing began. No longer. Yesterday, during The Wall Street Journal’s ‘Future of Everything Festival’ Powell made this comment:

“Restoring price stability is an unconditional need. It is something we have to do. There could be some pain involved.”

Reading the tea leaves just got a lot easier.

Pain? Sure: Look no further than the stock, bond and cryptocurrency markets. 🙂

But that’s not the pain Chairman Powell is talking about. He’s talking about your pain. Folks who are employed right now with good, well-paying jobs. Mr. Powell and the FED plan to inflict a fair amount of pain on many of you and the other almost 158 million Americans that are currently employed. The FED expects to increase the unemployment rate by a large enough margin to moderate both consumer spending and wage hikes — both of which contributed significantly to CPI inflation in the past year.

Our US unemployment rate is hovering near a half-century low — right at 3.6% at last count. In April the US economy added another 428,000 jobs … led by hiring in the restaurant, hotel and other ‘leisure’ markets. And job openings in the most recent JOLTs report (“Job Openings, Labor Turnover”) continued to increase in March, to over 11.5 million. Yes, at the beginning of April, American businesses were seeking 11.5 million additional employees.

Powell plans to change that. At that same WSJ festival, he commented:

The unemployment rate consistent with stable inflation is probably well above 3.6%.

Perhaps.

Apparently this is true if the US financial markets are booming, interest rates are near zero, and the government continues to hand-out trillions of dollars in stimulus payments. Clearly, stimulus payments stimulated spending! That fact has been proven with a capital “P.” In the past two years, we tested ‘Modern Monetary Theory‘ and proved it is a complete farce. As it turns out, a massive expansion in money supply, absent a commensurate increase in GDP, will trigger inflation. MMT is dead.

But now that much of the stimulus funds are spent and gone, the financial markets are tamed and “risk off” is the name of the game, home loan rates are up appreciably, and all other interest rates have also headed up, must the FED push millions of folks out of work to tame inflation? Is this outcome necessary? Does the “script” demand the FED raise interest rates until a much-higher unemployment rate takes the steam out of our economy and pushes a lot of folks into the unemployment lines?

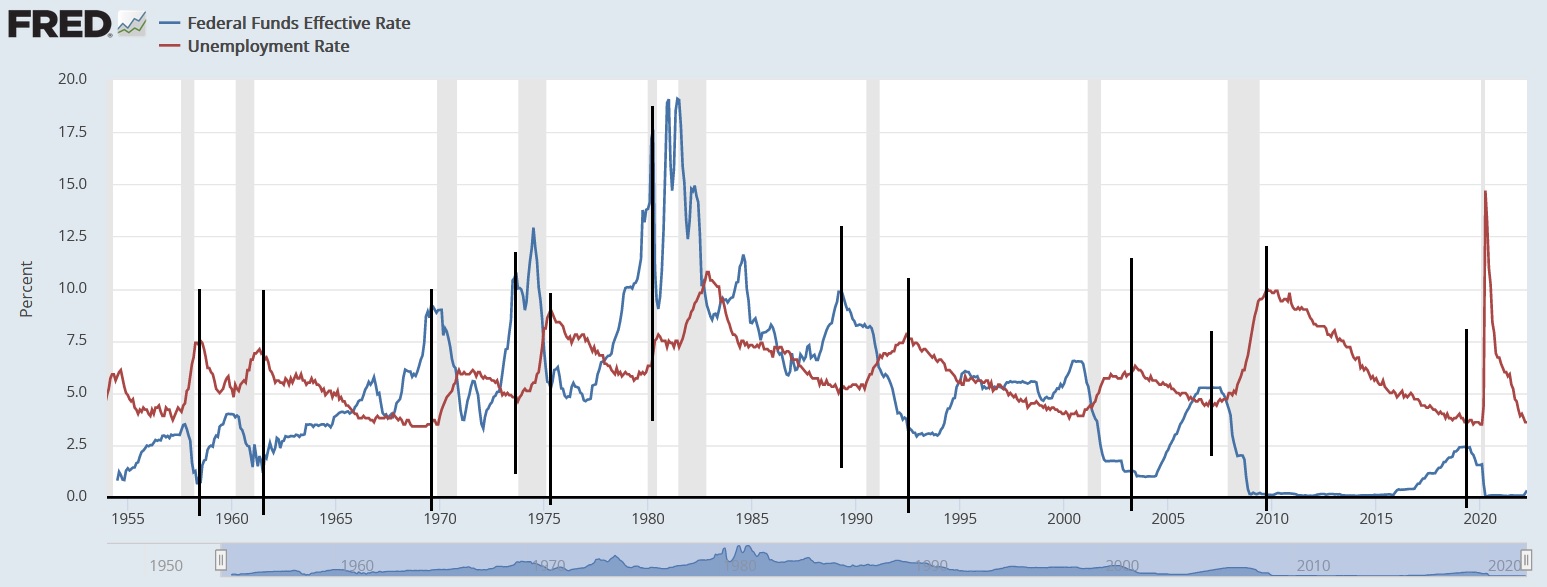

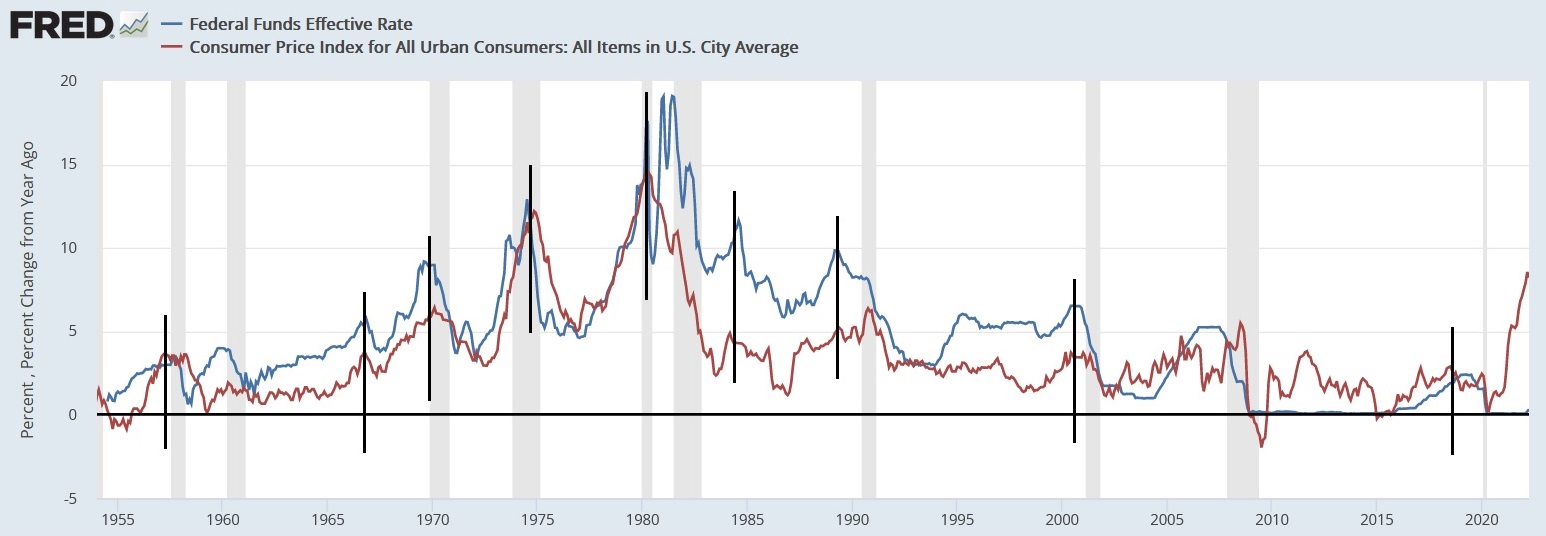

That’s been the script in the past. Consider this chart, courtesy of the St Louis FED:

Over he last 60 or 70 years, the FED has raised — and then lowered — interest rates following this identical script. Note that the peak in the unemployment rate has generally corresponded with a bottom in the FED funds rate. The two are highly inversely correlated. And the opposite is true. Meaning the FED funds rate increases — just like the rate increases happening now — generally preceded a significant increase in the unemployment rate (the red line). In the 1950s, FED rate increases triggered about a 3% increase in the unemployment rate — terminating at about 7.5% before falling again. In the 1960s, FED actions caused about a 2% unemployment rate increase. In the 1970s, the unemployment rate increase was even larger — over 3%. And the pattern repeated 1980s, the 1990s, and the 200os. The only decade to escape this outcome in the last 60 or 70 years was the 2010s … for different reasons. However, the FED is once again following the same script.

It’s worth mentioning that a 1% hike in the unemployment rate means about 1,570,000 people lost their job. A 2% increase will put more than 3.1 million people out of work. But Powell is telling us that history proves the script works time after time. After enough “pain”, the economy will slow and the CPI will fall.

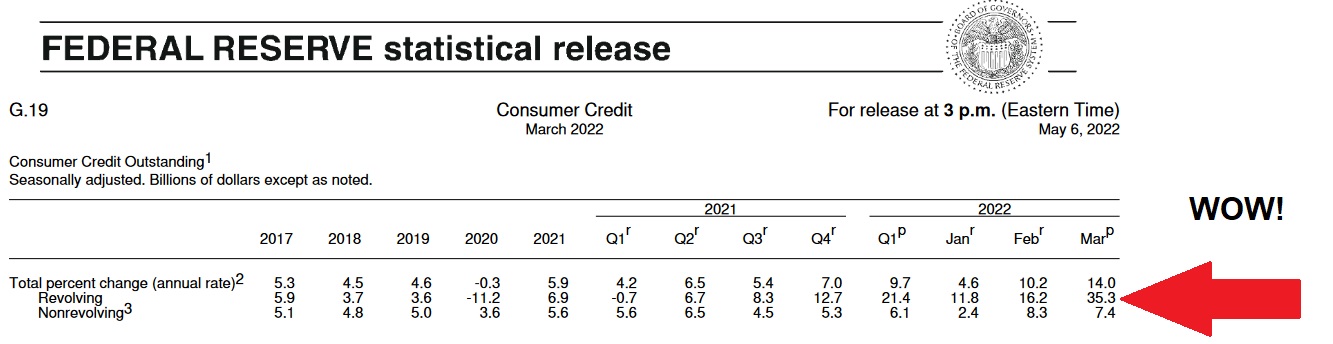

Likely adding further incentive to the FED‘s resolve may be the most recent consumer credit numbers. Consider this chart:

That’s right: ‘Revolving’ credit balances — mostly credit cards — increased at an annualized rate of over 35% in March! Compare this rate to the numbers from 2017 thru 2021. That is a staggering increase … and it comes on the heels of a heated increase in the prior month. Consumers are buying … and their plastic is heating up! In the face of this clear and stark evidence, what choice does the FED have? Apparently Powell and the FED believe they have only one: Raise rates until the consumer, the financial markets, the worker and the economy squeal in pain. It’s worked before … and the FED apparently believes it will work again.

The chart below clearly shows that steadily lifting the the FED funds rate (the blue line) against the backdrop of a consistently rising CPI inflation number (the red line) eventually results in a decline in the CPI.

Of course, that same script seems to have caused an recession just about every time the FED used it. Each of the vertical gray bars in the chart above represent an economic slowdown. Will current aggressive FED actions cause another recession? OOOOooooo … let’s check the “tea leaves” at the steak houses. Look into the cup … tell me what you see:

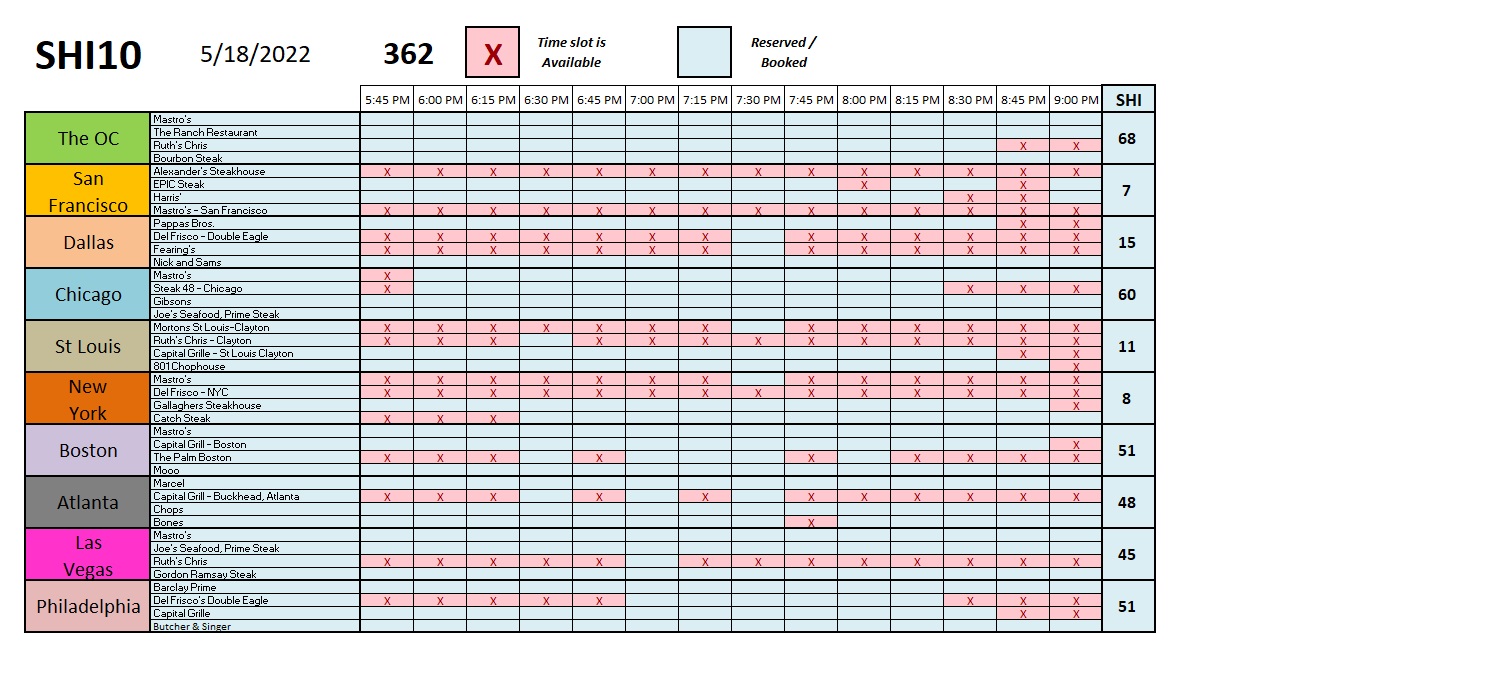

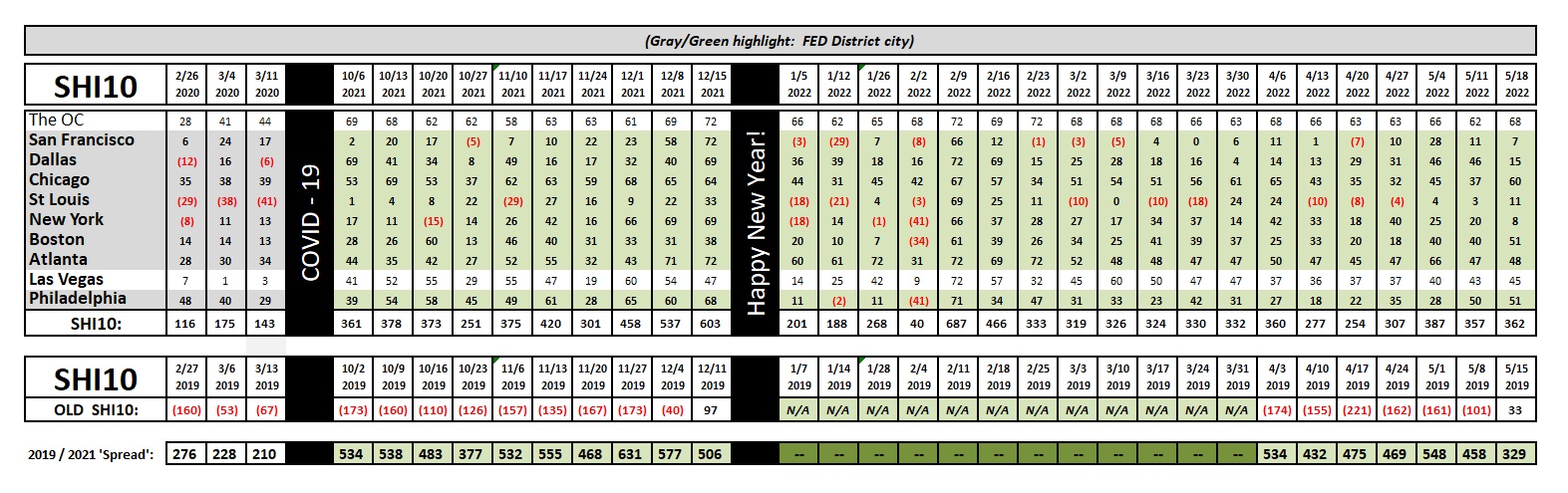

I see reservations! Here in the OC, it’s pretty clear our well-heeled diner is not yet begun worried about their stock losses. Steak house reservations are in high demand. Every SHI market across the country is manifesting relatively strong demand. Here’s the trend report:

We see expensive eatery demand softening a bit in Dallas, and New York, but every other market seems to be holding its own for now. Expensive steak demand is strong. So far. 🙂

But will it remain strong? Time will tell, of course. Because no one needs to buy and expensive steak at Mastros, just like no one needs to buy a new TV or kitchen appliance right now from Walmart or Target. And apparently they are not. As recent quarterly financial reports from both suggest, those discretionary purchases are slipping significantly. It appears that as of Q1 of this year, the “value shopper” has already begun to moderate their discretionary purchase activity. Just as they’ve done in the used car market. Of course, our opulent eatery patron is not a value shopper. And so far, it appears, demand for expensive discretionary items in this income segment is holding up.

In any event, it now looks like the FED plans to follow the typical play-book:

Step one: Food, housing and energy prices rise significantly, causing pain and anger across the country. Politicians are worried as households of moderate means are strained.

Step two: The FED takes action, beginning a “quantitative tightening cycle” to slow an overheated economy and reduce aggregate demand. Price increases and interest rate increases eventually dampen consumer demand for discretionary purchases reliant on borrowed money: Purchases of large ‘durable’ items like cars and refrigerators, and possibly even expensive steak dinners first go on plastic, but soon slow down. The threat of continuously higher rates may cause many to think twice before buying a T-Bone from Gordon Ramsey.

Step 3: Stock markets are spooked by (1) rising earnings uncertainty and (2) the fear of higher rates discounting the value of future earnings. Stock values tumble. The value of all bonds declines in direct inverse correlation to the size of the actual and anticipated rate hikes. The ‘wealth effect’ works in reverse: Wealthier investors ‘feel’ their paper losses and begin to scale back purchases of discretionary items. Thereby creating their own negative feedback loop, perpetuating the pain and the problem.

Step 4: Rising business and financial uncertainty rises and the appetite for ‘risk’ assets and risky investment strategies declines meaningfully. In this environment, business investment decline, further straining GDP growth. Business expansion will slow. Business options are reassessed and the riskiest are benched. Demand for labor falls in correlation.

Step 5: The economy inevitably slows. Both steps 3 &4 above directly impact the demand side of our economy, reducing aggregate demand across the entire economy.

Step 6: The JOLTs report reflects a significantly lower number of job openings. New hiring slows. Unemployment rates climb. Over 4% … over 5% … over 6% … the pain! Millions are unemployed.

Step 7: Eventually the FED eases rates once again, and soon interest rates decline.

Of course, the “pain” Powell referenced yesterday is now widespread. Pretty much everyone is feeling it by the time interest rates again begin to fall.

Is this script and play book inevitable and mandatory?

It’s hard to say, of course. Because today’s conditions are different that every prior cyclical episode. I believe this time is truly different. Apparently the FED disagrees because they’re following the ‘tried-and-true’ script once again. I contend that this time aggregate demand will fall on its own. I believe that trend has already begun. Clearly the FED disagrees.

Today, the globe faces very, very serious supply constraint headwinds. For the first time in decades, global supply routes and relationships are being re-imagined and rewritten. Russia is out. Permanently. What non-Russian company in their right mind would choose to do business in or with Russia again? Google? Not a chance. Earlier today, Google announced that ‘Google Russia’ plans to file bankruptcy after Russia seized its assets and bank account, making it impossible to pay Russian employees. Or anything else for that matter. No, Google is not going back into Russia any time in the next century or two. Nor will most companies that have left post-invasion.

And, of course, China is out; well, not out per se, but they are no longer the global manufacturer of choice. Perhaps India will take over? Hmmm…..

The disruptions we’ve seen are legitimate, durable, and in my opinion, are the cause of the majority of the global inflationary pressures we’re feeling today. Of course, another factor was the trillions in fiscal “helicopter money” rained down on consumers around the world. That stoked the flames.

But now, the money rain has stopped. That solves part of the problem. But the supply chains remain broken. Until they’re sufficiently healed, and the “supply-side” of the equation is adequately fixed, under the current conditions demand may continue to outstrip supply, fueling further CPI increases. Which, of course, is the outcome the FED is hoping to stop with their aggressive actions. We all know what happens after we sit in an ice bath: It gets very cold very quickly. The FED has dumped our American economy into the financial equivalent.

This is a rapidly changing landscape. The FED has pivoted a a few times, and may continue to do so as conditions evolve. I hope so. Because I’m of the opinion their latest pivot is excessive. Aggregate is already moderating. I believe inflation is already waning.

Their current stance will cause far more pain than conditions warrant. I believe the FED is acting far too aggressively in their stated desire to crush inflation. Perhaps they will soften their stance in the coming weeks. But for now, taking the FED at its word, I think we’d all better get ready: Powell has told us pain is coming in fast and heading our way. Unless Powell and the FED pivot again, pain is about to become “Everything Everywhere All At Once” which, until today, I thought was only the title of an exceptionally unusual movie.

Go see it. For a couple of hours at least, you’ll forget your pain. 🙂

<:> Terry Liebman