SHI Update 11/16/16: Trumpflation!

SHI Update: President Trump

November 9, 2016Trumponomics vs. Reganomics

November 19, 2016Wow. One week ago today, we learned Trump is our new president. And the financial markets went crazy! In four business days – Wednesday thru Monday – we experienced the entire 4 years of the Trump presidency. The DOW reached new highs … and global interest rates skyrocketed. What the heck is going on?

Welcome to this week’s Steak House Index update.

As always, if you need a refresher on the SHI, or its objective and methodology, I suggest you open and read the original BLOG: https://terryliebman.wordpress.com/2016/03/02/move-over-big-mac-index-here-comes-the-steak-house-index/)

Why You Should Care: The US economy towers over all others: our GDP is over $18.5 trillion a year. Is it growing or shrinking?

The objective of the SHI is simple: To predict the direction of this behemoth. But while the objective is simple, the task is not.

BEA publishes GDP figures the instant they’re available. Unfortunately, it is a trailing index. The data is old news; it’s a lagging indicator. We know how the economy is doing in advance of the GDP release.

Personal consumption expenditures, or PCE, is the single largest component of the GDP. In fact, the majority of all GDP increases (or declines) usually result from consumer spending. Thus, this is clearly an important metric to track.

I intend the SHI is to be predictive, anticipating where the economy is going – not where it’s been. Thereby giving us the ability to take action early. Not when it’s too late.

Taking action: Keep up with this weekly BLOG update. If the index moves appreciably – either showing massive improvement or significant declines – indicating expanding economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG: Our new president is impressive: Not yet in office, he was able to move interest rates up higher and faster than the FED! I commented in last week’s BLOG the 10-year Treasury had passed the 2% mark only 12 hours after the election; today, we find ourselves another 1/4% higher! Was I wrong when I suggested the bond market would settle down…and rates would head lower once again?

Perhaps. As with most predictions, we’ll know soon enough. But I’ve got Bloomberg on my side: The RSI – shown below – suggests the 10-year treasury is quite oversold:

The ‘Relative Strength Index‘ is a momentum oscillator. Suggesting the present always reflects some semblance of recent past movement. The RSI does not always accurately predict the future – but it does help identify market surges or drops that are inconsistent with overall market conditions. And right now, it’s telling us bond sellers are acting irrationally. I remain steadfast: Yields will come down again. 🙂

The yield spike is impressive when we consider the election was only a week ago. It does prove the power of rhetoric. Consider this from a Financial Times article on the 14th:

“The market value of bonds within the Bloomberg Barclays multiverse index, a broad index that includes corporate and sovereign bonds, has fallen by $1.5 trillion since Donald Trump unexpectedly won the US presidency in elections last week.”

Ouch. Amazing. Sure, I’ve been commenting for months bond buyers are nuts accepting today’s low and negative yields. Consider my ‘Greater Fool’ Blog: https://terryliebman.wordpress.com/2016/06/14/the-greater-fool-theory/

But Trump’s election, in itself, does not change the global imbalance between the supply of, and demand for, capital. https://terryliebman.wordpress.com/2016/10/02/a-race-to-the-bottom/

It is entirely possible the US deficit will increase under a Trump presidency. Whether due to fiscal stimulus or tax cuts. Throw in a budding medicare and Social Security budget, and we have a recipe for a growing national debt.

But we have to assume some degree of sanity here. On the part of Trump, the Congress and the Senate. Any deficit – thereby increasing US debt – will have to be discussed, considered and agreed to by all 536 of our legislators. I contend any US Treasury supply increase during Trump’s presidency will be readily absorbed.

Don’t forget the other side of the equation: A reduction in government regulation. I have no doubt Trump’s cabinet will work energetically to reduce red-tape, embodying the thoughts and words of Mr. Mori, (review: https://terryliebman.wordpress.com/2016/08/03/japan-warning-dont-step-in-a-bear-trap/) ushering in the potential for greater GDP growth. Increased growth means an increase in American’s wealth, larger tax collections, and a possible reduction in the deficit.

Finally, the Trump win has no effect whatsoever on the underlying macro-economic condition Larry Summers, Ben Bernanke and friends call ‘secular stagnation’. (http://larrysummers.com/2016/02/17/the-age-of-secular-stagnation/)

This theory suggests our advanced economies have a serious problem. Their economic successes of the past 100 or so years have created great wealth. Wealth and capital are inherently risk averse. Thus, advanced economies find their populations now have an increased desire to save (low risk) and a decreased will to invest (high risk). This theory suggests excessive savings ultimately reduces consumer demand, GDP growth, inflation, and drives down interest rates.

So it appears we have a fight on our hands: In one corner, we have the challenger, the new guy, the unknown, Trumpflation! … and in the other, the Champ, the known, Secular Stagnation.

Who will win? At the moment, it looks like the markets are betting against the Champ. Trumpflation! they say! But its early in the fight. Frankly, we haven’t even started Round 1.

I suggest we settle in, relax, and enjoy some refreshments while we watch. Ready for a steak? Good … so am I.

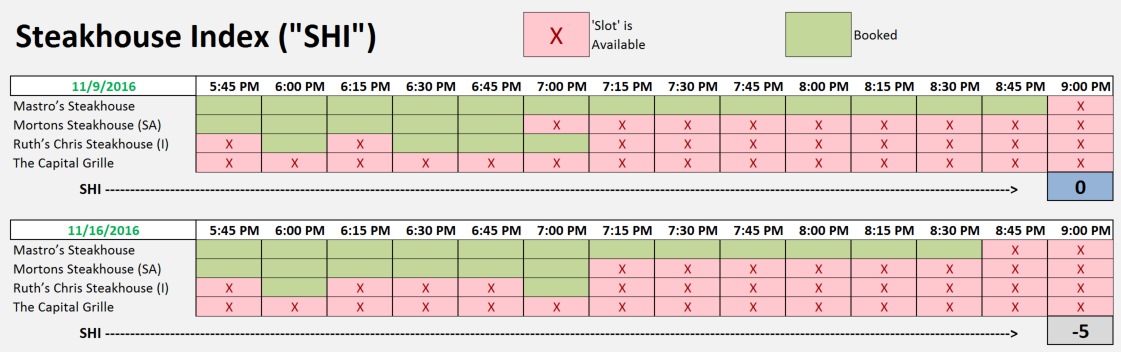

But a few less folks have booked tables this week. Not many … but unlike past weeks when Mastros was fully booked, right now we can get a table for 4 this Saturday at 8:45. Per opentable.com, by 11 am today, 132 parties have already booked a table at Mastros. The other players are more or less the same as last week. Here is the updated SHI chart:

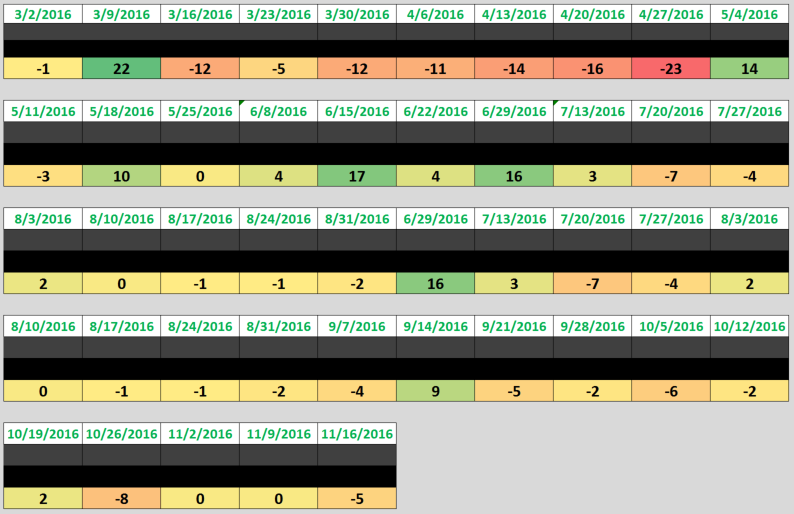

And here is the updated SHI trend since inception:

Remember: We’re using the same methodology we started with on March 2. Which suggests the recent lack of volatility – look at the top line – suggests an underlying stability in consumer demand for high dollar steaks. You could argue this week’s negative (-5) SHI reading seems to counter to the overall euphoria we’ve seen in the markets. But it’s really too small a move to derive any meaning.

Yet again, this week the SHI is suggesting consumers are happily spending their hard earned money on expensive steaks and bottles of wine … and our economy remains on sound footing.

And rest assured, we’re going to keep a close eye on Trumpflation!

- Terry Liebman