SHI 6.17.20 – The Beef Index

SHI 6.10.2020 – Goodbye Old Friend

June 10, 2020

6.24.20 – Positive Pecuniary Externalities

June 24, 2020

Buy, Buy, BUY! No, I am not paying homage to the *NSYNC song … I’m simply saying that stuff is selling! All kinds of stuff!

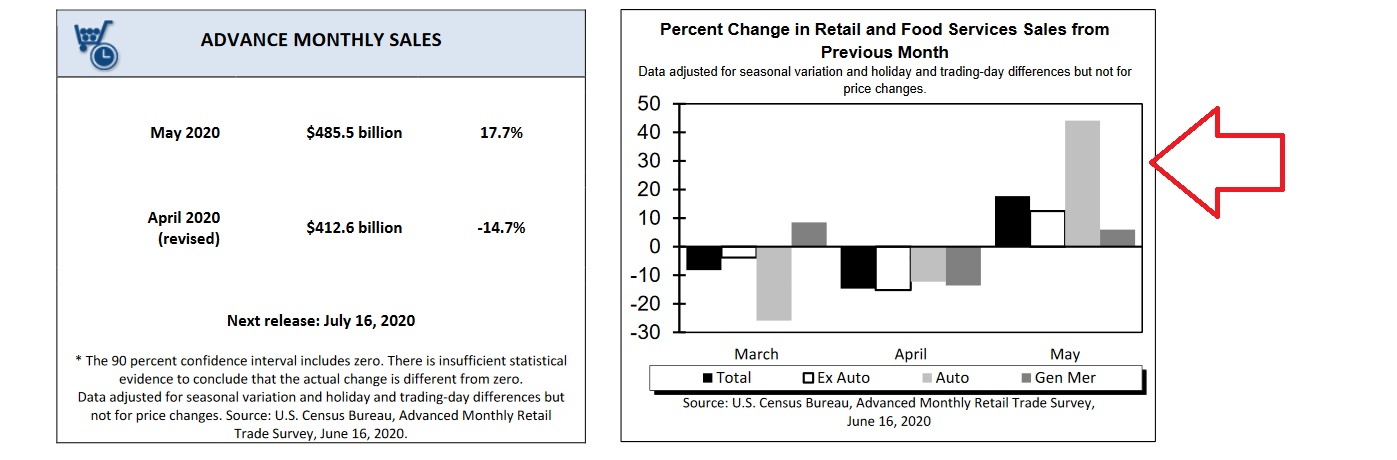

- Overall, retail sales were up 17.7% in May – more than double economist estimates.

- This week, the FED has begun a program to buy $750 billion in corporate bonds.

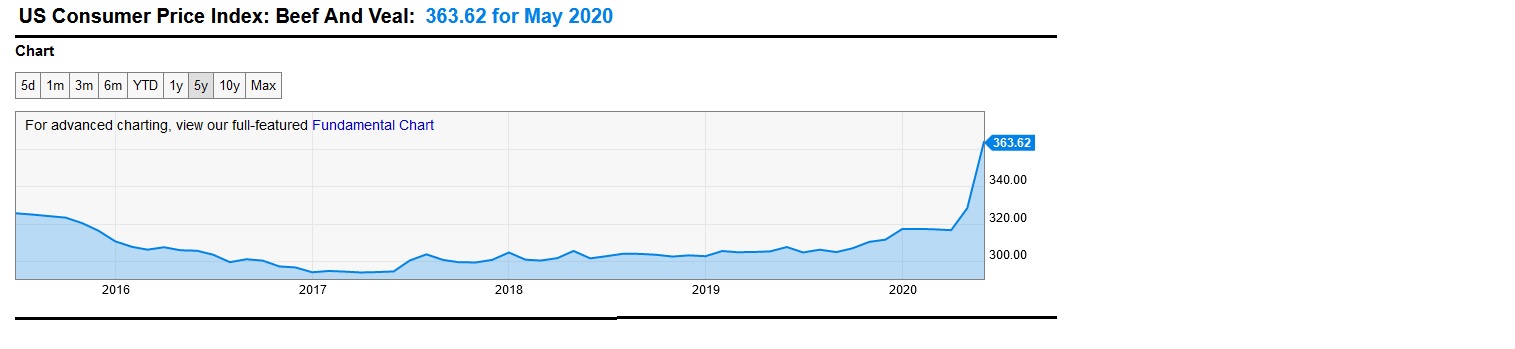

- Meat prices were up 10.8% in May. The “beef index” experienced its largest-ever monthly increase!

- Finally, a watermelon sold for $2,000 at a Japanese auction!

Yes, it’s true. There really is a beef index. And, yes, that really is a $2,000 watermelon. I don’t make this stuff up.

The beef index is tracked by the Bureau of Labor Statistics, within the CPI itself. And like the US stock markets, beef is up!

” Where’s the beef ? “

Right now, it’s in your kitchen. What does that mean?

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Before COVID-19, the world’s annual GDP was about $85 trillion today. No longer. It will shrink thanks to ‘The Great Lockdown.’ I did not coin this phrase — the IMF did. The same folks who track global GDP. Until recently, annual US GDP exceeded $21.7 trillion. Again, no longer. But what has not changed is the fact that together, the U.S., the EU and China still generate about 70% of the global economic output.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

At long last, the Steak House Index is laser focused on steak once again!

Alas, not in restaurants, mind you, this time we’re talking about steaks-at-home. It will come as no surprise that mandatory “sheltering in place” has caused a food price surge. And beef saw one of the largest price increases. The ‘Beef Index’ is up significantly:

Beef price increases, of course, are not entirely demand generated.

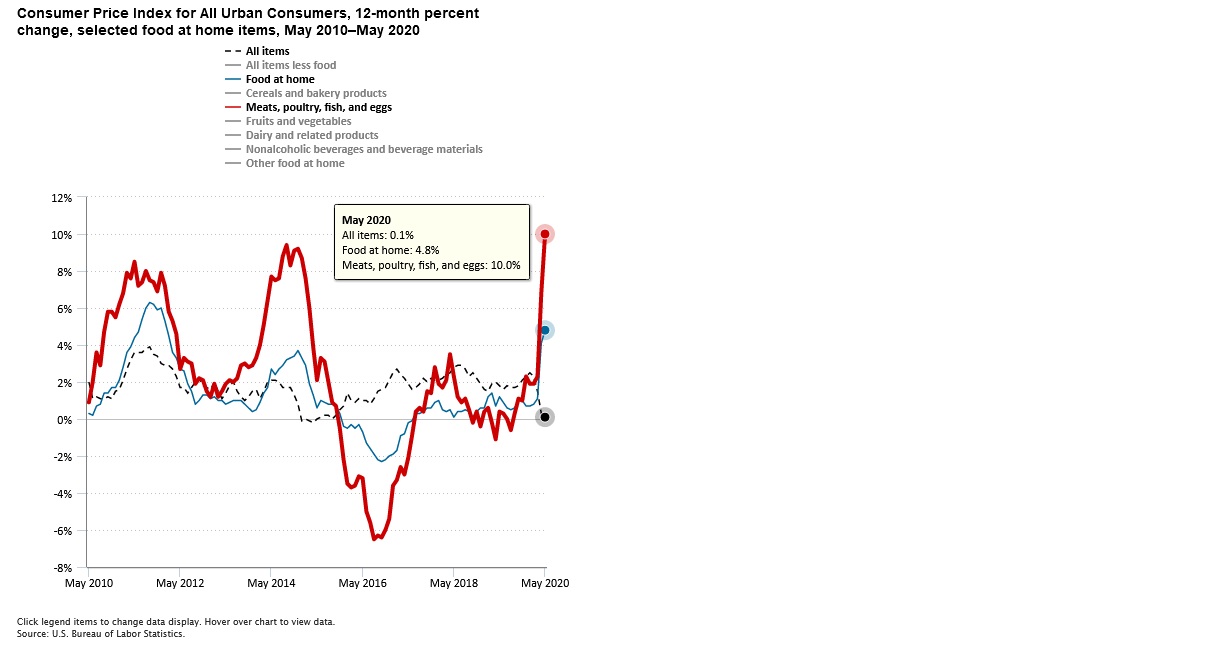

Supply has been curtailed by processing plant closures, the result of CV-19 spreading within their walls. We’ve seen processing plant closures across the US, helping push the beef index to all-time highs. Both increased demand and supply constraints have caused prices to rise in all groups of “food at home.” In the May CPI figures, food prices increased 4.8%:

The divergence of the three (3) lines in the CPI chart above is both obvious and stark. Meats and dairy are up significantly month-over-month. Food, in general, is up quite a bit. And yet we see the aggregate CPI in May was almost flat — we saw a 0.1% decline in prices during the month — and a paltry 0.1% year-over-year price increase. Digging deeper into the numbers, we can see that ‘energy’ counterbalanced food cost increases during May. Overall, energy costs were down 18.9% for the month … and gasoline was down 33.8% from the prior month. So, steaks were up, general prices in the aggregate were flat, and energy costs were down significantly.

Retail sales increased 17.7% in May over the prior month, following a 14.7% decline in April and a smaller overall decline in March. Take a look at this image:

That’s a “V” recovery in Retail Sales right there, folks.

“Advance estimates of U.S. retail and food services sales for May 2020 were $485.5 billion, an increase of 17.7% from the previous month, but 6.1% below May 2019. Total sales for the March 2020 through May 2020 period were down 10.5% from the same period a year ago. The March 2020 to April 2020 percent change was revised from down 16.4 percent to down 14.7%. Retail trade sales were up 16.8% from April 2020, but 1.4% below last year. Non-store retailers were up 30.8% from May 2019, while building material and garden equipment and supplies dealers were up 16.4% from last year.”

Note the acceleration of the retail sales shift to ‘on-line’ channels. ‘Retail trade’ sales were down 1.4% from last year … but the sales at ‘non-store’ retailers were up more than 30% over one year ago. On line sales, for obvious reasons, have gained traction during the pandemic lockdown. This comes as no surprise. What you may find surprising is the fact that retail sales increased at all, given the fact that millions of hard-working folks are now unemployed. Almost 21 million, to be precise, according to the May numbers from the US Bureau of Labor Statistics. How can May retail sales numbers improve when 21 million people are unemployed?

Fiscal stimulus is the answer. For the moment, at least, the $1,200 stimulus checks and the federal unemployment supplemental payments, when paired with state unemployment benefits, have replaced income lost from unemployment. Not for everyone, of course, as the system is neither perfect nor perfectly implemented. But in the aggregate, lost income has been replaced by stimulus payment. Interestingly enough, not only have Americans, in the aggregate, decided to buy, buy, buy … but they’ve also decided to save, save, SAVE! April saw the largest increase in the personal savings rate since this metric was first introduced back in 1959:

Personal savings is measured as a percentage of “disposable personal income,” or DPI. What is DPI? It’s the money a person retains after taxes and other mandatory withholdings are taken from a paycheck. In April, Americans saved 33% of their disposable income. The stimulus checks, as it turns out, have no withholding for taxes. In fact, this stimulus checks represent tax-free income. Neither state nor federal taxes need be paid. It is not considered taxable income. This fact most certainly helped boost the savings rate in April. It would appear Americans can save quite bit if they don’t have to pay taxes. 🙂

What about those $600 weekly supplemental federal unemployment benefits? Are those taxed? Yep. It turns out they are. Sort of. It turns out the recipient does not have Social Security or Medicare taxes withheld or due, like on wages, but federal income taxes will be due, and perhaps state income taxes depending on the state of residence. But this fact has not been widely discussed, and so many recipients of the supplemental $600 weekly may not be aware they will owe 2020 income taxes on these funds in 2021. Ouch. But for now, anyway, personal savings rates are way up.

Let’s review:

- Retail sales: UP

- Personal savings: UP

- Beef: UP

Also UP is the size of the FEDs balance sheet. And growing. On Monday, the FED said they are extending a $750 billion “emergency lending program” which will consist of corporate bond, purchased in the open market, from companies that meet the FEDs standards. Interestingly, the FED has kicked off this program in advance of any discernible need. They announced their plan to create the program some time ago. And, in response, the corporate bond markets stabilized and have been working quite well for a number of months now. Powell, it appears, is implementing the program to ensure the markets know that a commitment from the FED is a commitment fulfilled. And so the FED will buy, buy, buy. Remember, the FED already owns assets totaling almost $7.2 trillion. 🙂

Investors, too, are sitting on a pile of cash. Apparently, most investors don’t read my blog. Despite the fact that many yields are close to zero, according to the Wall Street Journal money market funds recently grew to about $4.6 trillion, the highest levels on record.

With all this new money sloshing around the system, should we be concerned about an inflation spike? In my opinion, no. Not now and not for the foreseeable future. Stimulus payments to Americans, in all forms, somewhat replace income lost by unemployment. Corporate borrowing has increased to replace income lost in the Great Shutdown. In both cases, the excess liquidity is more income replacement than growth in money supply. Today, frankly, I feel we should be more concerned about deflation.

The picture at the top of this page is of a $2,000 watermelon. That’s right. $2,000. And while that is an absurd price to pay for a watermelon, consider this:

- This watermelon is a ‘prized Densuke watermelon‘ grown in northern Japan, sold at the season-opening auction.

- The price is down more than 70% from last year’s price.

We can conclude two things from this auction. First, Japanese watermelon-lovers are nuts. Second, even crazy people will pay less for something when they can. Japan has already re-entered a deflationary economy. This in spite of the fact that Japan has not been hard-hit by Coronavirus, is paying nearly $1,000 in cash to every Japanese citizen, is giving tens of thousands of dollars to businesses, all financed by new government debt that the central bank of Japan has pledged to buy in “unlimited quantities if necessary.”

Per one Japanese economist at Mizuho Securities:

“Consumers will start to get used to buying at low prices once they experience it. They would think, ‘I should probably wait until a sale because the shop had one before.’”

And that’s the problem with deflation. Japan has struggled with this demon for years. The US have to make sure it doesn’t take root here. This, I believe, is the FEDs greater concern today.

We have no shortage of concerns today. But fear of inflation should not be on that list. In spite of rising steak prices. 🙂

– Terry Liebman