SHI 5.2.18 Cracks in the Wall

SHI 4.25.18 Lumber, Reach for the Sky!

April 25, 2018

SHI 5.9.18 Americans are Working!

May 9, 2018

Signs of economic softness are appearing. It’s a mixed bag out there.

Economic cycles are, well, cyclical. This will never change.

Cycle length and amplitude are always variable, but new cycles always come and go. Globally, I believe we’ve seen the peak of this one:

- US Q1, 2018 GDP growth was good: A solid 2.3% YOY reading.

- But at the same time, the US ‘purchase managers’ index’ slipped to the lowest reading in almost a year.

- The economy in the euro-area may be weakening.

- Even with interest rates at and below zero, Japan cannot trigger inflation.

Clearly, it’s a mixed bag out there. The US economy looks pretty solid … but are storm clouds forming on the horizon? Read on, my friends, read on.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will continue to be true for years to come.

Is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is almost $80 trillion today. US ‘current dollar’ GDP almost reached $20 trillion during Q1, 2018. We remain about 25% of global GDP. Other than China — a distant second at around $11 trillion — the GDP of no other country is close.

The objective of the SHI10 and this blog is simple: To predict US GDP movement ahead of official economic releases — an important objective since BEA (the ‘Bureau of Economic Analysis’) gross domestic product data is outdated the day it’s released.

Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric.

The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

Earlier in the year, global economic growth seemed synchronous. This may be changing.

Perhaps not here in the US. But overseas.

Earlier today, the Federal Open Market Committee (FOMC) at the FED made the decision to leave interest rates alone. No increase. The press release included this comment:

“In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments…. The actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.”

No, this is not different from the last press release. But today, international developments may be more important. Why?

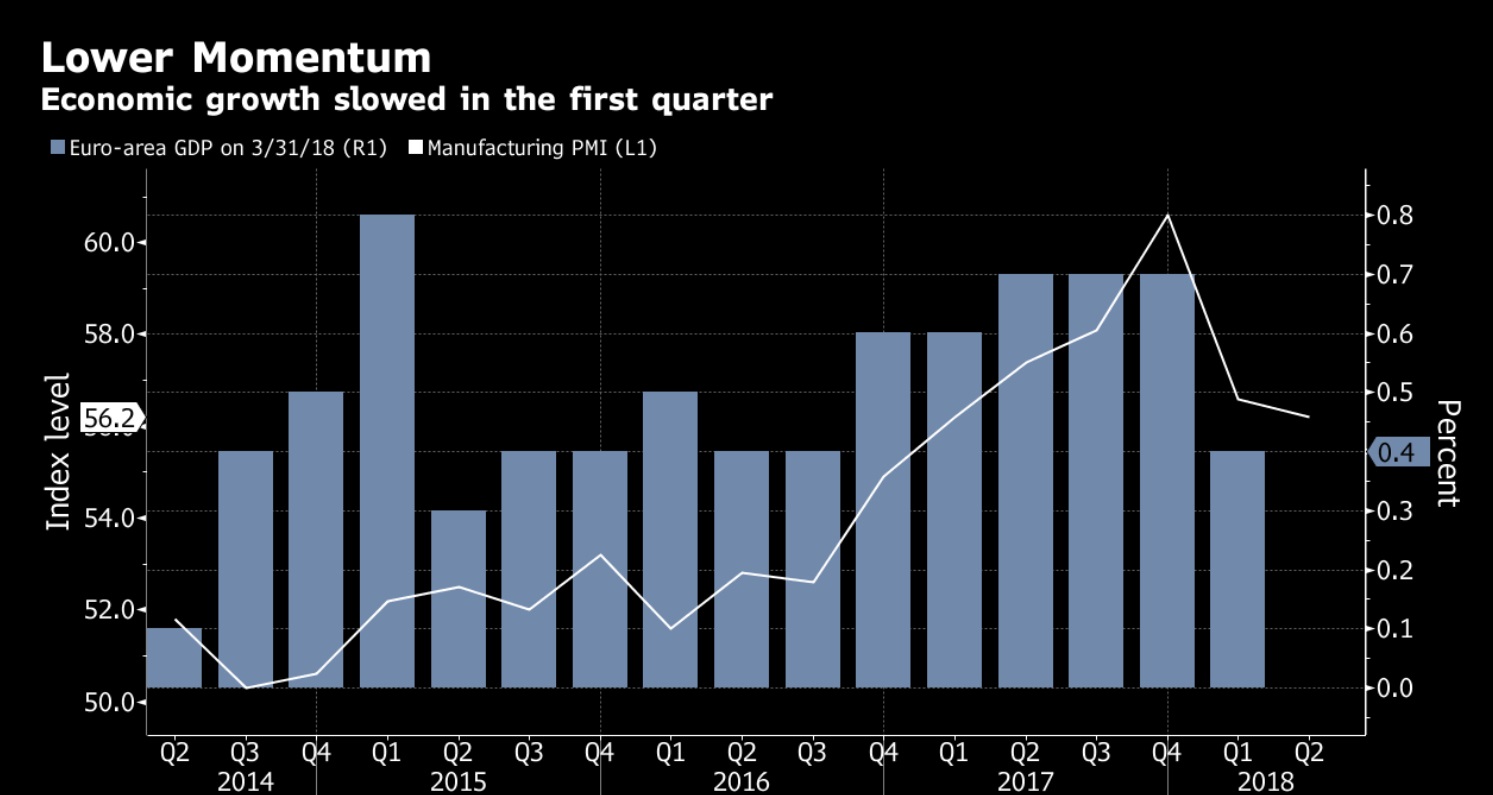

The headline from this Bloomberg article says it all: “Euro-Area Factories Fret About Euro as Economic Growth Cools.”

Q1, 2018 GDP for the euro-area slipped down to only 0.4% — down from 0.7% in the prior quarter. And, at the same time, the manufacturers ‘Purchase Managers’ Index‘ , or PMI, slipped a bit further. In January, one euro cost about $1.05 — today, it cost about $1.20. That increase is hurting euro exports.

This chart tells the euro-area story:

By comparison, GDP growth in the US was solid during the first quarter. According to the Bureau of Economic Analysis (BEA), our annualized real GDP growth rate was 2.3% — about 0.7% higher than the SHI10 and I had forecast last week.

In the first quarter, “Net Exports” added about 20 basis points to GDP growth. But the big “add” to growth was in “Fixed Investment” and the construction of new “structures” and “equipment.” These two segments, combined, added 76 basis points to GDP growth. And this makes sense. Have you looked around lately and seen all the construction cranes? Commercial development is booming.

But in spite of a ‘short term’ rate of negative 0.1%, and a 10-year bond with a zero yield, Japan cannot seem to trigger inflation. In fact, the Bank of Japan just abandoned their time-table to achieve a 2.0% inflation rate. Even with interest rates at, or below, zero, and a March unemployment rate of 2.5%, Japan’s inflation rate remains very close to 1.1%. Truly a conundrum.

Especially when compared to the US where our ‘short term’ rate is 1.75%, the unemployment rate is 4.1%, and our ‘core’ PCE inflation rate is very close to the FEDs 2.0% target.

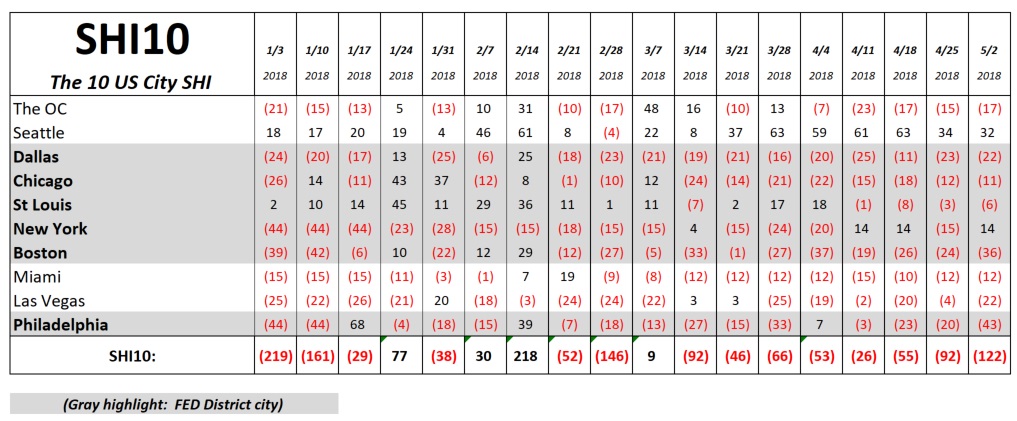

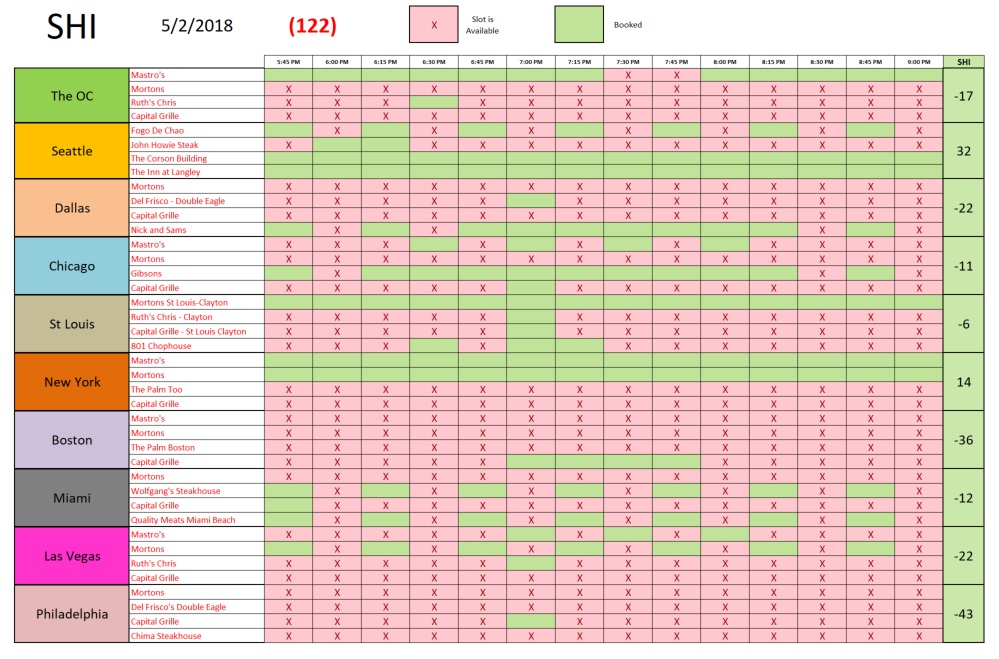

And finally, even our opulent eateries are also showing a bit of sluggishness. Take a look:

This week, demand for reservations in our SHI10 steak houses remained the same, or fell, in every market except NYC. Here are the weekly results:

New York steaks from Mastros and Mortons are HOT in NYC this week! And, of course, Seattle continues to be a bright spot for expensive steak consumption. But without exception, piping hot T-Bones are not in favor in the balance of our SHI10 markets this week.

Personal consumption expenditures, or PCE, were responsible for adding 73 basis points in growth during Q1. But as we peel back a layer and look a bit deeper, we see that the sale of ‘motor vehicles‘ subtracted 42 basis points. Ouch. Personal spending on “services‘ was the bright light during Q1, adding almost 1% of the 2.3%.

But “goods” aren’t selling well. This week’s SHI10 suggests the trend continues. Consumer demand for “stuff” is at a low ebb. Auto sales are not too bad: April sales were at an annualized rate of 17.5 million, just down slightly. But “residential fixed investment” — meaning new home construction and home remodeling — added nothing to Q1 GDP.

The Trump administration tax cuts and repatriation are definitely economic tailwinds. Q1 GDP growth is notoriously at the low end of range. I suspect we’ll see a good GDP growth bounce in Q2 from both the tail winds, continued strong construction activity, some exports, and tepid consumer spending. We have enough momentum to carry us for a while.

But otherwise, it’s a mixed bag. The economic storm clouds are forming — waaaaaaaaay out on the edge of the horizon. The signs are there.

– Terry Liebman