Steak House Index Update 8/31/16

Savings UP … while Rates are DOWN? What’s UP with that?

August 26, 2016The Jobs Report

September 2, 2016Another week means another steak! Grab your knife and fork…and let’s dig in!

Some may be surprised to learn that the FED – the Federal Reserve banking system – was not established until 1913 – about 100 years ago.

It may also surprise you to hear the FED is not our nation’s first ‘central bank’. The first was The Bank of the United States, chartered in 1791. For numerous reasons, it’s congressional charter was not renewed forcing the bank to close in 1811. A Second Bank of the US was established 5 years later, but it too ultimately closed in 1836.

The “Panic of 1907” was especially severe, ushering in one of the worst depressions in our country’s history. With no central bank to battle rapidly spreading fear and economic calamity, the infamous J.P. Morgan stepped in. He personally made temporary loans to key New York banks and other financial institutions to keep them liquid and weather the storm.

In the aftermath, both Wall Street and Washington agreed the US needed an institution able to provide emergency liquidity to the banking system if, and when, another ‘panic’ struck. The final result of the Panic of 1907 would be the Federal Reserve Act of 1913.

The FED was born.

Why You Should Care: Love ’em or hate ’em, today the FED is the most powerful financial institution on the planet. Without exception. Their actions have epic implications; their words move global markets.

Friday morning, we’ll get the next installment in the employment saga. Today, ADP gave their forecast for non-farm job growth:

Are they right? If yes, will this push the FED closer to raising short-term rates sometime this year? And if yes, what impact might this have on the GDP, consumer spending, and – by implication – on our Steak House Index?

Taking action: Continue to keep up with the weekly column.

We’ll see how current economic events impact the SHI. If the index changes appreciably – either showing massive improvement or significant declines – indicating expanding economic strength or a potential recession, we’ll discuss possible actions at that time.

Trending is very important…and we’ll watch the trend.

THE BLOG: Along with their influence, the FEDs balance sheet is massive. On July 27th, their assets equaled $4.464 trillion. Note that’s ‘trillion’ with a T.

In fiscal 2015 (the year ending 9/30/15) US Treasury receipts reached about $3.25 trillion.

During the first 1/2 of 2016, the FED made a good chunk of money off their assets. And it contributed almost $50 billion in income to the Treasury. Annualized, that’s about 3% of the Treasury’s total revenue.

This is a huge change from 10 years ago. At the end of 2006, their total assets equaled $873 billion. And they paid the US Treasury only $29 billion that year.

US quantitative easing not only resulted in all interest rates around the globe ultimately sliding toward zero, but has had the effect of dramatically reducing the US deficit. The result of both low, low Treasury interest expense and increased FED payments to the Treasury, the deficit adding to the national debt is down about $1 trillion a year since fiscal 2009.

Why is this important? For a number of reasons. First, let’s talk big picture.

This story is not unique to the US. The same events are playing out in all developed nations around the globe. Combined, the GDPs of the US, China the European countries using the Euro, and the UK equal about 50% of global GDP. One half. The globe’s GDP is about $85 trillion. This group makes up $43 trillion of that total.

At the end of 2006, their central bank combined assets were about $4 trillion. Today, their combined total assets are almost $14 trillion.

While interesting (at least to me! 🙂) I’ve not yet explained the importance. I’ll get to that.

With the US as the sole exception, the developed nations that make up most of global GDP have economies that range between “OK” and poor. (Yes, China’s GDP growth is a robust 6% or so, but this is WAY down from prior years.) This fact is reflected is the nearly $12 trillion of sovereign bonds trading in negative territory. Japan and many countries in the Euro area are there. Long-bond rates in the UK are lower than any other time in history.

So, now let’s get to the meat of the issue: In this environment, where the US economy is effectively an ‘island’ among other average-to-per economies, can the US raise short-term rates? Even a little? Beyond a small short-term rate increase, what might be the results of this action be?

Alternatively, is the pressure to increase – even a small amount – growing so large that the FED can no longer wait?

Finally, in this environment, is lifting longer term rates off the table? If not, how might the FED – and central banks of other developed nations – affect long-term rates?

One big reason for low global interest rates is the growth in central bank balance sheets. Consider this: The size of the sovereign debt market is about $45 trillion. A big portion is now trading at negative rates:

Above I mentioned the central banks of the US, the UK, the Euro countries and China – combined – increased assets by $10 trillion in the past 10 years. They’ve all bought a bunch of debt. Not all of which was sovereign debt, but a lot was. Increased demand (government buying) had the effect of increasing price, which, of course, resulted in lower yields.

Here’s the point: The opposite could also happen. In theory.

I’m sorry, we could spend hours on this discussion! But then we might miss our steak dinner! We can’t do that.

Suffice it to say this: All things considered, I feel the FED will raise the FED funds rate once this year. My guess: In December. By 1/4%. There’s just too much talk around the potential adverse conditions of leaving short term rates too low, too long.

But they will not tinker with long term rates. The reasons, in my opinion, are numerous and compelling. I’ll talk more about this in later blogs.

For now, let’s head over to the steak houses! What are we spending on expensive steaks these days? Let’s update the SHI!

I’m not going to mention The Capital Grille this time. At all. In fact, please ignore the fact that I just did. The chart below says it all:

All in all, not much change from last week. All right, I can’t help myself: Poor Capital Grille! Mastros, of course, is fully booked. Morton’s availability is identical to last week. Fewer tables are booked at Ruth’s Chris.

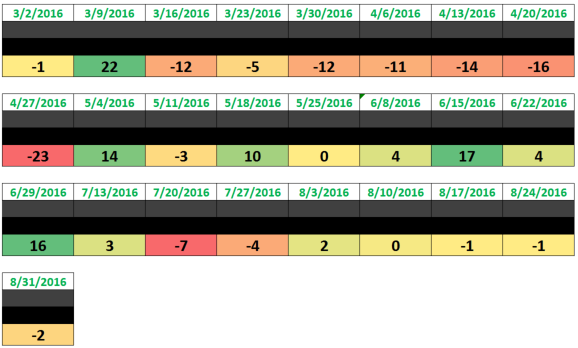

The index consistency is impressive. This week, our SHI shows a reading of negative (-2). The volatility of March and April seem to be a thing of the past. Does this suggest the SHI is a light-weight indicator – more of an appetizer than a main course? Perhaps.

But I’m more inclined to think the opposite: The SHI is simply telling us what we see all around us, both anecdotally and in the numbers. The US economy is on sound, solid footing, well supported by consumer spending. For this reason, it’s likely we’ll see a continued positive results in hiring, unemployment rates, and GDP growth.

Rest assured, there are economic headwinds. Plenty of them. Labor productivity and corporate profitability are two big ones. That we’re struggling with both at near zero interest rates is concerning.

But, for now, the SHI is telling us things are good. Not great. But good.

Here’s the SHI trending since inception:

Six weeks of very little change. The apparent stability in the index simply suggests no major change in consumer spending behavior.

As I first said last week: If, for some unexpected reason, many more tables were available, that could be indicative of a pull-back, or retrenchment in consumer spending. And the opposite is also true: If Mortons and Ruth’s Chris were fully booked and, by some miracle, time-slots at the Capital Grill were unavailable, that could indicate a sizable increase in the level of consumer spending. My conclusion is thus far: The SHI seems to be working as designed.

OK…lets leave it there for now. Let’s see what the jobs report tells us on Friday.

Eat steaks! 🙂

- Terry Liebman