A Hill of Beans

SHI Update 10/26/16

October 26, 2016The SHI Update 11/2/16

November 2, 2016The Wall Street Journal article heading read, “Good Quarter Signals Better Growth Next Year“. Sorry, but no, that’s not what the GDP reading tells us.

Why you Should Care: This quarter’s GDP growth rate was strong. That is an inherently good thing. But, as with most things, “the devil is in the details” and that’s where we’re going right now. Into the weeds. Because the WSJ claim aside, better growth is not assured by this quarter’s strength.

Taking Action: Remain defensive in your choices and investments. Unfortunately, our economy doesn’t have the horsepower to grow consistently at this high rate.

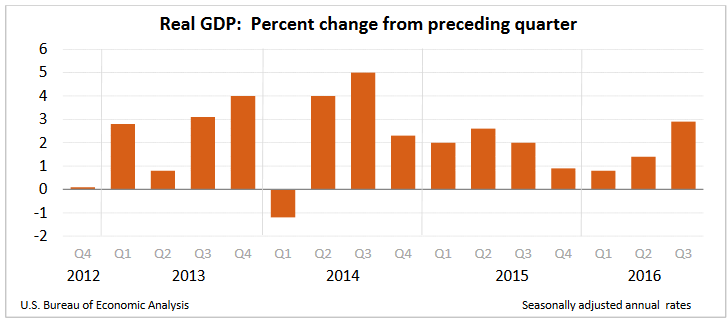

The BLOG: As we expected, Q3:2016 GDP growth rate was above trend. The ‘preliminary’ reading showed a 2.9% annual real growth rate … and even better, ‘current-dollar’ GDP increased by 4.4%, or $201.1 billion. The current-dollar (nominal) US GDP is now $18,651 billion.

On Friday morning, October 28th, the BEA reported: “The acceleration in real GDP growth in the third quarter reflected an upturn in private inventory investment, an acceleration in exports, a smaller decrease in state and local government spending, and an upturn in federal government spending. These were partly offset by a smaller increase in PCE, and a larger increase in imports.”

OK … you will recall we anticipated the “upturn in federal spending“, the inventory increase is typical in Q3, and the SHI has been predicting a slow down in consumer spending, or a “smaller increase in PCE” as the BEA reported.

But the “acceleration in exports” surprised me. In spite of the strong USD, are exports ramping up? Is foreign demand for US goods and services increasing for some reason? This would be great, if it’s true, so let’s take a look.

Our raw international trade data comes from the US Census Bureau. Here’s a link to their latest report: https://www.census.gov/foreign-trade/Press-Release/current_press_release/ft900.pdf. The final trade report encompassing all of Q3 will be released on November 4th … and this new data will then be included in the ‘second‘ Q2 GDP estimate, to be released on 11/29.

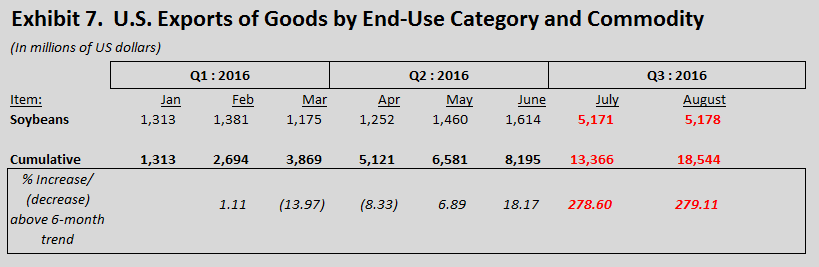

Open this trade report and go to page 7. There you’ll find ‘Exhibit 7,’ an itemization of US exports. As I expected and predicted, the 2016 YTD exports – in total – have declined by about 5.5%. This is correlated with – and likely caused by – the increased value of the dollar during Q3.

And if you look down the right hand column on page 7 you’ll see a lot of negative numbers – indicating declining export quantity.

Until you get to soybeans. Soybean exports are WAY UP. By a staggering amount:

In July and August, alone, the US exported $10.35 billion of soybeans – about 80% of our entire 2015 soybean exports! In just 2 months! Now THAT is a hill of beans!

According to the USDA, the US and Brazil – combined – produce about 2/3 of the world’s soybeans. Brazil is the worlds largest soybean exporter. Every year they produce and export about 100 million metric tons of beans – the US, slightly more. And according to the USDA, both the US and Brazil will produce about the same quantity this year. Global production appears relatively consistent.

Which means I have no idea why US soybean exports were so popular in July and August. I suspect this spike is a momentary aberration. And this bean spike helped US exports increase 10% during Q3, contributing 1.17% of the 2.9% GDP. Without this hill of beans, Q3 GDP growth would likely have been closer to 2.0%.

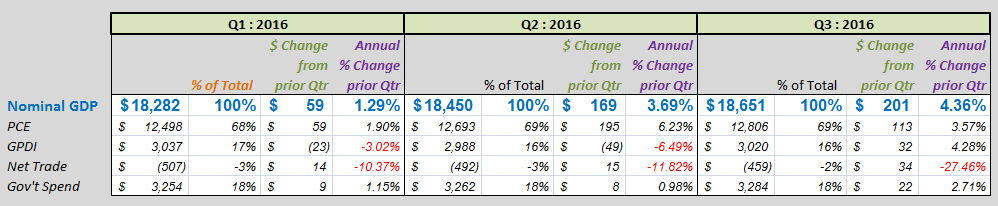

But even more concerning to me is the deceleration in consumer spending. Take a look at this chart:

Of the 2.9% GDP growth, PCE (or consumer consumption) was 1.47% – about 1/2 the final figure. You may recall last quarter, PCE actually exceeded the final GDP number. In fact, without robust consumer spending in Q2, the 1.4% final reading would have been much, much lower.

In raw numbers (see the chart above), this quarter PCE was $113 billion; last quarter, $195 billion. A very large decline.

Rest assured, the Q3 number is good. This was a strong quarter. In general, we should all be pleased. But the ‘one-off’ nature of exports – nicely juicing the number – is unlikely to repeat. Which means our economy must remain reliant on the long-term, consistent trends which make up the foundation of US GDP growth.

And those trends do not point toward a 2017 acceleration. No, we’re likely to see more of the same: Absent structural improvements, GDP growth in the 1.5 – 2.0% range for some time into the future. This good quarter notwithstanding.

- Terry Liebman