SHI 7.27.22 — So? Which Is It?

SHI 7.20.22 – Gone Fishing

July 16, 2022

SHI 7.30.22 — Oops!… I Did It Again

July 30, 2022

The FED raised interest rates again today, intending to slow the expansion rate of our economy.

Earlier today, they raised rates by 75 basis points – lifting the federal funds rate up to about 2.5%. It’s worth commenting that just six months ago, the fed funds rate was close to zero.

A few weeks ago, FED Chair Jerome Powell said the US economy was in “strong shape.” Other FED words used to describe of the current state of our economy include:

- very strong

- overheated

- soaring inflation

- strong labor market

- solid consumer spending

Meanwhile, at the same time, many economists are talking recession. Many suggest we are already in a recession. As you know, when in a recession, our economy shrinks. Many think it is shrinking now – and has been for all of 2022. GDP growth in Q1 was negative. Tomorrow morning, at 5:30 AM (PST), we’ll find out if GDP growth in Q2 was negative as well. In theory, when our economy shrinks two quarters in a row, we are in a recession.

“

Is our economy growing or shrinking?”

“Is our economy growing or shrinking?”

So? Which is it? Is the economy super strong, expanding, overheated and out of control? Or is the economy already in a recession, shrinking right now, with GDP contracting?

Both cannot be true simultaneously. Our economy cannot be strong and growing at the same time it is shrinking. Think of it this way: You cannot gain weight at the same time you lose weight, right? At any moment in time, only one condition can be factual.

Or can it? Can our economy be expanding and contracting, simultaneously?

Perhaps.

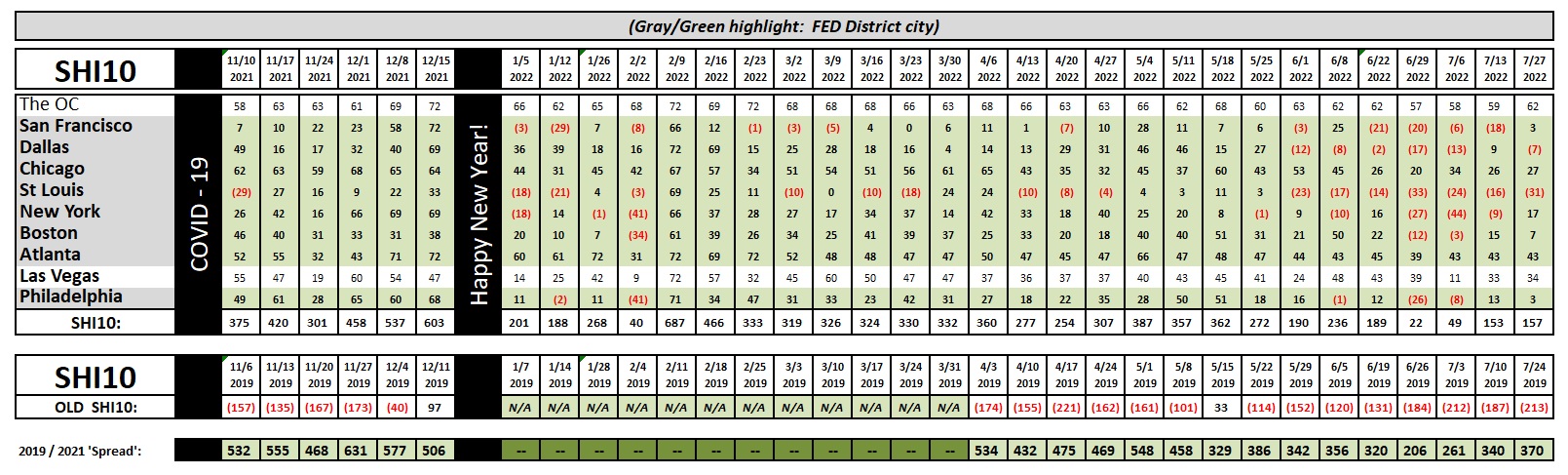

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. Sort of. We’ll have a better indication tomorrow. 🙂

At the end of Q1, 2022, in ‘current-dollar’ terms US annual economic output clocked in at $24.38 trillion. Yes, during Q1, the current-dollar GDP increased at the annualized rate of 6.5%. The world’s annual GDP rose to about $95 trillion at the end of 2021. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

Mark Twain purportedly quipped: “There are three kinds of lies: Lies, Damned Lies, and Statistics.”

Let’s talk about statistics. The problem with statistics isn’t that they lie per se … but you have to read the fine print. The proverbial devil is in the details. For example, consider GDP statistics. They have been compiled, using consistent methodology, by the Bureau of Economic Analysis (“BEA”) since 1947. That’s 75 years, folks. 300 quarters. That’s a long time of consistent, quarter-over-quarter analysis.

And in every one of those 300 quarters, the BEA hasn’t reported only one GDP number. No, they have consistently reported two GDP numbers: The “real” GDP number … and the “nominal” GDP number. I’ve talked about both statistics in many of my blogs.

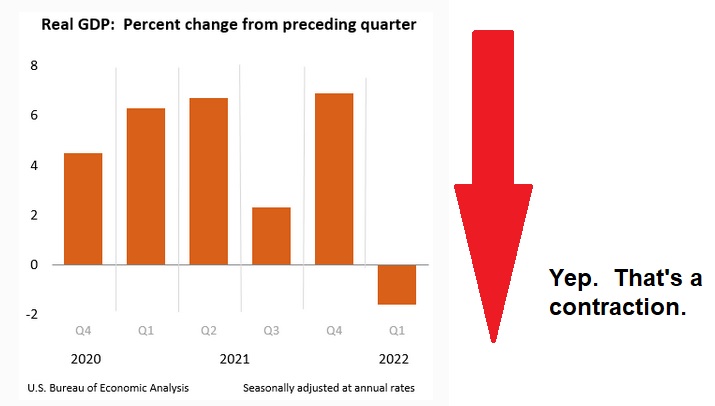

Yet, the only number generally discussed by pundits is the “real” GDP result. Even the BEA generally ignores the “nominal” GDP number. Case in point: I sourced the graphic below directly from the latest BEA report. Note the first word in the title:

“Real” is that first word. Clearly, by this graphic, it’s easy to see that GDP is contracting. Real GDP decreased at the annual rate of 1.6% in the first quarter. But if you read the entire report, about ½ way down the second page, you’ll find this:

“Current‑dollar GDP increased 6.6% at an annual rate, or $383.9 billion, in the first quarter to a level of $24.39 trillion.”

So, while the “real” economy shrunk in the 1st quarter … the “nominal” economy grew – substantially. So the debate over whether the economy is growing or shrinking – or doing both simultaneously – is a real debate. And in this immediate case, I’m using “real” to mean “valid.” While the FED assiduously ignores the nominal, or “current dollar” figure in their analysis, when they say the economy is overheating, they’re giving a nod to the nominal number. And employment. The FED is laser focused on employment figures. And when the media and economists opine that we are in a recession right now, they are focused on only the real number. Which is to say, not the nominal number. Confused? You may as well be. Experts seem to be equally flustered.

So? Which is it? Is the economy growing out of control – justifying the FEDs relentless rate increases? Or is it shrinking precipitously, as the “real” GDP numbers show, suggesting that the FED and other central banks around the world are over reacting?

Can I pick “C”? All of the above?

Sure. Let’s pick C. The BEA is not “lying to us” when they say the economy shrunk in Q1, nor am I “lying to you” when I say the economy grew in Q1. Both are true…all depending on your statistical viewpoint. And remember:

Almost 80 central banks across the globe are raising interest now.

And in every case, they use inflation, and an overheated economy, as the reasons justifying the rate increases. Let me repeat that: Almost 80 central banks are acting in unison, all raising rates.

Hmmm. That’s interesting. Are there any conspiracy theorists out there? Yes? Would you be interested in joining my conspiracy club? Well, if you’re on the fence, consider the answer to this question: Could it be that the FED and other central banks across the globe are using the phrases ‘run-away economy’ and ‘rampant inflation’ as a smoke screen?

A smoke screen, you ask? For what? Ahhhh… good. Finally. We are finally asking the right question.

The Bank for International Settlements (“BIS”) has 63 members. Each member is a central bank of a country. Here’s a list (right click, open a new tab):

https://www.bis.org/about/member_cb.htm

Is the first member on the list, the central bank of Algeria, raising rates right now? Nope. Ironically, it turns out they are not. But really, do we give two hoots about Algeria — economically speaking? Naaa…. Elon Musk’s net worth exceeds their annual GDP. ?

But Argentina is raising rates. Even though their official interest rate is now about 52%. Wow. And so is Austria, Australia, and just about everyone else on the list.

So why is every major central bank raising rates right now … when the US and other economies are flirting with recession and contraction? Could one reason be to reset global interest rates? Remember, it wasn’t that long ago when trillions of dollars of sovereign debt sported negative yields. And remember: The ECB only recently raised their interest rate from a negative .75% to get to zero. Call me a conspiracy theorist, but I believe one (1) reason most BIS members are raising interest rates is to reset global rate levels — above zero.

Of course, the other stated reasons are valid, too. Which is to say they are real. 🙂

Raising rates will ultimately help stabilize price pressures across all major economies. Of course, raising rates may also tip the world into recession and cost many their jobs. But hey … no pain, no gain, right?

Perhaps. Let’s head to the steakhouses.

Some improvement this week! Well, not really. But today’s reading is quite a bit better than a few weeks ago. Reservation demand firmed in San Francisco, softened slightly in Dallas, and remained identical in Atlanta. A mixed expensive eatery bag.

OK … I’ll end here. Be sure to watch CNBC tomorrow morning — 5:30 am sharp. Q2 GDP numbers will be hot off the grill — oops, I meant “the press.” Sorry. Here at the Steak House Index, we get carried away sometimes.

<:> Terry Liebman