SHI 01.23.19 – Can This Be Fixed?

SHI 1.16.19 – Sputtering Engines

January 16, 2019

SHI Update 1.30.19 – Weighing the Data

January 30, 2019

” … posed IMF Chair Christine Lagarde in a Davos interview on Tuesday. This existential fear, she contends, overshadows all markets and economic conditions right now.”

And by “this,” she speaks of the U.S government shutdown. Clearly everyone is worried about fallout as an end to the shutdown appears nowhere in sight. She’s not the only one worried. When asked, business leaders, consumers and universities express similar — if not greater — concern. Worry is wafting in the air, like the smell of a sizzling T-Bone, all around us, ubiquitous. If I owned an expensive steak house I might be worried too. Let’s look at all the talk and worry … and see if 700 degree filets are still flying off the grill.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will continue to be true for years to come.

Is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is about $80 trillion today. US ‘current dollar’ GDP now exceeds $20.66 trillion. In Q3 of 2018, nominal GDP grew by 4.9%. We remain about 25% of global GDP. Other than China — a distant second at around $12 trillion — the GDP of no other country is close.

The objective of the SHI10 and this blog is simple: To predict US GDP movement ahead of official economic releases — an important objective since BEA (the ‘Bureau of Economic Analysis’) gross domestic product data is outdated the day it’s released. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

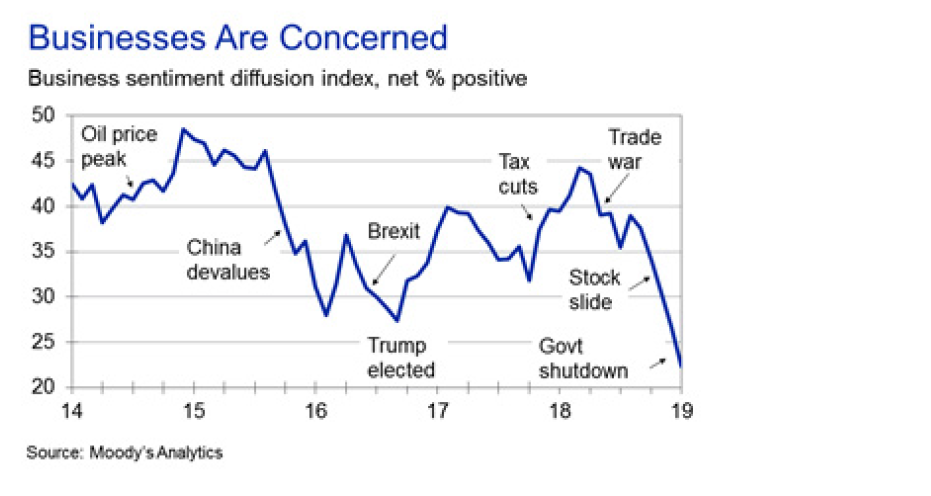

Business leaders are worried. They fear the future may not be as bright as the past few years:

According to Moody’s, business sentiment is dropping like a stone — faster than about 3 years ago during the China scare.

Moody’s assessment:

” … if the shutdown continues for any longer, the broader economy will suffer. If the president and lawmakers haven’t figured things out by the end of March, we estimate the shutdown will reduce first-quarter real GDP growth by approximately 0.5 percentage point. Of that, about half will be due to the lost hours of government workers, and the other half to the hit to the rest of the economy. Even this may be optimistic, since we assume the administration keeps triaging government functions. The dark irony is that if the shutdown lasts this long, the dollars and cents cost to the economy will be more than $25 billion. That sum would go a long way toward paying for the border security…. “

For 91 consecutive calendar quarters — more than 20 years — Duke University has surveyed CFOs across the globe, sharing with us this longest-running and most comprehensive report from senior finance executives. What are the CFOs saying?

-

48.6%K of U.S. CFOs believe the U.S. will be in a recession by the end of 2019.

-

82% believe a recession will have begun by the end of 2020.

Business leaders are not the only folks concerned. Consumers are as well. According to the University of Michigan ‘Consumer Sentiment‘ poll released on January 18th,

“Consumer sentiment declined in early January to its lowest level since Trump was elected. The decline was primarily focused on prospects for the domestic economy, with the year-ahead outlook for the national economy judged the worst since mid 2014. The loss was due to a host of issues including the partial government shutdown, the impact of tariffs, instabilities in financial markets, the global slowdown, and the lack of clarity about monetary policies.”

Even more concerning for our steakhouses was this comment from the University survey:

” … consumers now sense a need to buttress their precautionary savings, which is typically done by reducing their discretionary spending.”

Well, that doesn’t bode well for Mastros bottom line. This is not good at all.

And while we chew on that piece of gristle, remember that the Steak House Index is anecdotal. Meaning, the SHI is not intended to measure tangible economic metrics … we measure intangibles — how people are feeling … and whether these feelings impact consumer spending patterns.

Because, in the final analysis, consumers drive the global economy. Here, in Europe and now in China. And how consumers feel, in the aggregate, drives consumption behavior. And the sale of expensive cuts of beef.

As I’ve discussed before, in the macro, our collective behaviors are rational. Meaning, when faced with danger, we pull back. When faced with ‘financial’ danger, we do the same: we adapt our behavior to the conditions in which we find ourselves.

If we – or our company (for those of you on a company ‘expense account’) – are feeling financially pinched, it is unlikely we will take a party of 4 people to an expensive steak house for dinner on Saturday night. Conversely, if we’re feeling flush — sure — we’ll go to Ruth’s Chris Steak House on Saturday night and spend $300 or $400 for dinner.

And right now, business and consumers alike are clearly worried. Not by any one thing, mind you, but in the aggregate the sheer weight is bearing down. Like a sack of stones on our backs, fear is weighting down businesses and consumers alike. Let’s see if the steakhouses are feeling it.

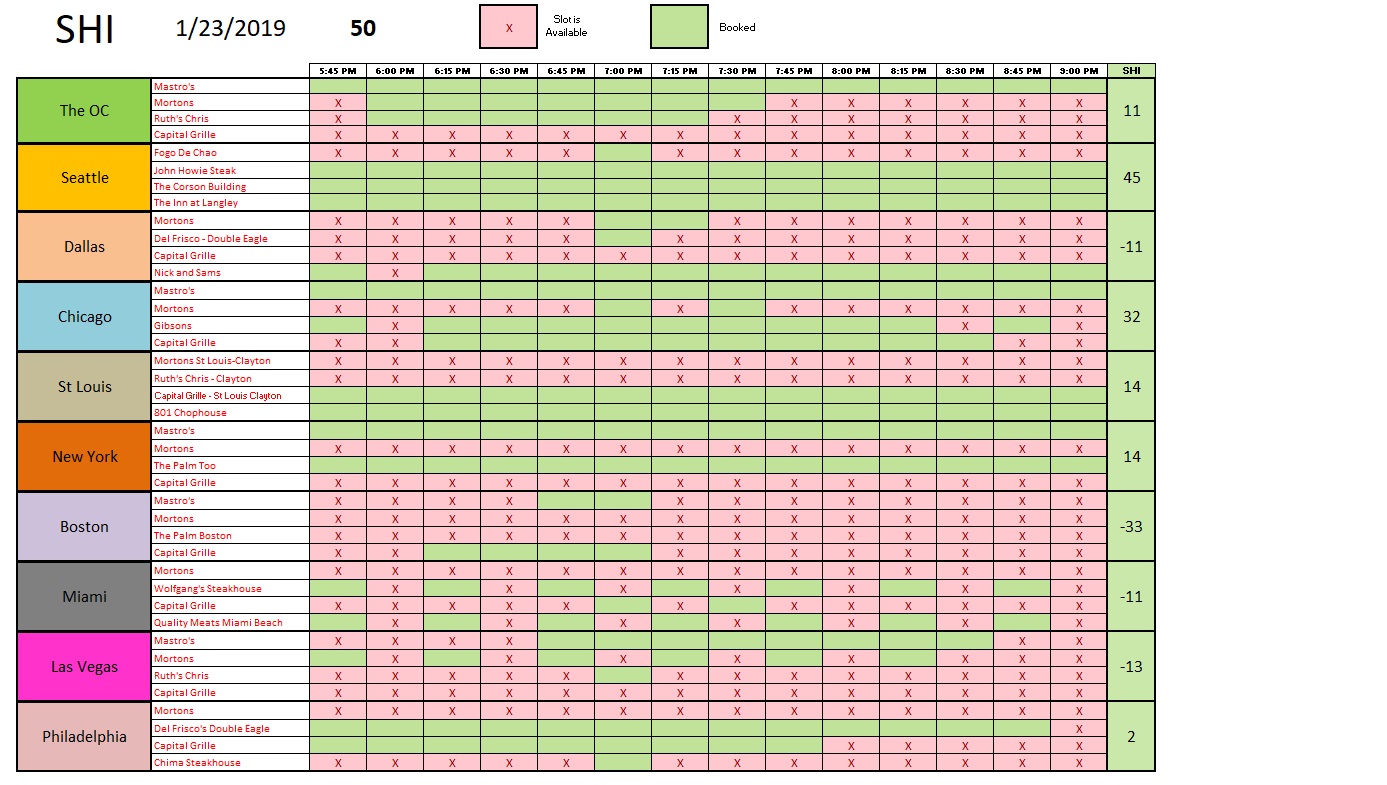

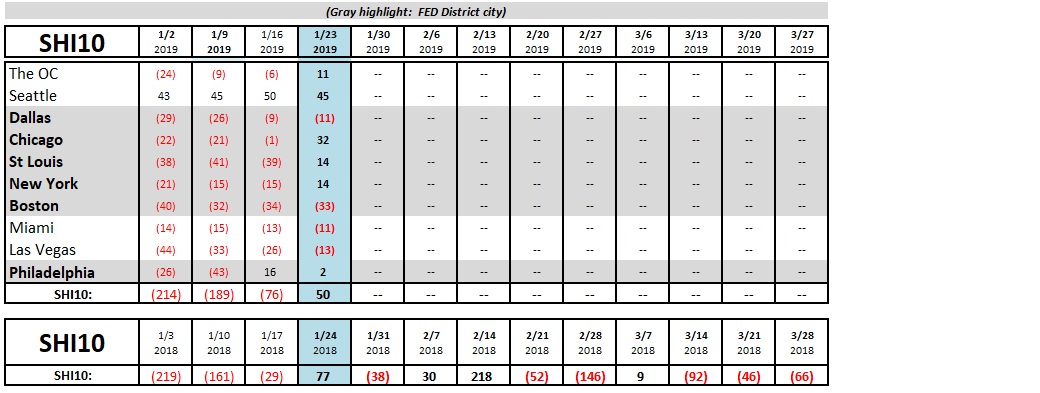

No, they are not. In fact, this weeks SHI10 reading is a positive 50. Up from a negative 76 last week. That is a sizable increase. Looking at reservation availability at the forty (40) restaurants that make up the SHI10, its pretty clear reservation demand has increased across the board:

In fact, with the exception of Seattle — where reservation demand is always in the stratosphere — and Dallas and Philly, where demand fell only slightly, every other SHI city saw significant increases in demand.

Interestingly enough,this week last year (2018) saw the same spike in demand. Take a look:

Summing up, this is clearly a turbulent time in both US and global economics. We have both headwinds and tailwind swirling around us. Consumer confidence numbers may be weakening, but high-priced steak demand has firmed. So, for now, hang on tight, pay attention, but the US is doing fine. No recession. At least not yet. But the longer the government shut-down continues, the heavier the bag of stones becomes.

– Terry Liebman