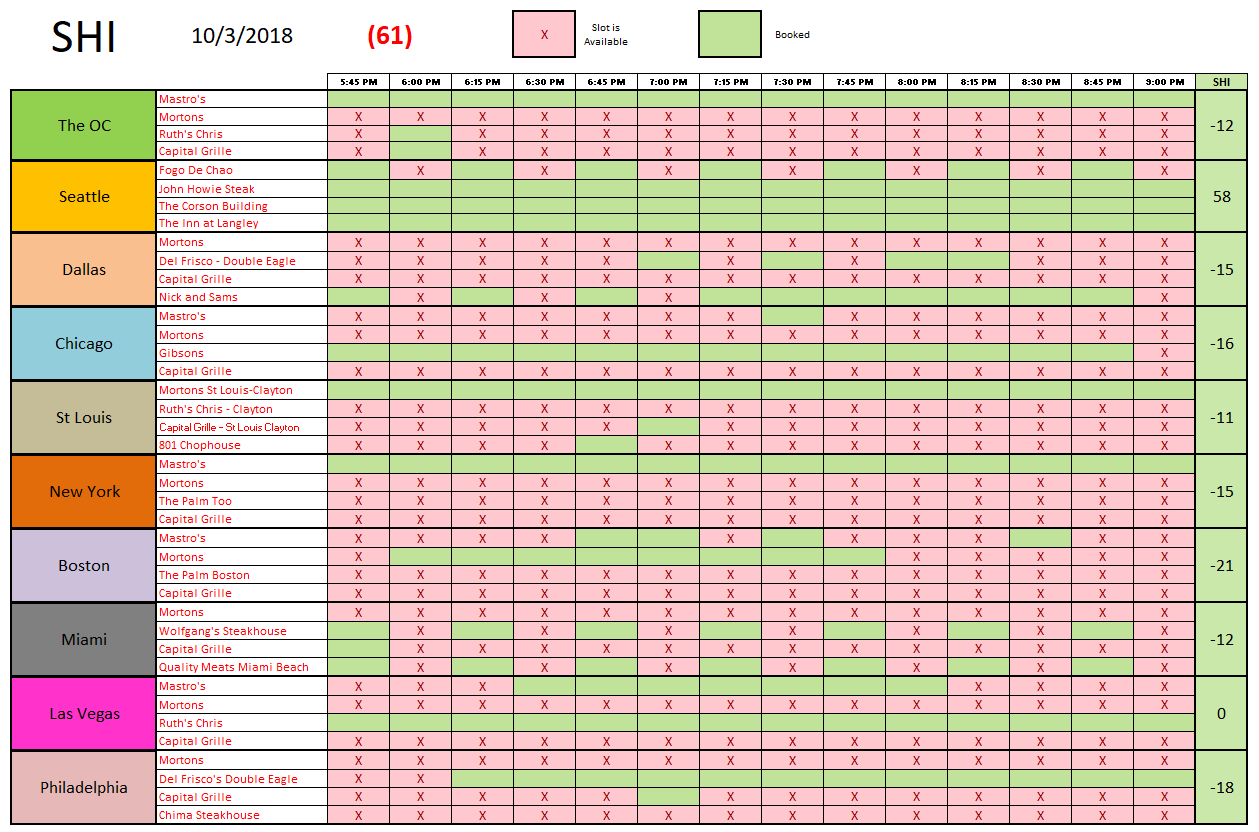

SHI 10.3.18 Steaks On The Run

SHI 09.26.18 Hot as Blue Blazes!

September 26, 2018

SHI 10.10.18 The Investor vs. the Consumer

October 10, 2018

“Some lucky fugitives escape the steak house.”

Take ‘Frank Lee‘ for example. According the the Wall Street Journal:

“Frank Lee bucked free from the back of a delivery truck chauffeuring him to his doom at a small abattoir in Brooklyn in April 2016. Still a bull at the time, he raced alongside cars on a street in Queens, passing school buses and storefronts until he found his way to York College. There he knocked a man over as students taking cellphone video turned him briefly into an internet sensation. City police ended his 20-minute freedom run with lassos and tranquilizers.”

But good news for Frank! His jailbreak earned him permanent freedom. Frank now spends his days roaming the 275-acre ‘Farm Sanctuary’ in upstate NY … and no longer has anything to fear from the likes of Nicks, Mastros or Ruths Chris. Frank is free as a bird. For life. 🙂

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will continue to be true for years to come.

Is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is about $80 trillion today. US ‘current dollar’ GDP now exceeds $20.4 trillion. In Q2 of 2018, We remain about 25% of global GDP. Other than China — a distant second at around $11 trillion — the GDP of no other country is close.

The objective of the SHI10 and this blog is simple: To predict US GDP movement ahead of official economic releases — an important objective since BEA (the ‘Bureau of Economic Analysis’) gross domestic product data is outdated the day it’s released. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

Martin Feldstein and I agree on one thing: And that is our shared belief that a recessing is coming. In the not too distant future. In fact, ‘Another Recession is Looming’ was the title of his OP/ED piece in the Wall Street Journal on 9/27.

But we disagree on a number of issues. That said, please note that Mr. Feldstein has a long and esteemed work history in economics, including:

- President, the National Bureau of Economic Research

- Chairman, Council of Economic Advisors and the chief economic advisor to President Reagan

- Professor of Economics, Harvard University

So, you may be wondering, what does Mr. Fieldstein have to do with ‘Steaks On The Run?’ Absolutely nothing. I simply found Frank to be an entertaining detour.

OK…back to Mr. Feldstein. He’s a very accomplished man. On the other hand, I do not now, nor have I ever, held such esteemed roles or titles. So while I disagree with a few of Mr. Feldman opinions below, frankly, you might want to take his opinion over mine. I’m a nobody. 🙂

OK…now that I’ve completed my self-deprecation, let’s jump into the debate! Here are quotes from Mr. Feldstein’s article:

- “… another long, deep downturn may soon roil the U.S. economy. … a downturn brought on in the next few years by rising long-term interest rates would likely be deeper and longer than your average recession. “

- “The high level of asset prices today mirrors the earlier trend in house prices that preceded the 2008 crash; both mispricings reflect long periods of very low real interest rates caused by Federal Reserve policy.”

- “But if one (a recession) hits in the next few years, the Fed will not have enough room to cut rates, as the fed-funds rate is expected to rise to only 3% by 2020. There also won’t be much room for a major fiscal intervention.”

Long, deep downturn? I don’t think so. It might be long … but I doubt it will be deep. Remember, a “downturn” means an economic contraction. An economic contraction is defined as two consecutive quarters of negative GDP growth. I believe the contraction will be as tepid as our current expansion. This has been one of the slowest, least exuberant recoveries in history. I suspect the contraction will follow the same pattern.

The asset price comment is more interesting to me. Asset prices move inversely with interest rates. Meaning, when interest rates are low, asset prices are higher. And the opposite holds true. All interest rates were sky high between 1980 and 1990. From there, they made a leisurely slide, interrupted with peaks and valleys, to the rate levels we saw just before the ‘Great Recession’ in 2008. It would be hard for me to argue that the almost-zero FED funds rate in place for years thereafter isn’t low. Short term rates have never been lower in this country. Never. However, as my long-time blog readers know, short term rates did get lower than zero in many parts of the world. In fact, central bank ‘benchmark’ short-term rates today remain below zero in:

- European Central Bank: Negative 0.4%

- Germany: Same as the ECB

- Switzerland: Negative 0.75%

- Sweden: Negative 0.5%

- Japan: Negative 0.1%

Our FED funds rate is now 2.25%.

And the list goes on. My point: The US has one of the highest central bank short-term rates of any stable, developed nation. How about long-term rates? Here are the 10-year government rates for the same countries:

- European Central Bank: 1.32%

- Germany: 0.45%

- Switzerland: 0.018%

- Sweden: 0.66%

- Japan: 0.14%

Today the US 10-year is trading near 3.1%.

Here’s my point. US interest rates a much higher than other developed nations around the globe. Mr. Feldstein may believe the US 10-year treasury can rise to 5% in this environment. I do not.

And since long-term rates will not rise significantly above their current levels — certainly not for any protracted period of time, even if they do temporarily — asset prices are not generally at risk.

The FED funds rate is now 2.25%. It’s likely to be closer to 3% when the recession begins. The FED will have plenty of room to cut rates and once again create an expansive, accomodative economic condition. In fact, as the rest of the developed world has shown us, the FED can even use negative interest rates, if need be.

All right, that’s enough bull for today. Let’s slice into some prime beef!

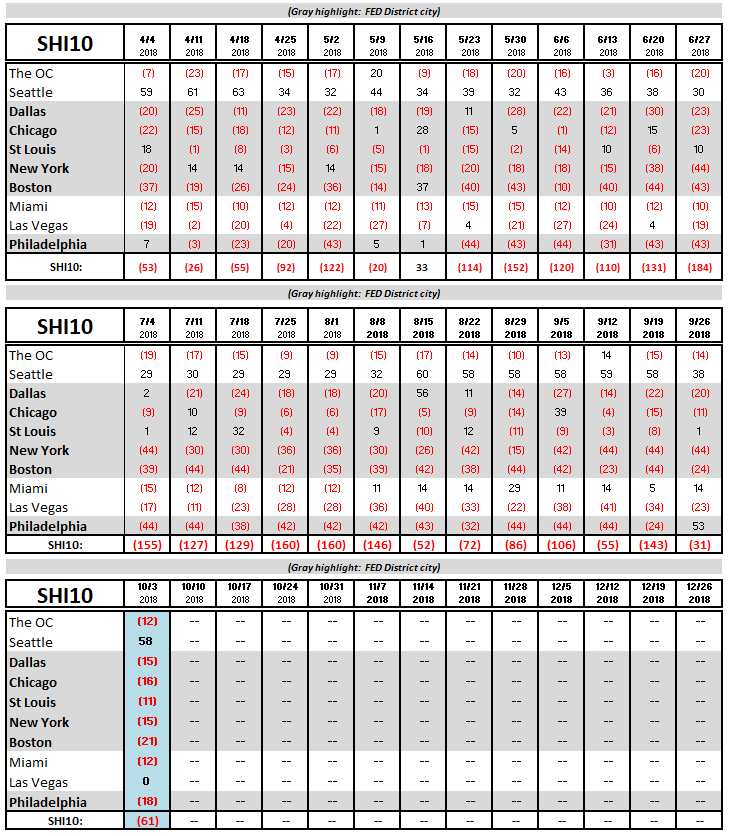

We’re now in the 4th calendar quarter, so you’ll notice I’ve dropped the Q1 data from the chart. This week the SHI10 is little changed from recent readings. Vegas is finally out of the red — barely. Here are this week’s SHI readings:

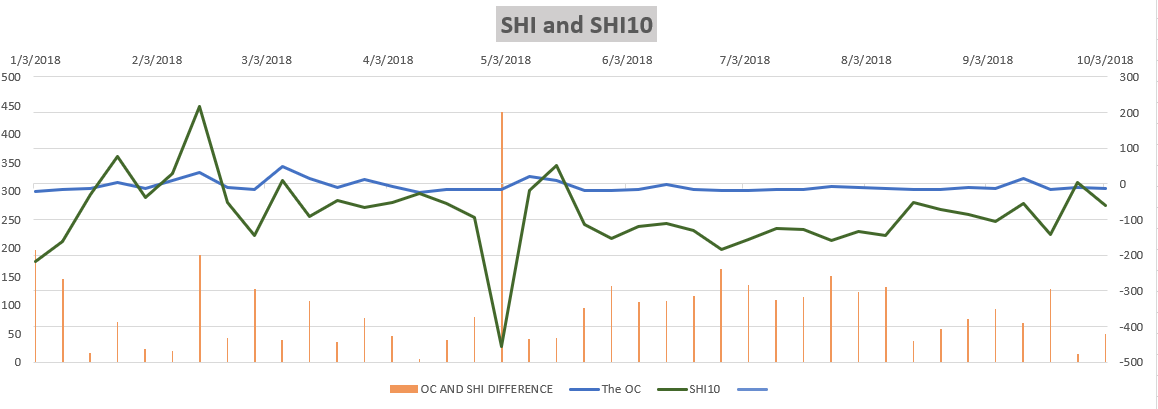

Finally, Kyle Anderson, my trusty SHI contributor and fellow steak-lover, offered up the graph below for your consideration. Thanks Kyle!

The blue line is the original SHI for Orange County, CA. The green line, the SHI10 reading for our 10-city index. And the orange vertical lines show the ‘delta’ between the two. The graph clearly shows the Orange County SHI has been rather consistent this year. And while the SHI10 has been volatile, recently is has been more consistent and improving. Take a look:

It may seem surprising to you that both Martin Feldstein and I are talking ‘recession’ while, by all indications, the US economy is clearly doing quite well. I understand. But remember, in this blog we’re attempting to read the “tea leaves” and forecast the future. The SHI is intended to help us forecast future economic activity…not what we’re seeing today.

So I’m sorry to be such a downer…talking about a recession in a couple of years. Personally, I think we should blame Martin Feldstein. After all, he’s the ‘brain’ here. I’m a nobody. 🙂

– Terry Liebman