A Race to the Bottom

The Steak House Index (SHI) Update – 9/28/16

September 28, 2016The Steak House Index (SHI) Update – 10/5/16

October 5, 2016On March 10, 2005 Ben Bernanke gave a speech to the Virginia Association of Economists. He made a novel statement: “Over the past decade,” he said, “a combination of diverse forces has created a significant increase in the global supply of saving — a global saving glut — which helps to explain … the relatively low level of long-term real interest rates in the world today.”

It’s worth noting that as Bernanke spoke back in 2005, the FED funds rate was 2.75%, the 10-year Treasury (CMT) was around 4.5%, and a 30-year mortgage would cost you about 5.9%. By today’s standards, these are exceptionally high rates.

Why You Should Care: Interest rates will remain low…for many years to come.

Taking Action: Unless you feel the FED – and other central banks around the world – will soon begin to unload their investment, plan for interest rates to stay very low for a very long time. Make your savings and investment choices accordingly.

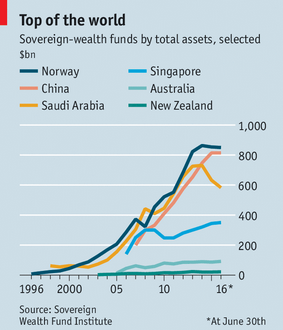

The Blog: Take a look at this graphic from the most recent Economist magazine:

Back in 2005 when Ben began to popularize the idea that a global savings glut was sloshing around within the developed world economies, buying up every debt and equity asset they could get their hands on, Norway was well on its way to become the worlds largest sovereign wealth fund. But it was a baby compared to its size today.

What is a sovereign wealth fund? Well, it’s usually an investment fund owned by a country. Some are formed when the country has a ‘surplus’ in balance of trade and accumulates large reserves. Norway has been a huge benefactor of historically high oil prices…and has amassed an investment fund valued at $882 billion as of last week. Per the Economist, this funds owns more than 2% of all listed stocks in Europe and over 1% globally. Impressive, right?

In 2005, China didn’t have a sovereign wealth fund (“SWF”). It does today. From it’s humble beginnings in 2007, China’s SWF today has assets exceeding $813 billion. So Ben wasn’t even talking about China’s wealth at that time – it didn’t yet exist.

Here are a few more that began in or after 2005:

- Qatar: $335 billion

- UAE: $306 billion (a total of 2 funds)

- Saudi Arabia: $160 billion (not their main fund, a “Public Investment Fund”)

- Russia: $138 billion (2 funds)

- Australia: $95 billion

- South Korea: $92 billion

- Kazakhstan: $77 billion

… and the list continues. Shall we add them up? Including China, in June of 2016 this group owned assets exceeding $2 trillion! Remember: In 2005 – when Ben first spoke on this topic – they were worth zero. Norway had about $600 billion less.

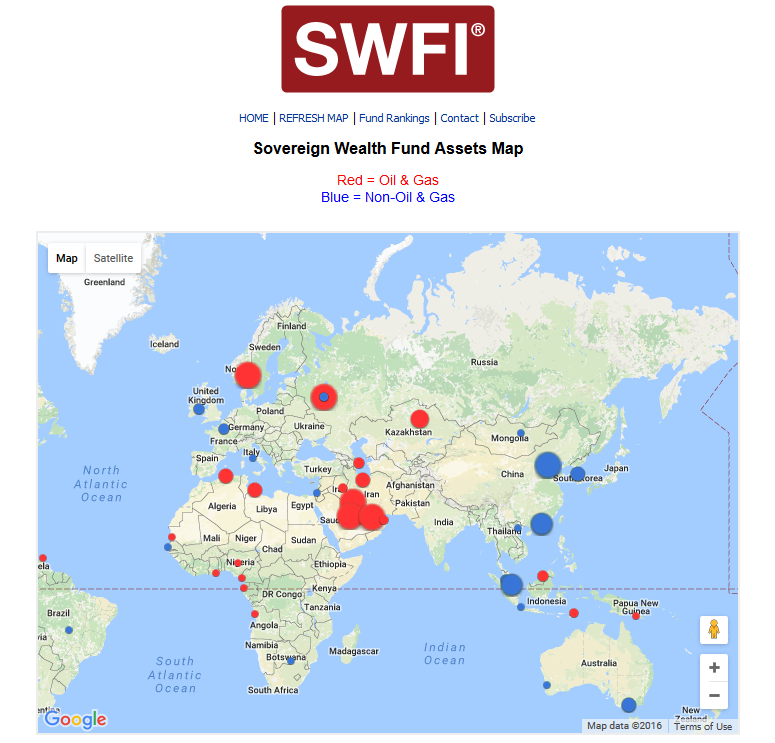

The Sovereign Wealth Fund Institute tracks this segment. Here’s an interesting graphic showing the global dispersion of SWF:

Ben Bernanke was spot on. The savings glut is real. A recent study from the International Center for Monetary and Banking Studies ‘Geneva Report’, entitled “Low for Long? Causes and Consequences of Persistently Low Interest Rates”, attributes the glut – and the low resultant interest rates – to:

- An increased propensity to save “driven in particular by demographic developments…” as I’ve discussed in many prior blogs; and,

- “The integration of China into global financial markets” as China became the #2 GDP in the world.

Number 1, as we’ve previously discussed, seems to be further exacerbated by low rates of return, creating a negative feedback loop. As populations age, saving more, and experiencing falling ROIs, they feel the need to save more to achieve their original objective. Thereby moving even more money from consumption into savings.

As to #2, Randall Krozner is quoted in the Economist as saying, “A billion people with a 40% savings rate; that brings a lot more supply (of savings) to the table.” Yeah, I’ll say.

In his September 30th blog, Larry Summers comments yet again, “…(the FED) should acknowledge that the neutral rate is now close to zero and it may well remain under 2% for the foreseeable future.”

Ben Bernanke and Larry Summers are two pretty bright guys. No, not because they agree with me (he, he, he, he….). Their depth of experience, across time and geography, suggests they are worth listening to. Apparently the FED agrees: Dr. Summers recently spoke at a Dallas FED forum: http://larrysummers.com/2016/09/30/four-modifications-to-feds-current-posture/

Let me finish with these comments: In their concluding remarks, the ‘Low for Long?’ report suggests that not only is the present low interest rate environment “historically most unusual” but if these conditions persist, they pose “special challenges for individuals and policy makers alike.”

And they suggest a return to a world with a higher neutral real interest rate is desirable. For many reasons.

Desirable or not, however, I don’t believe the conditions underlying this state will change any time soon. Simple math suggests the demographic condition underpinning the saving glut is likely to become even stronger in years to come – the result of more savers and the need for those savers to make up for reduced ROIs – in years to come. Throw in China’s new and growing wealth, SWFs, etc, and you have a pretty big, sloshing pool of money out there looking for yield.

Of course, the central banks can impact this condition. If they choose to. Remember, they hold about $18 trillion in assets today, up about $11 trillion since 2008. (Here’s my blog on this topic: https://terryliebman.wordpress.com/2016/09/18/the-rise-of-the-central-bank/).

Should they decide to unwind some of their trades, this action might re-supply the markets, thereby pushing down prices – and pushing up yields. But this action has other consequences – mainly, creating an economic ‘tightening’ which would have a deleterious effect on GDP growth, possibly pushing an already weak economy into recession.

No, I think this is a decade (or more) long condition. Buckle in.

- Terry Liebman

{kind=link}

4 Comments

Not great news Terry, but well reported.

Thanks Joe.

[…] But Trump’s election, in itself, does not change the global imbalance between the supply of, and demand for, capital. https://terryliebman.wordpress.com/2016/10/02/a-race-to-the-bottom/ […]

excellent points altogether, you just gained a new reader. What would you recommend about your post that you made a few days ago? Any positive?