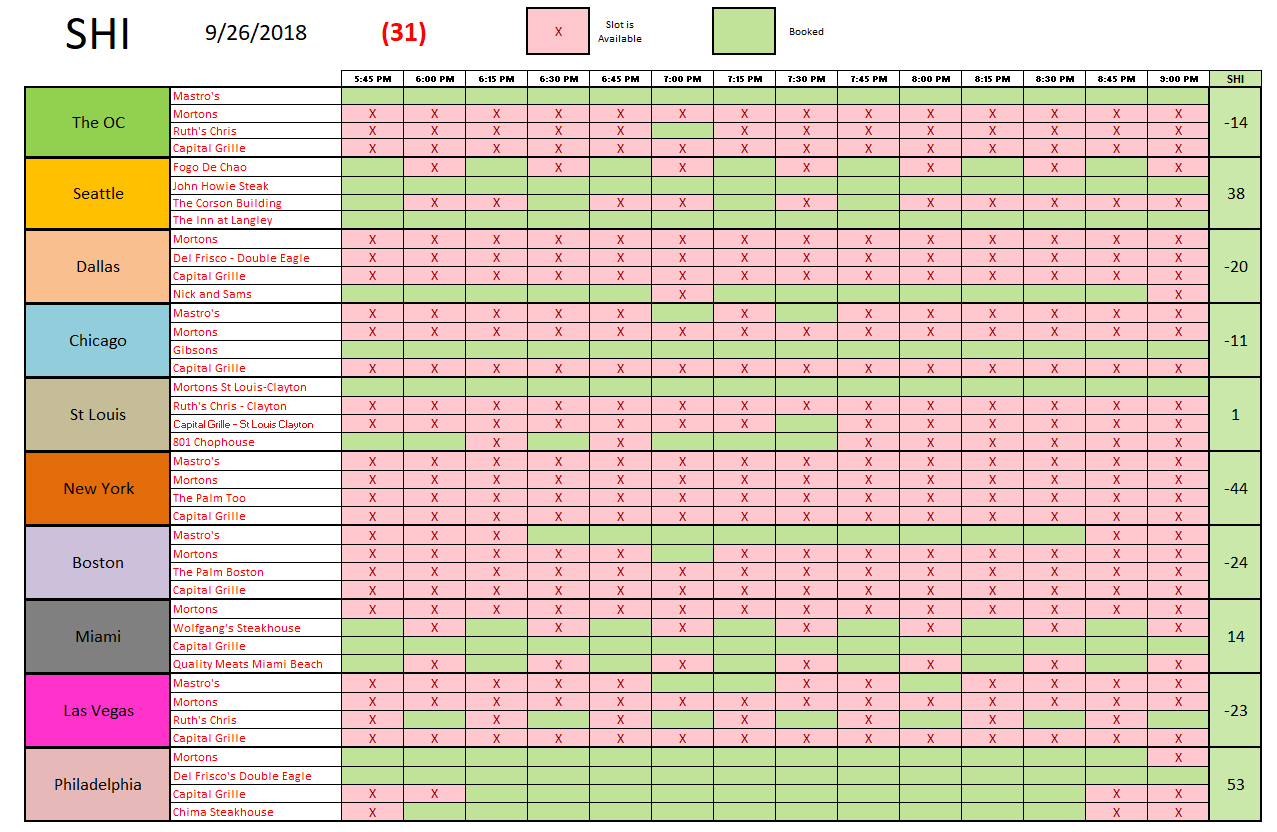

SHI 09.26.18 Hot as Blue Blazes!

SHI 09.19.18 One Thing is Certain …

September 19, 2018

SHI 10.3.18 Steaks On The Run

October 3, 2018

“Steaks at Ruths Chris may be smokin’ hot … but wage growth is not.”

Few economic issues get more press than wage growth. Or the lack thereof.

The rate of annual wage growth is one of the FEDs barometers for measuring possible future inflation. I’m sure they’re talking about this issue right now — since the FED is finishing their FOMC meeting as I write this blog.

The ‘Philips Curve’ theory suggests that as the unemployment rate falls below the “neutral rate” of unemployment, wage inflation will accelerate. Further, the further unemployment falls below the neutral rate, the greater the acceleration in wage inflation. So, according to conventional economic wisdom, right about now wage inflation should be smokin’ hot! Hotter than the searing grill at Mastros.

Yet it is not. In fact, while we’re seeing some increase in wage growth, the rate of increase is lukewarm at best. Why?

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will continue to be true for years to come.

Is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is about $80 trillion today. US ‘current dollar’ GDP now exceeds $20.4 trillion. In Q2 of 2018, We remain about 25% of global GDP. Other than China — a distant second at around $11 trillion — the GDP of no other country is close.

The objective of the SHI10 and this blog is simple: To predict US GDP movement ahead of official economic releases — an important objective since BEA (the ‘Bureau of Economic Analysis’) gross domestic product data is outdated the day it’s released. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

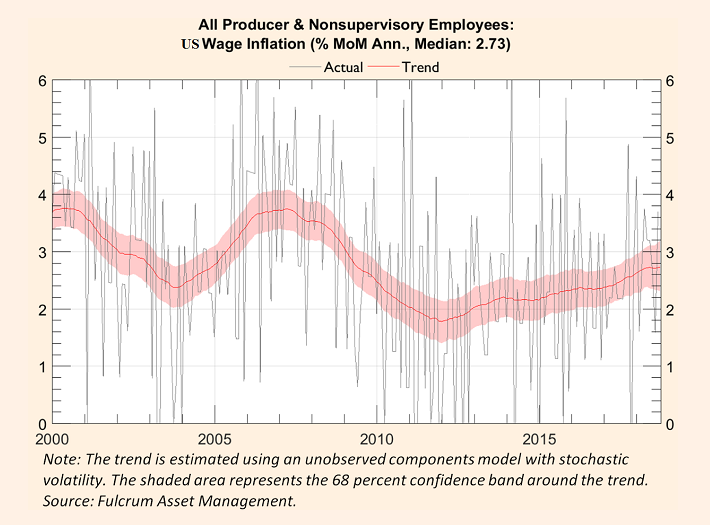

Sure, we are seeing some wage inflation. Absolutely. But not to the extent predicted by the Phillips Curve. And far below the levels seen in prior expansions. Take a look at this graph created by Fulcrum Asset Management:

And now look at the graph below — covering the same timespan as the graph above — in which I have inverted the unemployment rate (U3). I did this to show the directional relationship between the unemployment rate and wage inflation.

It’s easy to see that when unemployment is the lowest — around 2000 and now — wage growth is the highest. But while wage growth was close to 4% back in 2000, today it seems to have maxed out around 2.7%. If the Phillips Curve theory was working properly, wage inflation would be much higher And this has the experts — including those at the FED — rather confused.

Above, I asked the question ‘why?’ I believe there are at least two contributing factors. First, consumer confidence hit an 18-year high in September. Full employment will do that for you. Americans’ expectations for the future are bright. (The Conference Board, a private research group, said Tuesday its index of consumer confidence rose to 138.4, up from 134.7 in August—the highest level since September 2000, which represented the late stages of the 1990s technology boom. An index reading of 100 represents how households saw the economy in 1985.) If Americans are feeling good, they are clearly not worried about inflation. And if they’re not worried about inflation, they don’t seek a raise at work.

Second, I’ve talked extensively about demographics and automation is prior blogs. These factors, too, I believe, help keep a lid on wage inflation.

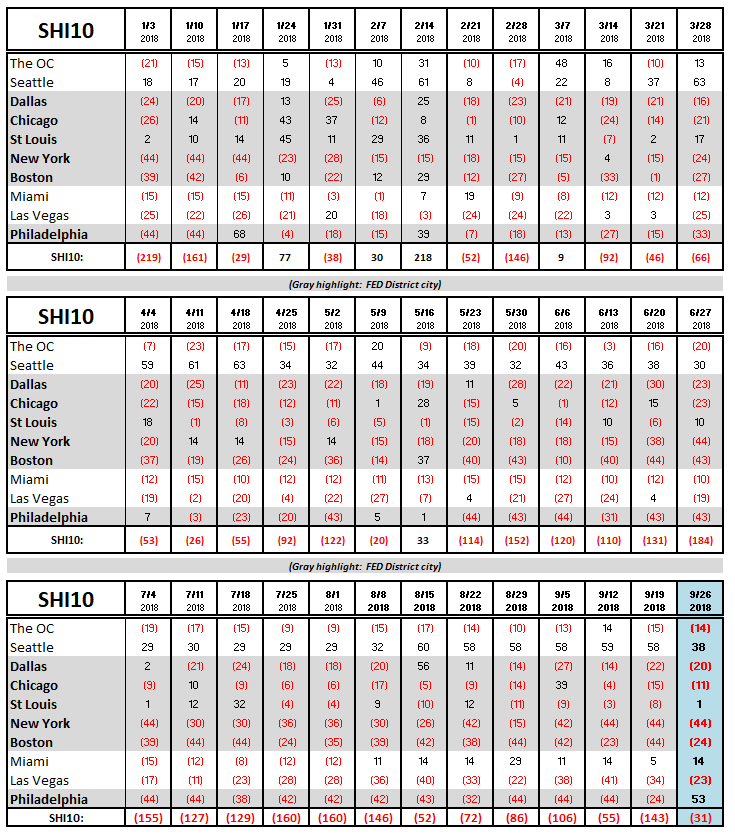

OK…we’ll come back to the FEDs rate decision a bit later. For now, lets head over to our pricey eateries. This week we see meaningful improvement in the SHI10:

Check out Philly! Welcome to the party, Philadelphia! An SHI of 53 is their best showing ever. I used to feel sorry for steakhouse owners in Philly. Now, I’m thinking NYC steakhouse owners are even more worthy of my pity. The Big Apple has clearly turned vegan! No carnivores here … except, perhaps, on Wall Street. The OC and Seattle are consistent with last week, and the balance of our 10 cities show standard variability. Take a look:

Let’s head back to the FED. In his press conference following the FOMC press release, FED Chairman Powell commented:

“Our economy is strong.”

Agreed. It is. As a result, the FED made the decision to raise their short-term ‘federal funds’ target rate by 25 basis points. The rate is now 2.25%. Borrowing costs on credit cards and autos will now increase. Here is the FEDs summary:

“Information received since the Federal Open Market Committee met in August indicates that the labor market has continued to strengthen and that economic activity has been rising at a strong rate. Job gains have been strong, on average, in recent months, and the unemployment rate has stayed low. Household spending and business fixed investment have grown strongly. On a 12-month basis, both overall inflation and inflation for items other than food and energy remain near 2 percent. Indicators of longer-term inflation expectations are little changed, on balance.”

It’s worth taking a peak at the FEDs longer term forecasts for things like GDP and short-term rates. Here’s a link to the data released earlier today: https://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20180926.pdf

But while the US economy remains strong today, the FEDs action increases future economic headwinds. I’m not suggesting the rate hike was inappropriate. I’m simply stating that the seeds of the EOY 2020 recession are being planted with each rate increase. The bond markets seem to agree: In response to today’s action, rates on shorter-term Treasurys increased; the rate on the 10-year, decreased. Our yield curve is flatter … and inversion approaches.

Yes, Chairman Powell, our economy is strong. Today. Give it time. The winds of change approach.

- Terry Liebman