SHI 1.16.19 – Sputtering Engines

SHI 1.9.19 – Just Kidding?

January 10, 2019

SHI 01.23.19 – Can This Be Fixed?

January 23, 2019

“A soft landing. That sounds so pleasant.”

I’m not a fan of soft landings. Don’t get me wrong: I absolutely LOVE soft landings when I’m flying Southwest. Or any other plane for that matter. But I’m not a fan of economic soft landings. No, I’m not advocating for a recession. I simply prefer robust growth! So I’m disappointed the signs are pointing to a soft landing in our near future. Maybe.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will continue to be true for years to come.

Is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is about $80 trillion today. US ‘current dollar’ GDP now exceeds $20.66 trillion. In Q3 of 2018, nominal GDP grew by 4.9%. We remain about 25% of global GDP. Other than China — a distant second at around $12 trillion — the GDP of no other country is close.

The objective of the SHI10 and this blog is simple: To predict US GDP movement ahead of official economic releases — an important objective since BEA (the ‘Bureau of Economic Analysis’) gross domestic product data is outdated the day it’s released. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

Not only did the Dow, S&P 500, and every other major index take a huge dive by the time 2019 rolled around, but so did the 10-year Treasury yield. On November 9th, it peaked at 3.21%. Today, it is closer to 2.7% — a 50 basis point decline.

Yes, we’ve seen about a 10% recovery in stock prices since then. Good. The market was definitely oversold. But it’s pretty obvious to those of us watching closely that all is not right with the world. Economically speaking, of course. After all, this is the Steak House Index, not a political commentary blog.

The list of economic headwinds is long. Let’s go from large economies to smaller:

- United States: Recession talk aside, it would be hard to argue economic growth is not slowing somewhat. Investor and consumer sentiment both reflect concern. The financial markets are flashing concern over the level of future corporate profits, inflation, and growth, with concerns reflected in stock market volatility, the significant decline in US Treasury bond yields, and the flattening yield curve. Consumers are also weighing in. All consumer surveys indicate lower expectations for future conditions. Finally, while damage from the trade war seems limited so far, there is no shortage of fear and uncertainty around the issue. And the government shutdown doesn’t help. Not one bit.

- European Union: on January 14th, Eurostat — the EU agency responsible for ‘official’ government statistical releases — announced industrial production fell by 1.7% in the 19 countries that make up the ‘euro area.’ The strongest economy in the EU — Germany — saw industrial production slip 1.9% in November of last year, and exports fell due to “weak external demand.” Official releases show German GDP declined 0.2% (quarter-over-quarter) in Q3, 2018. When the final Q4 statistics are released in March, I suspect the numbers will show Germany is now in recession. And remember: The ECB ‘short-term’ interest rate — the equivalent of the FEDs fund rate — is currently a negative 0.4%. (Compare this rate to the 2.5% FED funds rate here in the US. )

- China: China’s economy is clearly slowing. Like the US, China’s economy is largely consumption based today. Yes, China is still a huge manufacturer. But their ‘consumer class’ is now larger than ours here in the US. From iPhones to Coach purses, their consumers buy “stuff” just like ours do. China has more affluent consumers than we do … and their consumption is larger. Take car sales, for example. China is now the world’s largest car market, selling over 28 million cars in 2017. By comparison, US car sales were a bit over 17 million that same year. By the numbers, in 2017 China’s consumers purchased 65% more cars than US consumers. But car sales numbers in China are now shrinking. For the first time since 1990, new car sales have declined year-over-year, by more than 5%. China’s economy is slowing. There is no doubt about it.

In a world where global GDP is around $80 trillion, the 3 above economies make up about 2/3 of total global GDP. Which means if they are slowing, global growth is slowing. At the same time, the central banks of each have either eliminated all ‘quantitative easing’ or, in the case of the US, actually begun a cycle of quantitative tightening. So here in the US, interest rates are up and the FED is shrinking its (now) $4.1 trillion balance sheet. Their counterpart in Europe, the ECB, is no longer buying bonds, but is maintaining the size of their $5.3 trillion balance sheet, and leaving rates unchanged. Remember, the ECBs ‘short term’ rate is currently a negative 0.4%

China has shrunk their balance sheet by about 10%. It now totals about $5.2 trillion.

The bottom line: Even as the world’s economic engines are beginning to sputter, central bank conditions today offer more headwinds than tailwinds. This is why we see fear and uncertainty in the markets.

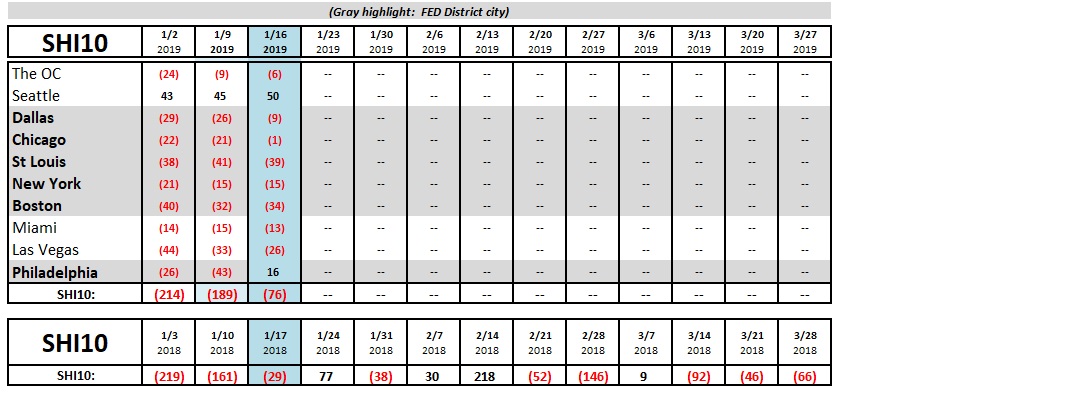

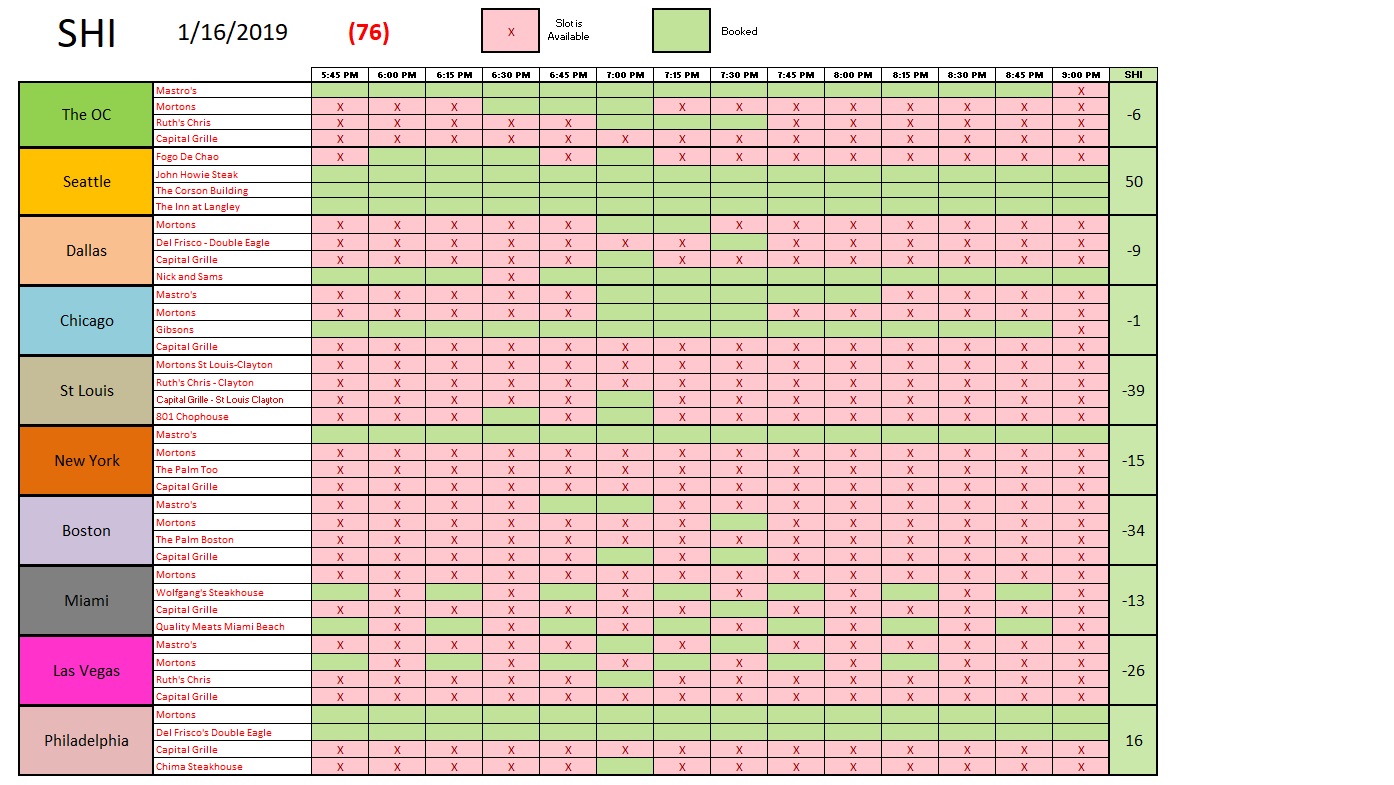

Let’s see if steak lovers are more or less certain they want an 800 degree filet Mignon from Ruths’ Chris.

They do! This week, pricey steaks are popular again! Reservation demand improved across the board. As you see above, this improving trend is consistent with this same time last year. I’m guessing that for the first two weeks of the new year, folks struggle with two choices: Should I go to the gym and work off a few of my newly acquired “holiday” pounds … or should I blow it off and head to Mastros and carbo-load on that Lobster Mac! For two weeks, the gym wins. But by mid-January, a perfectly cooked, fabulously expensive T-Bone is sounding pretty good! Here are the individual restaurant results for the week:

Finally, the FED ‘Beige Book’ was released today. The headlines:

- Economic activity increased in most of the U.S., with eight of twelve FED districts reporting modest to moderate growth.

- Auto sales were flat.

- The majority of Districts indicated that manufacturing expanded, but that growth had slowed, particularly in the auto and energy sectors.

In New York and Kansas City, economic activity was flat. In most other districts, growth continued, albeit at a slower pace.

The bottom line: The pace of economic expansion is definitely slowing. Here and globally. This does not suggest an economic trajectory heading into a recession. But the 3+% GDP growth rates of last year are likely a thing of the past. For now.

– Terry Liebman