SHI 5.20.20 – Smoking Cigarettes Can Kill You

SHI 5.13.2020 – Leaving California

May 13, 2020

SHI 5.27.20 – Climbing the Mountain

May 27, 2020

But you already knew that. Here’s what you may not have known:

” A stay in a nursing home can kill you, too. “

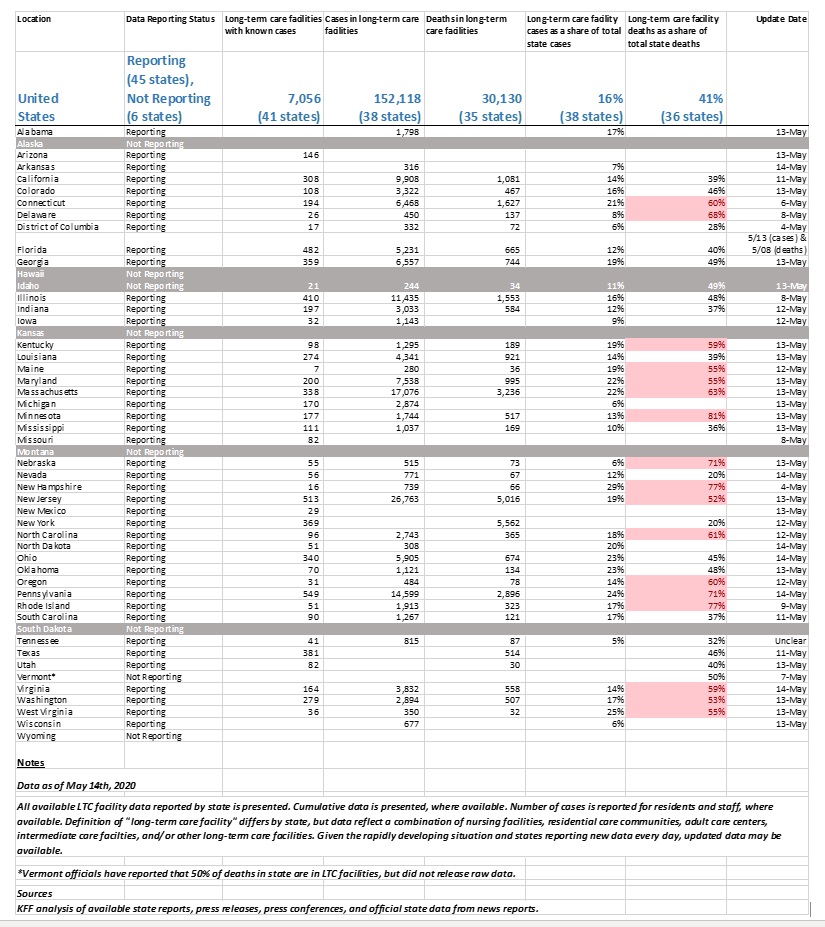

Sure, folks in nursing homes are old and frail. That’s why they’re in nursing homes in the first place. But those in ‘long-term care facilities’ are not dying because the are old and frail … they are dying in record numbers from Covid-19. Because of the people who are bringing Covid-19 into nursing homes in the first place. Am I exaggerating? Nope. Take a look at the data, courtesy of research compiled by the Kaiser Family Foundation as of May 14th:

-

In the 38 US states reporting this data, 16% of all CV-19 cases have appeared in nursing homes.

-

Yet, 41% of all CV-19 deaths in those states are residents from nursing homes.

The data from individual states is even more staggering. Of the 38 states reporting, here is a top-10 list of individual states and the percentage of ALL CV-19 deaths in the state that occurred in nursing homes located in that state:

-

- Minnesota: 81% of all CV-19 state deaths have taken place in nursing homes.

- Rhode Island: 77%

- New Hampshire: 77%

- Pennsylvania: 71%

- Nebraska: 71%

- Delaware: 68%

- Massachusetts: 63%

- North Carolina: 61%

- Oregon: 60%

- Connecticut: 60%

- Minnesota: 81% of all CV-19 state deaths have taken place in nursing homes.

Some states have fared better. But in the aggregate, 41% of all CV-19 deaths took place in nursing home (36 states reporting), whereas just 16% of all CV-19 cases were reported in (almost) the same nursing home group (38 states reporting.)

Here’s a link to the data source if you want to look deeper (right click, open in a new window) — there’s a bunch of additional information here: https://www.kff.org/health-costs/issue-brief/state-data-and-policy-actions-to-address-coronavirus/?utm_source=web&utm_medium=trending&utm_campaign=covid-19

Finally, below my ‘signature,’ I’ll attach the chart of all individual state data. Draw your own conclusions. I’ve already made my opinion patently clear.

Time to move on: let’s get back to the data of economics.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Before COVID-19, the world’s annual GDP was about $85 trillion today. No longer. It has shrunk sizable during ‘The Great Lockdown.’ I did not coin this phrase — the IMF did. The same folks who track global GDP. Until recently, annual US GDP exceeded $21.7 trillion. Together, the U.S., the EU and China still generate about 70% of the global economic output.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

Later today, the US Treasury will sell $20 billion of “20-year” Treasury bonds. 20-year bonds haven’t been sold since 1986. In total, the Treasury has indicated they plan to sell $54 billion of 20-year Ts over the next few months, to help finance a portion of this year’s already massive budget deficit.

Yield expectations are in the 1.2% +/- range. Meaning that $20 billion of new bonds will cost the US Treasury — and the US taxpayer — about $240 million each year for the next 20 years. The UK also sold government debt today. They sold 3.75 billion in English pounds of 3-year bonds earlier today. They did much better than the Treasury is expected to do: their $4.6 billion (equivalent) sale was snapped up by investors at an average yield of negative .003%. Yep. Negative. Which means the UK will not pay interest to the investors for this loan. Nope, the investors will pay the United Kingdom $138,000 each year, for the next 3 years, for the privilege of owning the debt. 🙂

Crazy, right? Well here’s another interesting tidbit for you: Can you guess who’s been buying the vast majority of Treasury securities lately? You got it! The Federal Reserve. Since mid-March, in order to stabilize our sovereign debt markets, the FED has acquired about $1.5 trillion of Treasury securities. Will the FED buy the 20-year bonds issued by the Treasury? Probably not directly, but they are currently on pace to buy about $6 billion of Treasuries each week … so indirectly, their actions “make room” for the new Treasury securities. How much will the FED earn on the $1.5 trillion of Treasury securities it has purchased? Well, they’ve bought a combination of short- and long-term debt, so probably less than 1.2%. But if we assume an average interest rate of, say, 0.5%, then the FED will earn $7.5 billion each year on their $1.5 trillion investment. Nice! And remember: This is without any cost, because the FED simply ‘creates’ the money and then uses their newly minted dollars to buy the Treasury securities. And here’s the even better news: The FED pays 100% of their annual net income to the Treasury! Said another way, the bigger the FED balance sheet becomes, the more the Treasury — meaning the US taxpayer — makes! So, thru this lens, it appears we’re doing better than the UK! I don’t make this stuff up, folks.

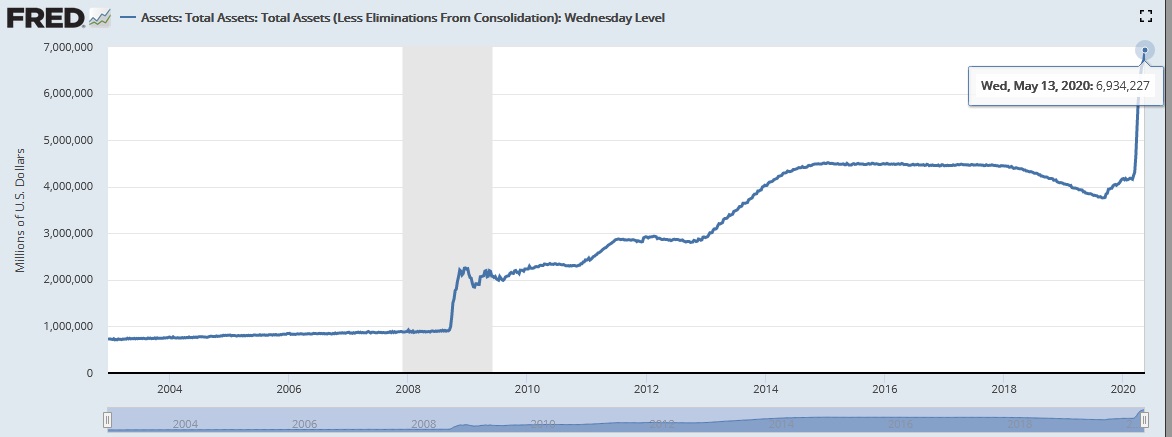

Here’s an image showing FED balance sheet movement since 2004, from data provided by our fiends at the St Louis FED:

So, as of May 13th, the FED balance sheet had swelled to just below $7 trillion — almost double its size from September of last year. (You’ll recall it “peaked” at about $4.5 trillion in 2015.) And it is almost certain to grow much, much larger. The FED is in a box, one with unlimited dollar resources but only one choice: It must maintain Treasury market stability … as the new securities are sold to pay for the US coronavirus-generated deficit. So, if the 2020 US deficit rises to, say, $6 trillion — a potential, if not likely, outcome — the FED will be tapped to acquire enough Treasury securities in the open market to keep the market stable and short and long-term rates at today’s historic and ultra-low levels. All the while, earning a good return on its zero-cost investment, ultimately returning all the profit to the Treasury. 🙂

The FEDs balance sheet is likely to exceed $10 trillion by the time the year is over. In 2017, with a much smaller balance sheet, the FED was able to pay the Treasury about $80 billion in profit. Rates are quite a bit lower today, so their earnings per invested dollar will be lower. But it’s possible the FED could return $100 billion to the Treasury when 2020 finishes.

Good news? Bad news? You decide … but either way, staring down the massive deficits looming in our future, it is certainly a silver lining.

Here’s another silver lining:

Do you plan to take on any new debt? Or refinance your home? Purchase an investment property? Perhaps buy or lease a new car? Well … here’s some good news for you! Once the economic recovery begins, and all financial markets stabilize, you will likely see the lowest financing rates you’ve ever seen. No, credit cards will probably stay at 21%. But you might be able to refinance your home for 30-years with a 2% interest rate! Wouldn’t that be nice? Stay tuned … it’s coming.

– Terry Liebman