SHI 3.22.23 — How Safe is YOUR Bank?

SHI 3.15.23 — Bank Panic!

March 15, 2023

SHI 3.29.23 — Reputation Lost

March 29, 2023

Or, perhaps, more precisely, how safe is your money?

The short answer? Not overly safe.

Because banks are designed to fail. Not intentionally, of course. But the current design is seriously flawed. On the other hand, if you have less than $250,000 in your account, your money is quite safe. FDIC-insured safe. Guaranteed-by-the-US-Government safe.

However, if you’ve been fortunate enough to save more than $250,000, or if you are a business owner with more than that in a bank business account, bank safety is a really important issue to you. And it should be.

“

Your bank is not “safe.”

“

Your bank is not “safe.”

But this is nothing new. Banks have always been unsafe for large or business depositors. On the other hand, they are probably safer than storing money in your mattress. 🙂

The problem is design. You bank promises to return your money the instant you want it. But as soon as you left your bank, they immediately lent out your money for years. That’s how banks make money. So how can they possibly keep their promise to return your money … if they don’t have it sitting in their vault?

Risk is part of life. Every day we take risks – some we choose, others are circumstantial. When you make an ‘investment’ expecting a return, you’ve decided to accept some level of risk. When you step off the curb and walk across the street, you risk “getting hit by the bus” so to speak. But when you deposited $300,000 into your businesses checking account to cover a bi-monthly payroll, did you ever consider those funds might simply vanish before your employees cash their checks? No. You did not.

Well, until now that is. Now everyone is thinking about it.

Which brings us back full circle: How safe is YOUR bank? Let’s take a look. And does “fear” impact expensive steakhouse reservations? After all, rich folks with fat wallets love our opulent eateries … are they too worried to eat thick, juicy steaks? Has the banking crisis curtailed reservation demand? I wonder ….

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. At the end of Q3, 2022, in ‘current-dollar’ terms, US annual economic output rose to $25.74 trillion. Thru Q3, America’s current-dollar GDP has increased at an annualized rate exceeding 7%. The world’s annual GDP rose to over $100 trillion during 2022. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the 3 big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

“You can’t unring a bell.” Every attorney knows this expression. It’s difficult, if not impossible, to forget information once it is heard.

We now know banks are, in general, unsafe. The bell has rung. How unsafe are they? Is some of your money at risk?

We all get some benefits from our bank checking or savings accounts. They help us buy stuff, pay bills, and other similar things. And lately, they might even pay a little bit of interest. And yes, the FDIC has agreed to protect from loss up to $250,000 “per beneficiary.” So, in theory, with a little creativity, a depositor can probably protect much more than this amount.

But a mid-sized business cannot. And that’s a serious problem. And even worse, the risk is completely asymmetrical. In other words, while the bank helps the business with buying stuff, paying bills, paying payroll, etc., the value of those services is not high. Meaning that while the “benefits” of using any particular bank are easy to identify, how much risk-of-loss should that business accept? Almost none would be my answer.

Ironically, until recently, the risk seemed exceptionally small to all of us. And then “along came a spider who sat down beside ‘er … ” or more specifically, the SVB bank failure, and all of a sudden that risk is in the spotlight. Looming large like a big spider.

Much has been made about the size of the “uninsured” deposits at Silicon Valley Bank. I get it. A depositor with uninsured deposits is likely to quickly bolt out the door with his money the moment believes the bank is in trouble. Even though that choice, in itself, increases the bank’s problems. The higher the uninsured percentage, the more deposits that may run out that door. Troubling.

Do you know what percentage of your bank’s deposits are uninsured?

Probably not. But uninsured deposits tell only a small part the story. Another is the extent of your bank’s “unrealized losses,” which I discussed back in January and in last week’s blog. You’ll recall I shared the current state of “unrealized losses” our banks are carrying in their investment portfolios. Did you miss either of those two blogs? Here are the links if you’d like to read them:

https://steakhouseindex.com/shi-1-5-23-jobs-jobs-jobs-and-money/

https://steakhouseindex.com/shi-3-15-23-bank-panic/

Yes, unrealized losses in your bank’s portfolio are also a critical data point to understanding how safe your bank is today. But unfortunately, the issues don’t stop there. We also need to know what percentage of your bank’s deposits are held in fixed-rate “loans” made to customers over the years plus the percentage of HTM investment securities. What are “HTM” securities? As discussed last week, these are “held to maturity” investments – investments which by FDIC regulation do not require the bank to “mark them down” when rates go up. As I said last week:

We all know that our bank is not sitting on the cash we deposited. Even though we are promised we can withdraw our cash at any time, we know they invested the money for a much longer duration. In “safe” things like home mortgages, US Treasuries, etc. But those investments fluctuate in value as interest rates change. And if rates go up really, really fast, assets purchased before the rate hikes are worth less, on a current-value basis, than before the hikes.

Which is why the FDIC permits member banks some latitude about how they manage this issue. A few decades ago, federal accounting standards were revised. Under this new standard, banks were required to report the “fair market value” of their assets in all public disclosures. But with a nuance. Banks have three (3) different possible labels for securities they hold on their books. And the bank can pick the label they want to use. The “Hold To Maturity” — let’s abbreviate as ‘HTM’ — label means market value losses do not impact earnings or capital. Meaning, any “mark to market” losses can effectively be hidden from public scrutiny. If classified as “Trading” assets, those identical holdings would have been required to include the unrealized losses in their earnings and equity. A third category, “available for sale,” lets lenders exclude such losses from their earnings, but not equity.

OK, let me make this a bit simpler. To decide how safe your bank is, we need to know at least two things: First, what percentage of the deposits are uninsured, thereby skittish and subject to a fast run out the door? And secondly, what percentage of the deposits are illiquid because they have been used for loans and HTM securities?

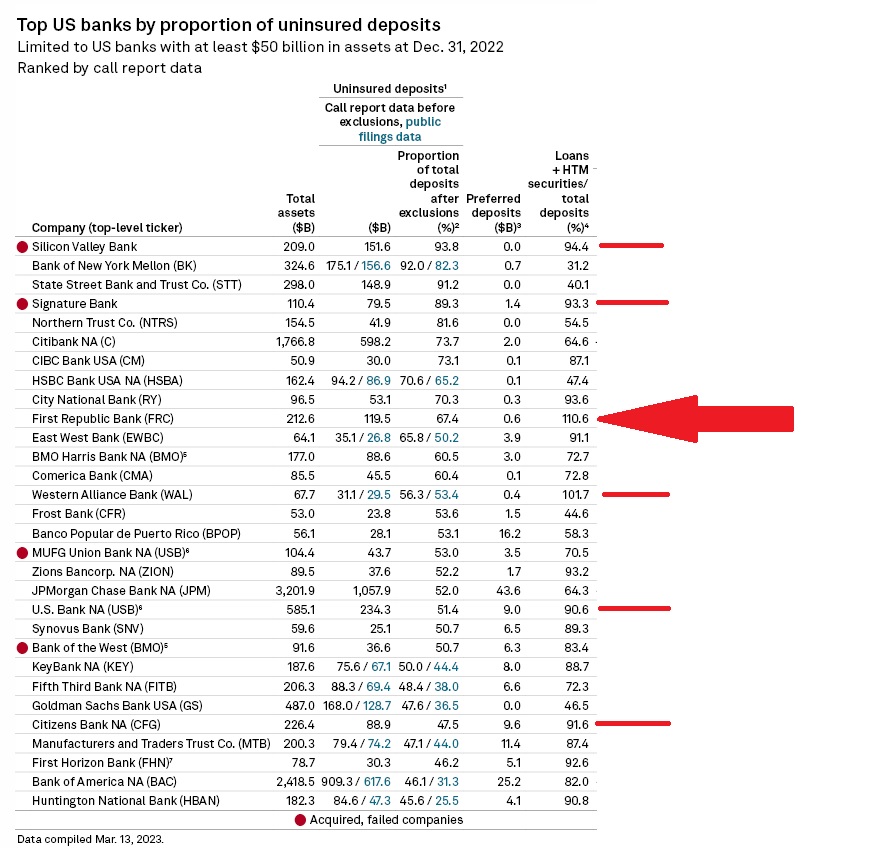

Fortunately, S&P Global has an answer for us. “Market Intelligence” is a newsletter put out by the rating agency, Standard & Poor’s. The ‘S&P500‘ is their creation from 100 years ago. Anyway, the image below is right on point, from their March 14th newsletter. It is right on point, showing meaningful data about “uninsured” and “illiquid” deposits. Take a look:

(here’s the link, if you want to read the report: https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/svb-signature-racked-up-some-high-rates-of-uninsured-deposits-74747639)

Is your bank on the list above? I suspect it is … as this list includes all banks with at least $50 billion in assets. The list is sorted by the “uninsured” deposit column. The bank with the greatest uninsured deposit percentage is at the top … the smallest at the bottom. The “illiquid” question is addressed in the column to the right.

I added the ‘red lines’ and the red arrow on the right side of the image.

As we all know, the bank at the top of the list has already failed. SVB was a $200 billion bank. As we see above, almost all its deposits were uninsured. Which means any fright at all and their depositors will attempt to grab their cash and head for the door. Additionally, and equally unfortunate, their ‘loans + HTM’ combined to almost 100% of total deposits.

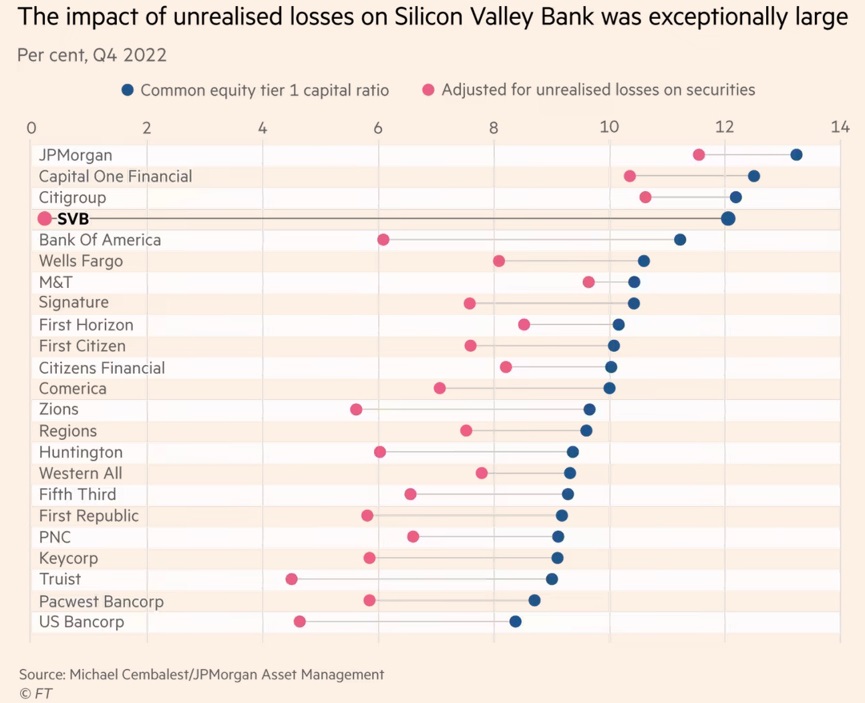

As we know now, this combination proved fatal for the bank … and I’m sure another metric known as “common equity tier 1 capital ratio,” after that metric is adjusted for the “unrealized losses,” also exacerbated the problem:

The unrealized losses discussed above are not “true” losses — in that they have not actually happened yet. But they would happen in a fire sale — if the institution was forced, for some reason, to sell these securities. Look at the SVB common equity after adjustment for unrealized losses. Just about zero.

Thru this lens the bank’s failure makes perfect sense. The same can be said for the failed Signature Bank.

Now let’s look at the other beleaguered bank, First Republic. Their uninsured percentage is quite a bit lower. About 2/3 of their deposits are in that bucket. Their larger problem is their illiquid capital. And their tier 1 capital after adjustment for unrealized losses. Take a look: Their ‘loans + HTM’ are over 110% of their total deposits! Meaning their loans and investment securities exceeds their total deposits! Is this even possible? Apparently it is.

Remember, this is the foundational challenge a bank faces: After promising a depositor complete liquidity, and then lending or investing that deposit into completely illiquid assets, how can the bank possibly return funds to depositors on demand? Especially if herd mentality takes over and a bank run ensues? They can’t. Unless they get some help … and they did ….

Did you know the FED solved this problem 10 days ago? Not for the ‘loans’ portion of the portfolio, but the ‘HTM investment’ in government securities is now backstopped by the FED to 100% of the security’s face value. On March 12, the FED established the ‘The Bank Term Funding’ program…. From the FED‘s press release:

“The BTFP offers loans of up to one year in length to banks, savings associations, credit unions, and other eligible depository institutions pledging any collateral eligible for purchase by the Federal Reserve Banks in open market operations, such as U.S. Treasuries, U.S. agency securities, and U.S. agency mortgage-backed securities. These assets will be valued at par. The BTFP will be an additional source of liquidity against high-quality securities, eliminating an institution’s need to quickly sell those securities in times of stress.”

The take-away is clear: Any and all government-guaranteed security qualifies as collateral … the FED will lend 100% of the ‘face value’ of those securities thereby eliminating any unrealized loss potential for the bank … and this action eliminates the bank’s need to potentially sell any of these securities to meet depositor demand. This is a huge help. Frankly, if this lending facility was in place before the SVB failure, it probably would have prevented the SVB failure!

There is a TON of cash sloshing around in bank accounts across the developed world:

Companies in developed nations are holding over $14 trillion in cash. Do you think they want to hassle splitting up their hoards into $250,000 increments across thousands of banks? Of course not. Banks need to be safe for individuals and companies. So how can we make banks safe?

Earlier today SoFi Bank took a stab at an interim solution. SOFI is now offering FDIC insured checking accounts up to $2 million. How? Simple. ‘SoFi Checking and Savings’ is making this added coverage available through the ‘SoFi FDIC Insurance Network,’ a recently created partnership with 12 different banks. Presumably, SoFi, themselves, will split up your $2 million hoard so you don’t have to. Interesting. This solution may have legs … let’s keep watching and see how it evolves.

Let me propose an alternative: The FDIC should sell insurance to the depositor.

Right now the FDIC covers up to $250,000 at no cost to the depositor. Banks pay a small fee to the FDIC for this insurance. If you’re more curious about the actual cost, here’s the “FDIC Assessment Rates” website … but I’ll warn you: It’s pretty opaque and I couldn’t make heads or tails out of it … and it has something to do with camels. 🙂

https://www.fdic.gov/deposit/insurance/assessments/proposed.html

Say you owned a business and you wanted to insure your deposits exceeding $250,000. Would you pay for that insurance? Sure. If the cost was reasonable. And it should be quite low if most depositors chose to be fully insured and pay the fee. In this way, the “uninsured” would be subject to loss from a bank run … but insured depositors would have no risk. Think about it: Wouldn’t this eliminate both the fear and risk of a bank run?

Or maybe the FDIC should go one step further: Make FDIC insurance mandatory for all deposits. And simply charge the depositor some small premium, based on deposit size, to insure their accounts and money. This would eliminate all bank runs. Because all funds would be fully safe and insured, there would be no reason to move them from your bank, regardless of the bank’s size, “unrealized” losses, or illiquidity. And with the FDIC and FED bank oversight in place to ensure all banks still follow prudent, established guidelines, theoretically absent widespread fraud, bank runs would become a thing of the past and Hollywood legends. I like it!

Let’s head to the steakhouses.

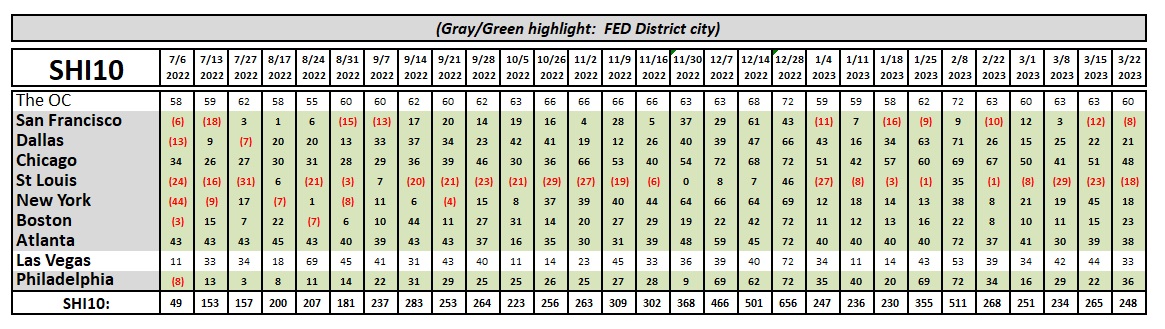

No, it turns out this weeks SHI10 is almost identical to last weeks. Turbulence in the banks has not caused tummy-troubles for the well-heeled, expensive eatery clientele. This week, plenty of rich folks remain happy to part with $1,000 for dinner for four. Interesting.

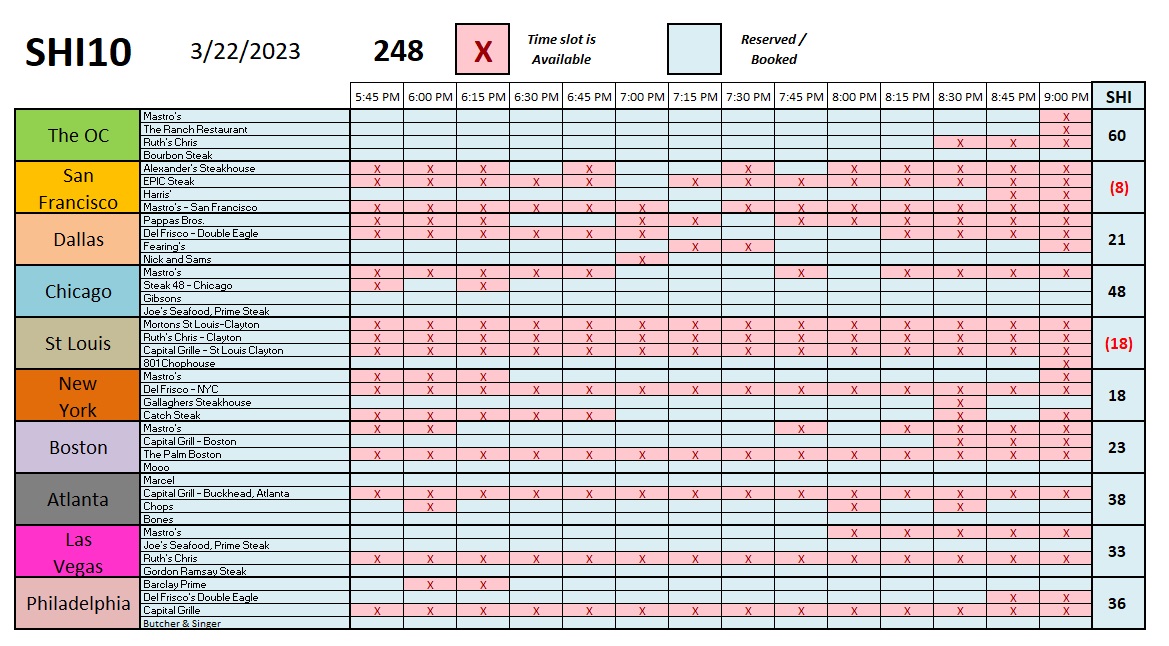

Here are the weekly results by restaurant:

Oh, earlier today, if you missed it, the FED raised rates by another 25 basis points. Fed funds are now about 5%. An interesting choice in light of the bank run backdrop. They remain convinced inflation is a more serious threat. Interesting.

<:..:—:…:> Terry Liebman

{kind=link}

{kind=link}