The FEDs Trillion Dollar Balance Sheet

SHI Update 2/1/17: “You’re FIRED!”

February 1, 2017SHI Update 2/8/17: Occam’s razor

February 8, 2017

I’m often asked about the FED balance sheet. Usually about its large size and how a FED decision to shrink it might roil US and global financial markets.

Let’s take a closer look.

WHY YOU SHOULD CARE: Is the size of the FED balance sheet important? Yes, critically. You need to know why it’s so important to you and your finances. So read on.

TAKING ACTION: Carefully read this BLOG. Make sure you understand the contents … and if you have any questions, be sure to ask. When I summarize, toward the end of the BLOG, I will share my thoughts and opinions. If you agree, follow my recommendation. If you disagree, do the opposite. 🙂

THE BLOG: Periodically, Yardeni Research Inc updates their ‘Global Economic Briefing’ entitled Central Bank Balance Sheets. Their research and data is phenomenal and I will include a few of their graphics in this BLOG. If you wish to review the entire paper, here is a link to the latest update, dated February 2, 2017: http://www.yardeni.com/pub/peacockfedecbassets.pdf

You also may want to re-read my BLOG, “The Rise of the Central Bank” where I first talked broached this topic last year: http://wp.me/p8f7f1-or

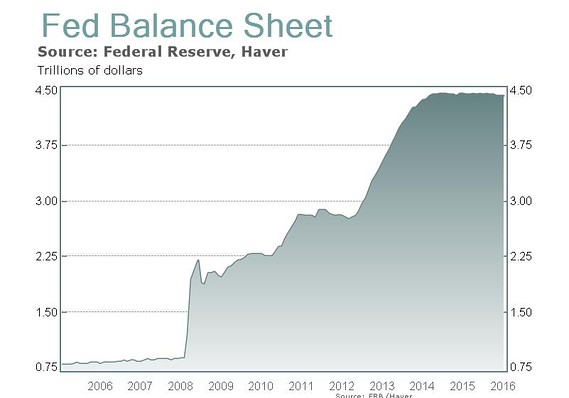

In late 2008, about the time Lehman Brothers collapsed, the FED began to dramatically increase the size of their balance sheet: FED assets grew from about $800 billion to over $2 trillion, in less than 3 months. And they didn’t stop there. Three ‘quantitative easing’ cycles later, by the end of 2015 total assets grew to over $4.4 trillion. Where it remains today.

During this same period, the central banks of Europe, Japan, and China also grew significantly. A the end of 2016, asset balances of each were:

- ECB: $3.5 trillion

- Japan: $4.2 trillion

- China: $5.0 trillion

Total assets of these 3 central banks – when combined with the FED – equal about $17.4 trillion.

Let me put this into perspective: Back in 2008, this figure was closer to $6 trillion. Thus, since 2008 we’ve seen an increase of over $11 trillion in currency and bank reserves sloshing around the globe.

Is an $11 trillion increase a meaningfully large number – when compared to the value of outstanding ‘sovereign’ bonds and ‘agency’ debt? Yes. There are close to $50 trillion in outstanding sovereign bonds and about another $6 trillion of agency (FNMA, FHLMC, GNMA) debt securities. So, dividing 11 by 56 we have about a 20% increase. Make sense? This is a statistically significant number. We’ll discuss how significant below.

Why did these countries follow the FEDs lead and purchase massive quantities of assets? For two reasons. First, for the same reason as the FED: The US exported the ‘Great Recession of 2008’ around the globe. Other developed nations needed to ‘reflate’ their economies – just as the US did. As the old joke goes, “When America sneezes, the world gets a cold.”

The second reason has to do with international currency values. When the FED increased the amount of US currency in circulation, one impact was an immediate devaluation of the USD compared to the currencies of other developed nations. This of it this way: If 100 US dollars equaled 100 Swiss Francs, we have a 1:1 relationship. But if the number of USD increased, say, to 120, now 1 SF buys 1.2 USD.

Which makes US imports cheaper in Switzerland, and Swiss exports more expensive in the US. To combat this mechanism, the central banks of every developed nation also acquired domestic assets – in the same manner as the FED.

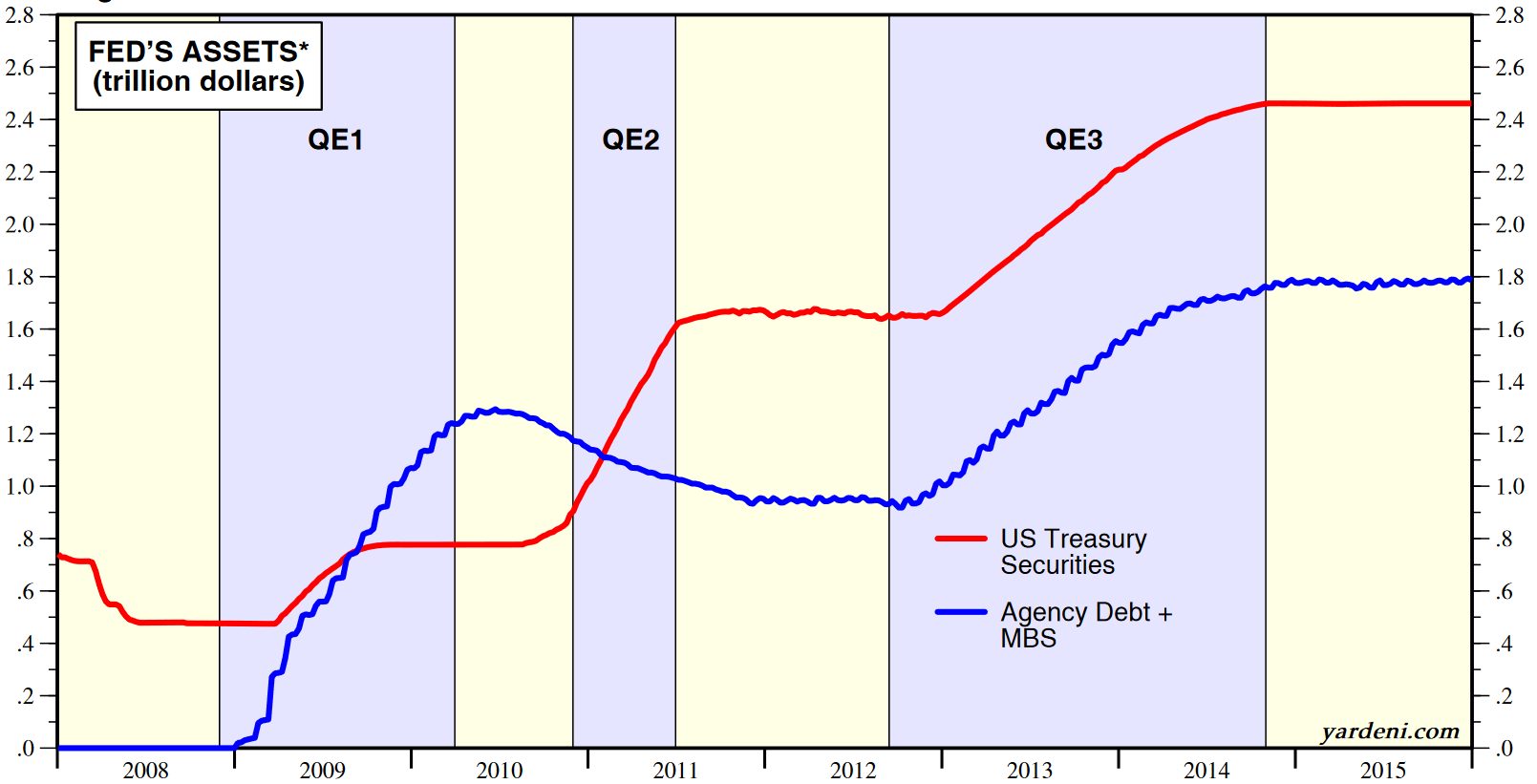

The FEDs assets are primarily US Treasury securities and securities issued by the home-loan agencies, FNMA, GNMA and FHLMC:

How does a central bank buy assets? Simple: They issue currency to the asset seller. As a result, the FED owns the asset … and the currency paid to the seller becomes a FED liability. The result of this transaction is also simple: The amount of currency in circulation increases by an amount equal to the cost of the asset.

So…on the asset side, the central bank typically owns ‘domestic’ and ‘foreign’ bonds … on the liability side, they primarily “owe” for currency in circulation and bank reserves:

When a central bank shrinks its balance sheet, it reverses their actions: It either sells the securities it owns, or when those securities mature, does not re-invest the principal into new securities. When either happens, the central bank then removes currency from circulation. Neither has happened since 2014. The FED has not sold securities it owns, and the proceeds from any maturing security have been reinvested. As a result, assets on the FEDs balance sheet have remained consistent near $4.4 trillion.

Has the FED made a decision to shrink their balance sheet? No. Sure there’s talk about it – as there should be. But nothing I’ve seen or heard indicates any serious intent to shrink their balance sheet.

And this is a very important distinction, because if handled poorly, the potential for market disruption is staggering. In his recent blog, Ben Bernanke comments on precisely this issue, suggesting “policy communication will be made easier and the risk of market disruption minimized if the shrinkage of the balance sheet, once it begins, is passive and predictable.” I completely agree.

Ben goes on to suggest “… before [the FED] beginning to shrink the balance sheet, the FED should have a clearer idea of what its ultimate size should be.” Once again, I completely agree with Dr. Bernanke.

This, too, is a very important issue – and the reason I don’t think the FED will be shrinking their balance sheet any time soon. When the FED balance sheet was about $800 billion back in 2008, we had about that same amount of currency in circulation. Today that number has almost doubled – currency in circulation is over $1.5 trillion. Further, the FED estimates that number will increase to $2.5 trillion within the next 10 years.

Above the $1.5 trillion of currency we discussed above, the FED is also currently holding “excess reserves of Depository Institutions” of almost $2 trillion. What are ‘excess reserves?’

Excess reserves are capital reserves in excess of what is required by regulators. For commercial bank members of the Federal Reserve system, excess reserves exceed the standard reserve requirement amounts set by the FED. Since the ‘Great Recession of 2008’ many commercial banks have opted to deposit these reserves with the FED rather than lend them out.

Why might a bank prefer to deposit excess reserves with the FED … as opposed to making loans to deserving Americans? In a word: Risk. Or, more precisely, the lack thereof.

A bank loan is inherently risky. The borrower may not repay. On the other hand, depositing excess reserves with the FED has zero risk. And yet, it pays a pretty handsome return:

Not bad, right? The bank receives 3/4% on idle funds … funds you or I may have on deposit with the bank earning close to zero. How much is 3/4% per year on $2 trillion? $15 billion. Per year. Let me say this again: US banks are making $15 billion each year on money you and I have sitting in our checking accounts. While we get close to zero. This is why banks have significant excess reserves at the FED. And this is a condition unlikely to change any time soon.

Combining the current demand for currency PLUS the bank incentive to deposit excess reserves suggests the FED set a near-term floor at a minimum of $3.5 trillion … and know they’ll have to increase this figure to $4.5 trillion within the next decade. Ironically, this is precisely where the balance sheet rests today!

Let me summarize. Yes, a rapid sell-off of FED assets could seriously disrupt the capital markets. As would a rapid asset sell-off of by any other developed nation with a similar sized balance sheet. The result of this disruption might be to throw developed economies into recession.

Every central banker knows this. Which is why they won’t do it.

Further, the FEDs assets today must remain at or near $3.5 trillion. US currency needs and excess reserve deposits make this level mandatory. Of course, should the “Emergency Economic Stabilization Act of 2008” be repealed, eliminating interest on excess reserves, then this level could fall. But as long as this law remains intact, it’s likely excess reserves will remain near their current level of $2 trillion.

No, the FED will not significantly reduce the size of their balance sheet any time soon. Don’t worry.

- Terry Liebman

2 Comments

I in addition to my pals were actually going through the good tips from your site then quickly developed a terrible feeling I had not expressed respect to the site owner for those strategies. My ladies became happy to see all of them and have now truly been loving them. Many thanks for getting well considerate as well as for utilizing this form of fine themes millions of individuals are really wanting to know about. Our sincere apologies for not expressing appreciation to you sooner.

Choosing between the two systems could be the difference between shrinking the balance sheet by $1 trillion and $2 trillion, according to JPMorgan s Feroli.