SHI Update 12/28/16: Confidence Reigns!

December 28, 2016SHI Update: 1/4/17 – Happy New Year!

January 4, 2017

Make no mistake: The road ahead looks promising. All indications are strong.

From my economic, financial and ‘real-property’ viewpoints, 2017 is likely to show continued improvements over 2016. I’m optimistic. And I’ll share some of my reasons below.

But there are a few clouds, far out on the horizon, that give me pause. Just a bit. Below, I’ll talk about those as well.

Why You Should Care: It’s quite likely 2017 will prove to be just another relatively ho-hum year with little excitement – from a financial and economic perspective. But there are a few scary bear-traps in the shadows. Below I’ll talk about those that are little concerning today.

Taking Action: Stay informed…read on and see if you share my concerns.

The BLOG: By all measures, Americans have plenty to be happy about as 2017 begins. No, everything is not great… or perfect. But if history teaches us anything we know it never is and never has been. Nor will it ever be. But, in general, things are pretty good here and abroad!

There is no greater proof of this fact than the epic economic and philosophic tome written by economist and historian Dr. Dierdre McCloskey entitled “Bourgeois Equality: How Ideas, Not Capital or Institutions, Enriched the World.” This 768 page book is a stunning intellectual, economic and historic achievement. Agree or disagree with the author’s conclusions, one cannot help being staggered by her intellect.

The essence of the book is this: In the history of humanity, something unique happened around 1800. For the first time – ever – across the globe, human suffering and poverty began to recede. To a massive extent.

In her book, Dr. McCloskey assures us the “Great Enrichment” of mankind since 1800 is the result of ideas. “Our riches,” she argues, “were made not by piling brick on brick, bank balance on bank balance, but by piling idea on idea.”

Ideas, not governments or institutions, were the catalyst. Not just the “good” and practical ideas – for microchips, electric motors and In-and-Out Burgers – but even the trend-setting and society changing ideas of equal liberty and dignity for ordinary folks. Throughout the developed world, new ideas formed the foundation for betterment and its practitioners, upending ancient hierarchies and toppling conventional wisdom. According to Dr. McCloskey, commoners were encouraged to have a go, a “middle class” formed in its wake, and this “new bourgeoisie” took up the “Bourgeois Deal,” and people across the globe were all enriched.

Again, agree or disagree with the author, her arguments are entertaining and compelling.

And the facts are too: Economic historians have discovered that since 1800, adjusting for inflation, there has been a massive improvement in living standards for the average person – by a factor of 10. In the “best run” countries, the factor for improvement in the standard of living is far greater: more that 30X.

I’ll leave this topic for now…but I agree: In the macro, the human condition, across the globe, have never been better. Of course, that doesn’t mean everyone, everywhere, is better off today. Nor does the dispersion of improvement spread equally.

No, plenty of challenges remain. The waves of populism and protectionism spread across the globe, and the anger against the political and wealthy ‘elite’, make us very aware of some of the more immediate obstacles. As Trump moves into his new house on January 20th, he will have no shortage of opportunity to implement meaningful change.

Americans and foreigners alike harbor great expectations … in 2017 and the years following, his administration will be tested as the clouds ebb and flow:

-

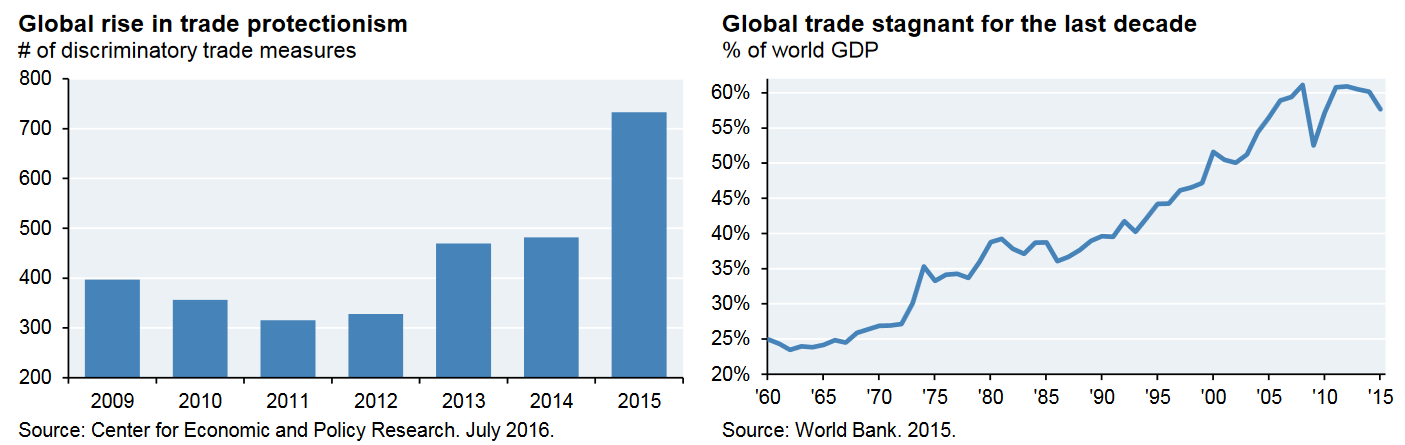

Global Trade: Protectionism is on the rise. After decades of growth in across-border trade, since the “Great Recession” the tide has turned. Global trade, as a % of world GDP, is on the decline:

And this is before Trump enters the White House and potentially shepherds in new US anti-trade policies, a possible “trade war,” and other protectionist measures. Is “free trade” a panacea or the problem? Probably a little of both. But once rung, it’s impossible to un-ring a bell. Hopefully, the Trump administration will recognize this truth. We’ll see.

-

Banking and Foreign Exchange: The value of the US Dollar is on the rise. Ignoring the reasons for the moment, rest assured there are both positive and negative implications. Positive: Everything and every place outside our borders is cheaper! Europe is on sale! Today, one USD buys .95 Euros. Two years ago, one USD bought .82 Euros. And in 2008, .68 Euros. The same trend is true in England and all across the developing world.

Here’s the negative: A rising dollar means our exports are more expensive for other countries to import. Have no doubt: this will impact the US GDP. Adversely. Further, the dollar rise puts pressure on China (which we’ll talk more about later). The yuan, China’s currency, fell 7% against the USD in 2016. Wealthy Chinese – of which there are now many – are very unhappy with this trend. Capital outflows are the result…as a lot of wealth leaves China. In theory, each Chinese citizen can move the equivalent of $50,000 out of China each year. In reality, the amounts are much larger. The ‘official’ Chinese balance of payments deficit reached $469 billion by the end of Q3, 2016. Unofficially, a French investment bank Natixis SA estimated 2016 outflows will exceed $900 billion before the year ends.

But the capital outflows aren’t the biggest problem. When capital leaves China, it leaves their banking system and enters (presumably) a US bank. While no one knows for certain (China is notorious for publishing misleading economic and financial metrics) Chinese banks already have serious liquidity problems. Per The Economist magazine, many Chinese banks have mis-categorised risky loans as investments to dodge scrutiny and reduce capital requirements. These shadow loans were worth roughly 16% of standard loans in mid-2015, up from just 4% in 2012. No doubt, this practice increased in 2016.

Further, for years China restricted bank loans to less than 75% of their deposit base, ensuring that they had plenty of cash in reserve. Today, again per The Economist magazine, the real level is nearing 100%, a threshold where capital outflows exacerbate this problem to crisis levels. Combine massive bad debt (https://www.bloomberg.com/news/articles/2016-12-01/small-china-banks-with-4-trillion-assets-seen-too-big-to-fail) with growing capital outflows AND a trade war with the US and <BANG!> we could see China’s economy light up the sky like one of their beautiful sky rockets. Not in a good way.

In their October, 2016 “Global Financial Stability Report” the IMF raised serious concerns about growing concerns over China’s banking system and the proliferation of “shadow credit assets” credit products held by Trust and Securities companies and Asset Managers. Per the IMF, these products grew by 50% in 2016, resulting in an outstanding balance of about 40 trillion Renminbi – or about 5.75 trillion USD. About 1/2 of these assets are high-yield, adding further stress to a stressful concoction.

Summarizing, not only is the China credit system expanding at a pace far faster than the economy can support, new “shadow” credit instruments are high-yield, and finally, a large (but undisclosed) portion of these liabilities are in default status. Truly an incendiary mix.

-

The FED: Trumponomics must concern the FED. The combined effect of proposed tax cuts and increased infrastructure spending, if they become reality, is inherently inflationary. Even if the Trump administration achieves the 4%+ annual GDP growth they’re forecasting (the result of our tax cuts/infrastructure plan, repatriation of foreign US capital, deregulation, large military expansion, and retooling the Affordable Care Act), thereby keeping the US debt levels stable and annual deficits small, this result, too, is inherently inflationary. Of course, these changes won’t happen overnight, or even in one year, but the sum total must have the FED concerned about the longer-term inflation picture. Translation: Potentially more FED short-term rate increases than I’m currently anticipating.

-

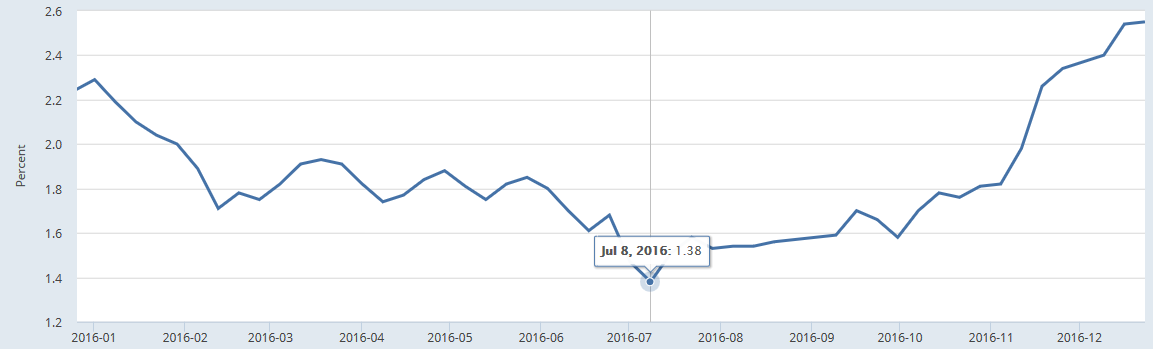

US and Global Interest Rates: US long-term rates spiked after the presidential election. Significantly. After bottoming in early July at 1.38%, the 10-year Treasury ended the year very near 2.5%. It’s easy to see the spike after November.

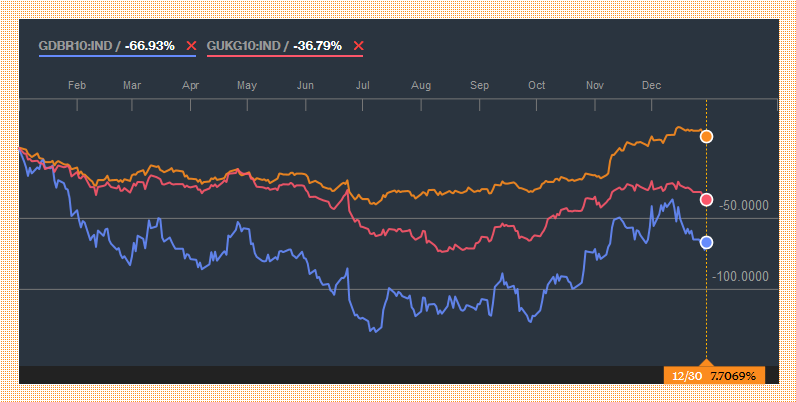

But while our rates are up, interest rates in other advanced economies are not. Here’s an ‘index’ chart, courtesy of Bloomberg, showing while the US 10Y-T is up 7.70% from January 1, 2016, the Great Britain 10Y is down almost 67% and the German 10Y Bund is down almost 37%.

You didn’t think “negative interest rates” were gone did you? Nope. Sure, the media may have given you that impression…but rest assured, government securities in much of the developed world remain firmly entrenched in the negative:

No, the US didn’t make the chart. Here’s the point: About 40% of Eurozone and Japanese debt is trading with rates below 0%. Combined, their GDP is about 125% of the US GDP. While there is not direct correlation between their government interest rates and rates in the US, each impact the other, whether by contagion or financial physics.

In the “Global Financial Stability Report” the IMF suggested long-term rates are low today for 4 reasons:

-

Central Bank bond purchases;

-

Increased demand for ‘long-duration’ assets by pension funds and insurance companies;

-

Political uncertainty increases longer term bond demand; and,

-

Secular stagnation (the concept that we’re now in a low GDP, low productivity world.)

Clearly, these conditions are global. The US is not exempt. The IMF report had some great illustrations supporting these claims:

Summarizing, again, these 4 conditions are global are unlikely to change in the near future. Which suggests that over time, longer-term US yields must realign with those in other advanced nations. But does that mean their rates will rise … or ours will fall? Hmmm……

-

Saudi Arabia: Oil. OPEC. Driving global forces. But in 2014, 2015 and 2016, SA ran a massive budget deficit: Close to $100 billion per year, about 15% of its annual GDP. In 2016, SA took on debt…selling government bonds for the first time. In 2017, it’s expected they will take Aramco public, possibly creating the most valuable publicly held company on the planet. All the while, working to retooling the SA economy into a “market” economy, unreliant on oil revenue, by 2030. Make no mistake, this is a very dark cloud indeed…perhaps not for 2017 but in years beyond.

-

European Dominoes: Whether it’s a teetering Monte Paschi (bank) in Italy, another Greek tragedy, a Brexit bomb, or some other equally Shakespearean complication, 2017 may bring us another mess that threatens the stability of the ECB or the Euro…and spreads contagion around the global financial system. Not good.

-

Regulation: In 2016 the California legislature passed 1,059 new bills … and Governor Brown signed 898 into law. 898 new laws on top of the already massive pile of rules and regulations. Staggering. On the other hand, at the federal level, Trump has assured us that for every one new federal regulation, two existing regs must be eliminated. According the the Competitive Enterprise Institute, the US Federal Register (US laws) was up to 79,380 pages in 2016. This tree can use a bit of pruning. Bravo!

Scary right? Welcome to 2017! Like every year before, storm clouds shroud the horizon.

Maybe we should worry simply because this year ends in a ‘7’. After all, the largest one-day stock market decline took place in 1987; the Asian (ASEAN) crisis reared its ugly head in 1997, threatening global economic stability; our “Great Recession” kicked off in 2007 … and now 2017 is here. Is this alone cause for concern? 🙂

Only if you are superstitious. 🙂

Remember, while many other advanced nations remain mired to various depths in their own financial and economic morass, the US recovery continues. GDP, if low, is at least consistent. Corporate profits will begin to grow faster this year. Labor conditions remain strong and the employment picture continues to improve. Our financial markets are cresting new highs; the balance sheet of US households has never been higher – collective US household net worth is now over $90 trillion. Banks are healthy. Interest rates, by historic standards, remain near 5,000 year lows. In the macro, home prices have recovered…and are likely to continue to increase in value.

Try not to worry! As I right this BLOG, I’m optimistic the clouds will remain on the horizon. Things are actually pretty good! And if I feel that’s changing, I’ll let you know.

Now that 2017 is here, in my next BLOG post (after the SHI Update), I will make my 2017 predictions. Be sure to check back – this will be fun!

1 Comment

Great info and right to the point. I am not sure if this is really the best place to ask but do you guys have any ideea where to get some professional writers? Thx 🙂