SHI 10.10.18 The Investor vs. the Consumer

SHI 10.3.18 Steaks On The Run

October 3, 2018

SHI 10.17.18 That’s Quite a JOLT!

October 17, 2018

“Consumer confidence hovers at an 18 year high.”

About two weeks ago, Lynn Franco, the Director of Economic Indicators at the Conference Board commented:

“After a considerable improvement in August, Consumer Confidence increased further in September and hovers at an 18-year high (138.4). The September reading is not far from the all-time high of 144.7 reached in 2000. Consumers’ assessment of current conditions remains extremely favorable, bolstered by a strong economy and robust job growth.”

The bond market seems to agree. Debt investors have driven up long-term treasury yields by more than 25 basis points in the last month, steepening the yield curve, suggesting bond traders see robust GDP growth ahead!

Then why, you might ask, is the Dow Jones Industrial Average dropping like a stone? From it’s recent peak of 26,828 on Wednesday, the 3rd, to about 25,598 — almost a 5% drop — at the time I’m posting this blog? Shouldn’t the stock market be rising, too? 🙂

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will continue to be true for years to come.

Is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is about $80 trillion today. US ‘current dollar’ GDP now exceeds $20.4 trillion. In Q2 of 2018, We remain about 25% of global GDP. Other than China — a distant second at around $11 trillion — the GDP of no other country is close.

The objective of the SHI10 and this blog is simple: To predict US GDP movement ahead of official economic releases — an important objective since BEA (the ‘Bureau of Economic Analysis’) gross domestic product data is outdated the day it’s released. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

Consumers clearly are feeling flush. This bodes well for our economy. Investors, on the other hand, don’t seem to be sharing their exuberance. In fact, this last week suggests equity traders are more worried about the future than consumers. Could tariffs and trade fears finally be taking their toll? Or might investors harbor a growing fear that past and future FED rate increases might choke-off our almost 10-year economic recovery?

It’s probably too early to tell. But worth watching. And keep this in mind: Stock investors are known to sell stocks and buy US treasury bonds when yields get high enough. Could that explain recent stock movement? Now that the 5-year treasury is yielding over 3%, this return can draw investors from the equity markets. Remember, a couple years ago, the 5-year treasury was yielding near 1%.

So, reviewing, consumer confidence is strong. Rates are higher. The stock market is down. A lot. Perhaps not every investor is worried about the economic headwinds coming our way, but quite a few are. And those fearful folks are selling their positions. Am I doing the same? No. I have sold nothing. I think they are over-reacting. We’ll see who’s right in the coming weeks.

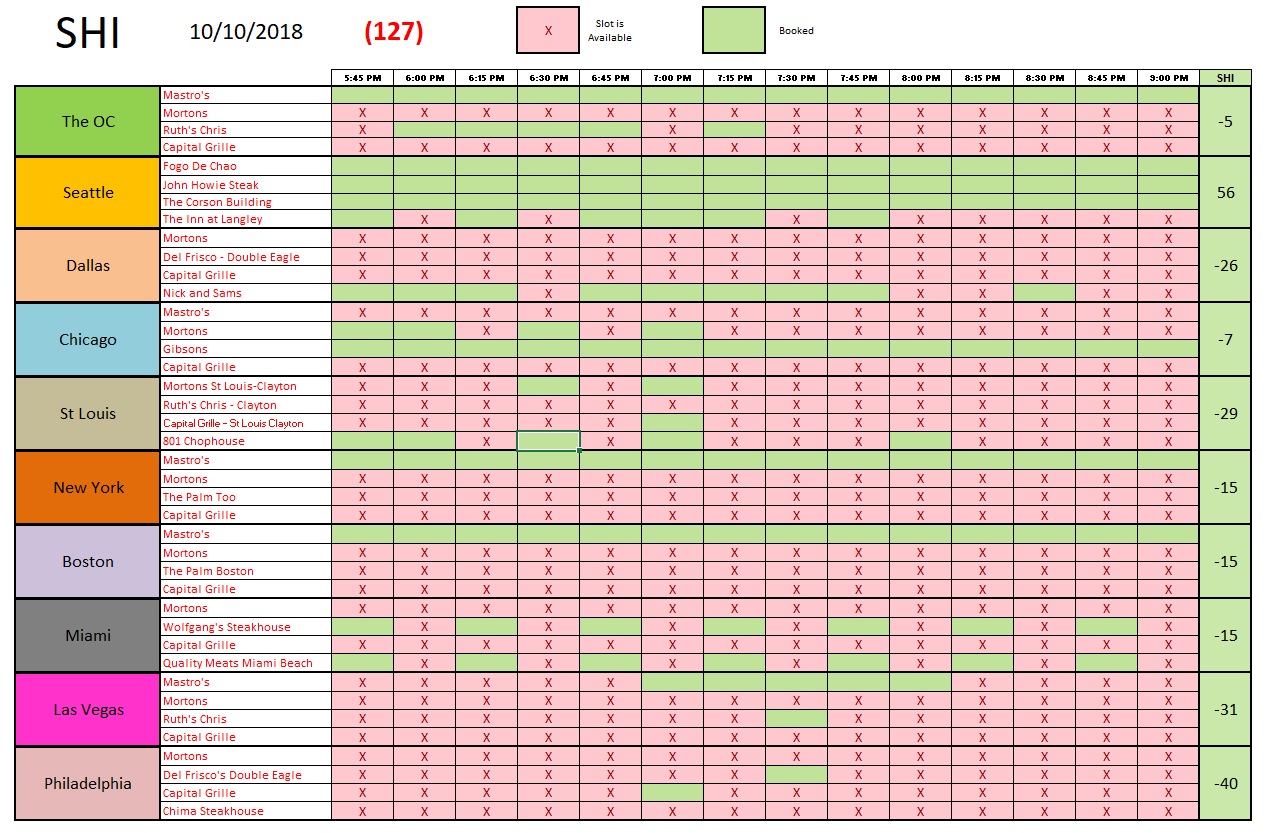

Piping-hot steaks are still flying off the griddle, however. The ‘best’ reservations at our pricey eateries are hard to get:

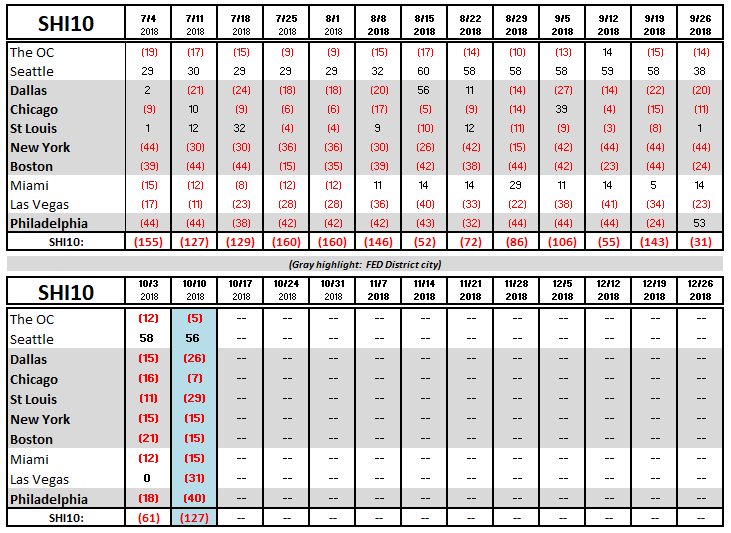

It’s interesting: Mastros continues to be the “hot ticket” in most markets. Clearly they do something right … because they are probably one of the most expensive restaurants in every market. Most cities are showing a weaker SHI this week than last, which we can see clearly from the trend report:

Could the market volatility be indicating the beginning of the end of our economic expansion? Probably not. I believe it reflects investor nervousness only. The consumer is happy and spending. But the investor is worried about yields, trade battles, and FED rate increases. We will watch each of these carefully in the weeks to come. They are important headwinds … all packing potentially hurricane-force winds.

- Terry Liebman