SHI 5.9.18 Americans are Working!

SHI 5.2.18 Cracks in the Wall

May 2, 2018

SHI 5.16.18 Buying Steaks and Other Stuff

May 16, 2018

The April unemployment rate plummeted to 3.9%! Americans must be working!

A 3.9% unemployment rate is a good thing! This must mean many more Americans are working this month than last, right?

Unfortunately, no. In fact, when we look behind the headline employment numbers once again, we see that the number of “Employed” Americans actually increased by only 3,000 during the month of April. Only 3,000!

Which begs the question, “Golly, if only 3 thousand more folks got new jobs during the month, how did the unemployment rate drop so much?” Great question. You’re getting good at this stuff! 🙂

Here is this week’s blog summary:

- In April, the US unemployment rate fell to 3.9% – the lowest ‘official’ unemployment rate since December of 2000.

- The size of the labor force shrunk by 236,000 folks, causing the ‘participation rate’ to decline again, now at 62.8%.

- The number of people not in the labor force increased by 410,000.

- U-6 – our alternative unemployment measure improved, declining to 7.8%

- Year over year, average hourly earnings have increased by 2.6%.

- Wage inflation remains dormant.

The short answer to the question above is this: The unemployment rate fell so dramatically because the labor pool declined by 236,000 people. The number of folks not in the labor force is growing rapidly! Read on for a more detailed analysis and discussion.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will continue to be true for years to come.

Is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is almost $80 trillion today. US ‘current dollar’ GDP almost reached $20 trillion during Q1, 2018. We remain about 25% of global GDP. Other than China — a distant second at around $11 trillion — the GDP of no other country is close.

The objective of the SHI10 and this blog is simple: To predict US GDP movement ahead of official economic releases — an important objective since BEA (the ‘Bureau of Economic Analysis’) gross domestic product data is outdated the day it’s released.

Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric.

The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

Open this link. It’s worth a quick look: https://www.bls.gov/news.release/empsit.a.htm (Right click on the link and choose “open in another window.”)

The numbers are in thousands. We see that either due to immigration or age changes, the number of Americans in the labor force grew by 175,000 people in April. Yet the size of the labor force declined by 236,000. If we add these two numbers together (and ignore a bit of rounding error), we see the 410,000 folks who left the labor force in April. That dynamic, not a large increase in the number of working Americans, is what drove the unemployment rate down to 3.9%.

In the final analysis, our low unemployment rate isn’t a “new jobs” story. It’s a demographics story. And, as I’ve said previously, is eerily similar to the demographics story unfolding in Japan.

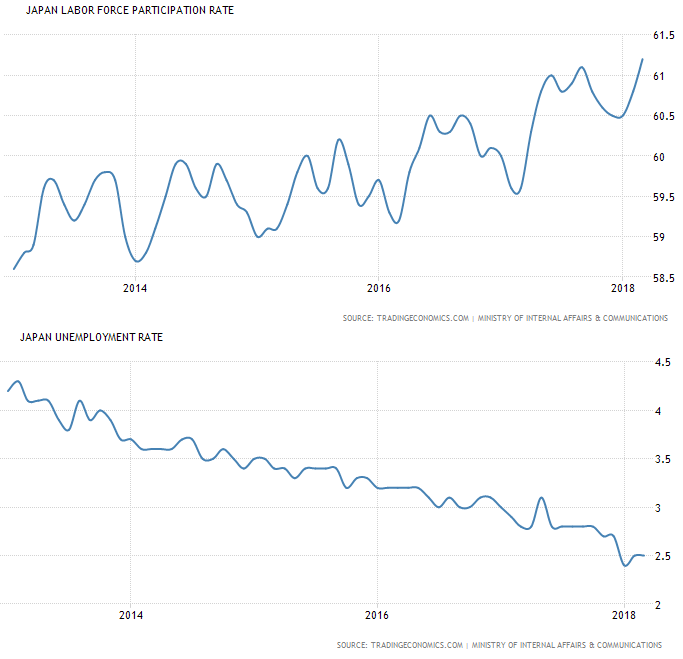

What is Japan’s unemployment rate? Take a look:

That’s right: The March, 2018 unemployment rate in Japan was 2.5%. The size of their labor force is 68.67 million folks; but an additional 42.29 million “able bodied” Japanese are “detached” from the work force. Giving Japan a “participation rate” of 61.89%. Just about 1% below ours.

Last month, US demographics drove the unemployment rate down. Not new jobs. Those totaled only 3,000 for the month. So why are economists and financial pundits so giddy about the 3.9% unemployment rate?

I’m not sure. Yes, it’s great that 96.1% of American who want to work have a job. That’s definitely a good thing. But in the past year, the number of Americans “not in the labor force” increased by 1,338,000!

So who, precisely, are the folks “not in the labor force?” Well, according to the U.S. Bureau of Labor Statistics (BLS), the ‘civilian labor force’ includes folks who are:

- both employed and unemployed (people either looking for, or who have, a job),

- 16 years of age or older; and;

- not “institutionalized.”

The rest of Americans — those who are neither employed nor looking for a job — are considered “not in the labor force“.

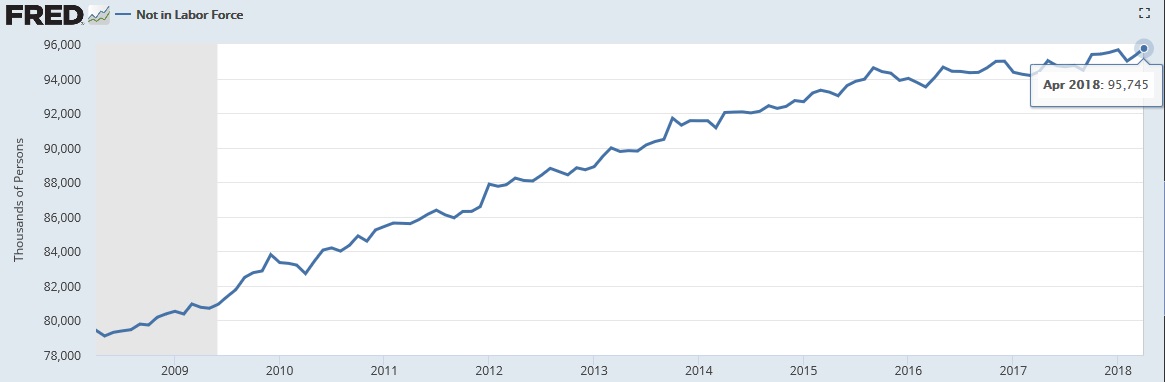

In the US, as in Japan, this is a serious longer-term problem. Sure, we have about 155 million working Americans right now, but that number is growing very, very slowly. Remember, in the past year alone, 1,338,000 more Americans exited the US labor force. This group has been growing for years. Here’s a 10-year chart, courtesy of FRED:

Yes, you see that number correctly: In April of 2018, almost 96 million Americans were not in the labor force! Remember, in theory, these are people who could take a job if they chose to. But, for personal reasons (age, health, desire, etc.) they were neither working nor were they seeking employment.

Folks, this is a growing problem. Over time, economic growth requires either (1) a growing labor force, or (2) increasing productivity. Preferably both. While our labor force is growing, albeit slowly, the number of people not in the labor force seems to be growing faster. Not only does this group become a drag on the country’s resources, but this group tends to have spending habits which are not supportive of a consumption-based economy.

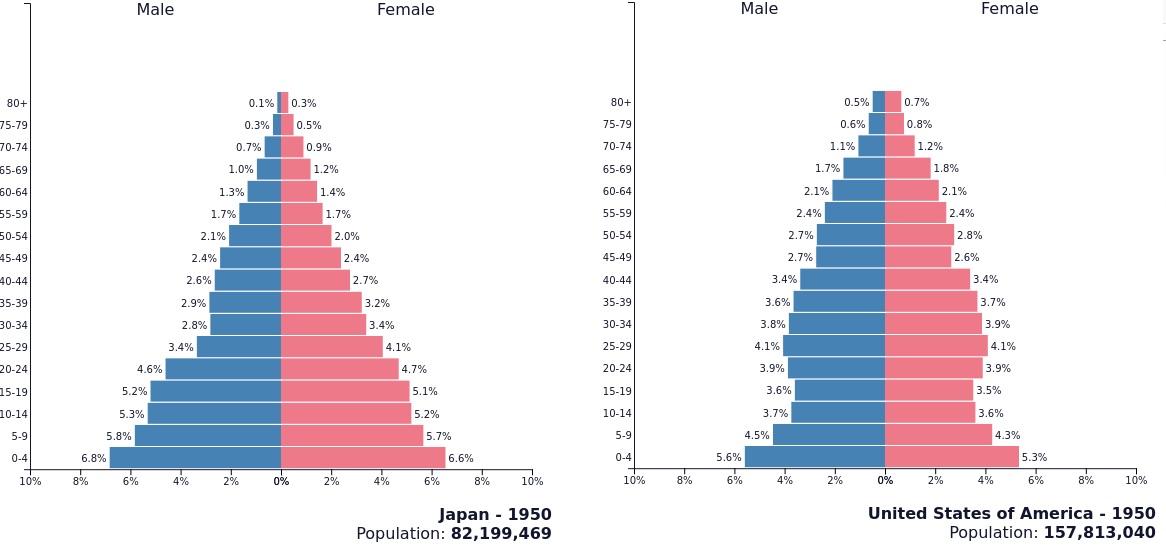

The origin of the problem is easy to see. Take a look at these two images below. The first shows the US and Japan ‘population pyramid’ from 1950. Both resembled an actual pyramid — large on the bottom…very thin on top.

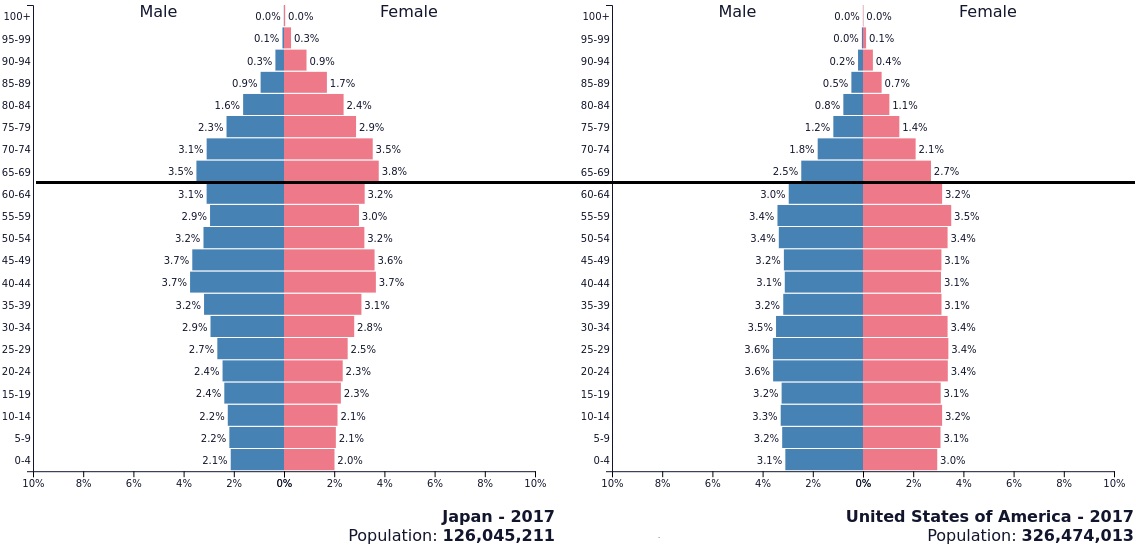

Now take a look the the 2017 pyramids for both the US and Japan. They tell a very different story:

Clearly, both the US and Japanese pyramids are rather top-heavy. I’ve drawn a black line at the 65 year cohort. Japan is in bad shape … but the US isn’t far behind. It’s easy to see why the US and Japan labor forces are shrinking: People are retiring. And number of new entrants into the labor force (the 15-19 year cohort) is much smaller than those leaving — again, Japan is in worse shape than we are.

But this dark cloud hanging over the US may have a silver lining. 🙂

Take a look at the images below. I’ve vertically lined up two (2) charts, so we can easily see the time correlation. The top chart is Japan’s labor force participation rate for the past 5 years. The bottom chart is their unemployment rate. (Courtesy of TradingEconomics.com)

The message is clear: As Japan’s unemployment rate fell below 4%, more people decided to go back to work. People who previously were “not in the labor force” decided to rejoin and get a job. As a result, Japan’s participation rate increased quite a bit.

The same thing is likely to happen here in the US. Assuming our unemployment rate continues to decline, a significant number of retirees are likely to return to the work force. Not only will this help with the US labor shortage, its a solution likely to be inexpensive from a wage perspective. Alternatively, it is unlikely to help labor productivity. Sorry, but us old folks aren’t as spry as we used to be. 🙂

The bottom line: Due to demographic changes, it is likely the US — like Japan — will have low unemployment rates during economic expansions far into the future. But … both countries have millions of folks on the sidelines who, with the right incentives, may agree to come back into the office or plant!

Here’s an interesting question: Like Japan, will the US inflation rate be unaffected by the low unemployment rate? Or will wage inflation push up the US inflation rate?

Economic labor theory suggests Japan’s inflation rate should be much higher than 1%. Yet Japan’s inflation rate seems to be stuck at 1.1% or lower. My opinion? The answer is pretty simple: As US and Japanese populations age, in the aggregate folks buy less “stuff” (goods and services) than when they were younger. And post retirement, they are willing to work cheaper.

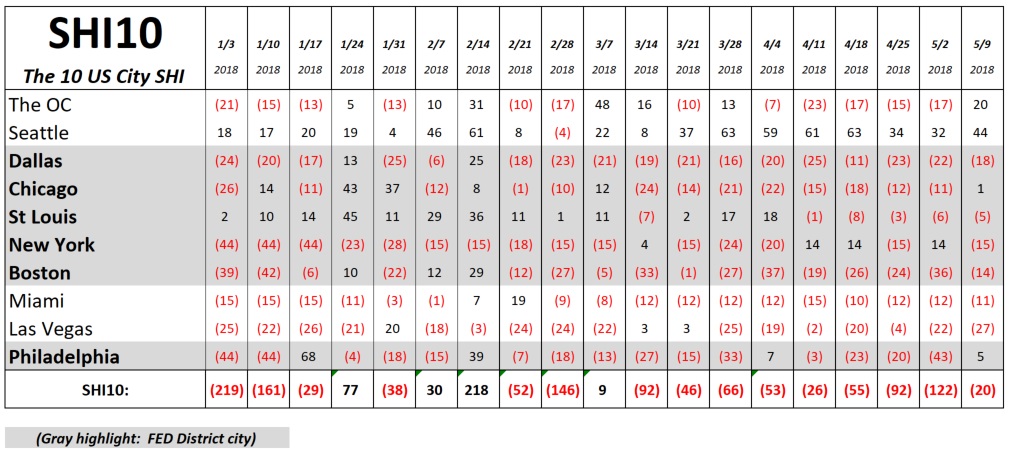

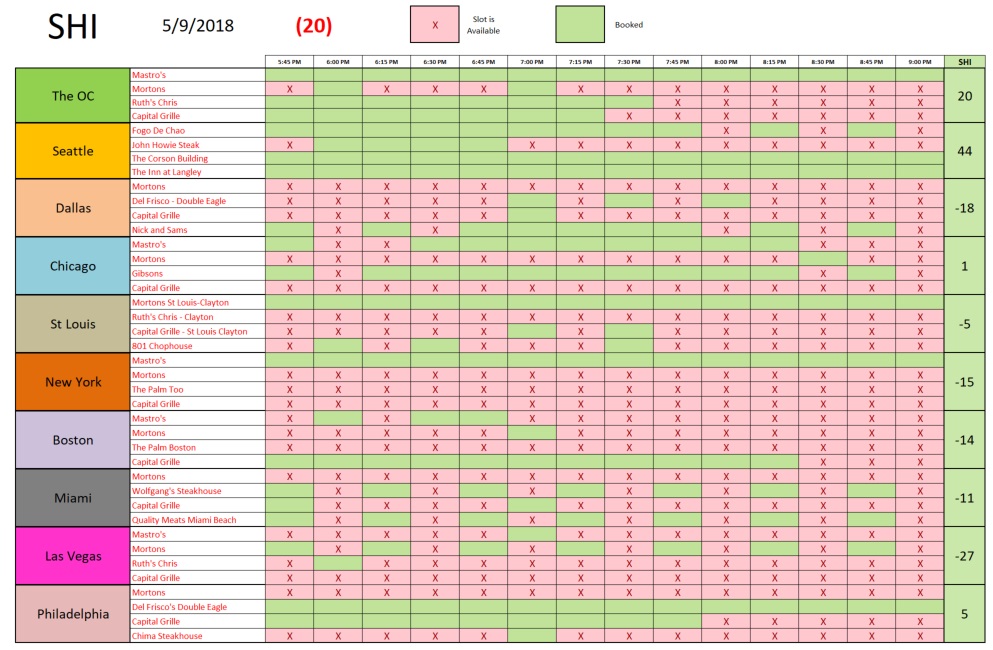

Time will tell. And now it’s time to head to the steak houses. What are expensive slabs of beef telling us about our economy this week? Like a Prime Rib in the skillet, our economy is clearly sizzling! Restaurant reservations at our posh chophouses are flying off the shelf this week. Take a look at the SHI10 5/9 improvement over prior weeks:

With the exceptions of only NYC and Las Vegas, every other market in the SHI10 showed a significant increase in restaurant reservation demand this Saturday. The OC is having a great week. And take another look at the Seattle numbers. Once again, this city leads the SHI10 by a significant margin. If you have any cow friends, you might warn them to stay away from Seattle! Clearly, it’s dangerous up there!

One week does not make a trend … so we cannot yet conclude Q2 GDP growth is accelerating. But the longer-term SHI10 trend gives the correlary argument plenty of support: Continued strong demand for expensive steak houses is consistent with a strong economy. While there are storm clouds far out on the horizon, the economy remains fundamentally sound. For now. No recession in sight.

– Terry Liebman