SHI Update – June 22, 2016

The Physics of Economics, Part 3

June 20, 2016The “Big Game” is Over. Who Won?

June 24, 2016I can think of nothing better than eating a thick, juicy porterhouse while watching the big game.

Which game you ask? Oh … the one in the UK … the BRexitians vs. the BRemainers. Who will win? Will the UK remain in the EU or will they go solo…making their way in the world all by themselves? Well, tomorrow is the day! So stay tuned!

For today, let’s update the SHI. Is Mastros still fully booked … still leading the race? Has the Capital Grille finally moved into second or third place? The drama and excitement are downright palpable!

And, as always, if you need a quick refresher, take a look at the original blog: https://terryliebman.wordpress.com/2016/03/02/move-over-big-mac-index-here-comes-the-steak-house-index/

Why you should care: The US Department of Commerce ‘Bureau of Economic Analysis’ publishes the most recent GDP figures the instant they’re available.

Here’s the problem: GDP numbers are not proactive … we seem them months after economic events have occurred. Which means we can’t make financial/investment choices – personal or business – before the economy turns sour … only after.

Not good. We want advance notice of an economic decline. The SHI may help give you that. Our objective with the SHI is to be predictive, to anticipate when the economy is going to ‘turn’ and give you the ability to take action early – not when changes are too late.

Taking action: Just keep up with the weekly column. If the index changes appreciably – either showing massive improvement or significant declines – indicating expanding economic strength or a potential recession, we’ll discuss possible actions at that time. Trending is very important…and we’ll watch the trend.

THE BLOG: Once again, unless you’re OK with a 9:00 dinner reservation, you should have booked Mastros Ocean Club earlier in the week. Because there’s nothing else available today. And yet again, the Capital Grille is the ‘Rodney Danderfield‘ of our high-dollar steakhouses: ‘I don’t get no respect!’

You’re not familiar with Rodney? He was a funny guy … we lost him back in 2004. Very funny guy. He’d say things like, “I could tell that my parents hated me. My bath toys were a toaster and a radio.“ 🙂 So sad for the Capital Grill … so sad. 🙁

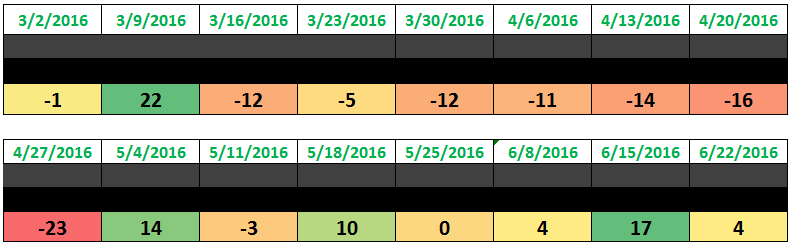

Mortons (SA) and Ruth’s Chris (I) make up the ‘middle of the pack‘ and both have spotty availability before 7:45 pm, unlike last week when both were booked solid thru 7:15. Regardless, this week our SHI is a solid positive 4. Identical to the reading only 2 weeks ago:

An SHI reading of 4 is still quite strong. Take a look at the conditional formatting in the chart below…where dark green is the best (highest) and red is the worst (lowest) SHI reading:

So, once again, the SHI tells us the economy remains on solid footing.

In the SHI update a few weeks ago, I talked about the contributing components of the GDP. What, specifically, contributes to the total figure. Here was that blog:

I think it bears repeating that GDP activity occurs in four major categories:

In the latest BLS release on May 27th, they reported that the 2016: Q1 GDP “seasonally adjusted in annual rates, in billions of dollars” totaled $18,229.5. Here’s how each of the four major categories added into the total:

- Personal Consumption Expenditures (PCE) – $12,513.8

- Investment – $3,009.8

- Net Exports – ($506.8)

- Government Expenditure – $3,212.7

As I discussed in that blog, the SHI is intended to be directly correlated with PCE. Which is where the vast majority of GDP growth occurs. However, it doesn’t tell the whole story. For this reason, in next week’s blog, I’ll be creating and adding another index, one I feel might offer even greater insight into our GDP forecasting.

It will be named the ‘Steak House Composite Index‘ or the SHCI for short. It will be a composite of three economic health barometers, each drawing from a different perspective. In that regard, I feel it will be another ‘arrow in the quiver‘ so to speak, a multidimensional view of the same question: How strong is the US economy?

What, specifically, will the SHCI include? First, the Labor Market Conditions Index and a really great, really deep view into the US labor market prepared by the FED, pulled and assimilated from 19 labor market indicators. I’ll talk more about this later in the week. The second will be a US Treasury ‘Yield Curve’ view – specifically the moving spread between the “10-year CMT” and the “3-Month CMT“.

The FED updates the LMCI monthly, the first business day after the BLS releases their update on the ‘Employment Situation’. So, the SHCI follow the same schedule.

So, to recap, the SHI will continue to be released weekly. The SHCI will be a monthly index release. Make sense?

I’ll explain more next week….until then, stay hungry my friends! And have a great day!

- Terry Liebman

1 Comment

[…] https://terryliebman.wordpress.com/2016/06/22/shi-update-june-22-2016/ […]